Wow… if things get any more uncertain, I may have to give up footy tipping and take up something easier — like forecasting interest rates.

Since our Snapshot edition sent to you last week, the big picture has not exactly become calmer.

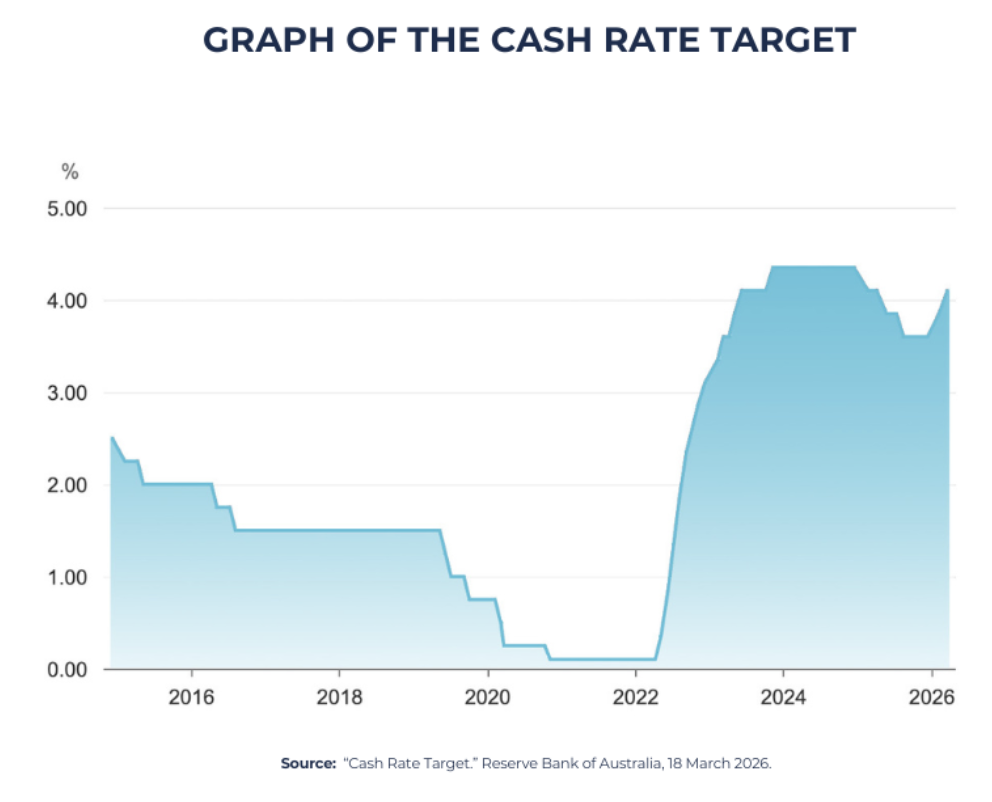

The Reserve Bank of Australia has now lifted the cash rate by another 0.25%, taking it to 4.35%. That makes three increases this year and takes the cash rate back to its post-COVID peak.

Some borrowers may have a little more buffer than they realise if they kept repayments higher during earlier rate cuts, but that still needs to be checked against their actual loan setup.

So yes, the noise is getting louder.

Global events, supply pressures, energy uncertainty, rising costs, stubborn inflation and a Federal Budget focused on both repair and political philosophy have all made the finance and property outlook harder to read.

But that does not mean we stop thinking clearly.

As Rudyard Kipling wrote:

“If you can keep your head

when all about you are losing theirs…

you’ll be a Man my son!”

Now, it must be said, Kipling did have two daughters, so perhaps we can safely update the sentiment for today without references to sons or daughters:

If you can keep your head when the market feels noisy, you give yourself a much better chance of making a sensible decision.

That is really the point of this edition.

The aim is not to predict every twist and turn. It is to slow things down, look at what is changing, and consider what it may mean for your loan, your property plans, your cash flow and your next decision.

This month’s edition of the The Deep Dive contains the following topics:

- Making a home loan tax deductible – what can actually be done?

- How to stay ahead as rates keep rising

- What rising rents mean for your buying plans

- Plan your property purchase – before emotions set your budget

- Tax depreciation schedules – what property investors should check before year end

- The causes of our housing crisis – housing supply Vs Investor’s competing demand Vs Tax

- Planning to build? Costs are changing

- EV sales hit record share in March

- Fuel security and EVs – why Australia’s petrol problem is bigger than the bowser

Read more below.

Making A Home Loan Tax Deductible:

What can actually be done?

Key Message: Many people wonder whether their home loan can be made tax deductible. The answer usually depends less on the loan itself and more on what the borrowed money was used for.

I received a query on this topic recently from a client and thought that it would be a good one to research and separate fact from myth. I ran this past my good friend and tax advisor, Swati Gupta, IX Advisory, to make sure I had covered the issues from a technical perspective – so a shout out to Swati for her useful input!

Before giving you the details, this topic always involves the rider: speak with your accountant before proceeding. The tax outcome depends on the structure, the use of funds and the records kept.

Our blog site will have an even more in-depth version of the article below. So whilst this article is thorough, there is a bit more depth in the blog we have created. Plus, we are developing our Debt Recycling Checklist

What was the borrowed money used for?

If the money was borrowed for private purposes, the interest is generally not deductible. If the money was borrowed for an income-producing purpose, the interest may be deductible, provided the structure and records are clean.

Where deductibility may come into play?

There are several situations where part of a home-loan position may move into deductible territory.

These can include:

- Debt recycling, where home debt is reduced and then re-borrowed in a separate split for an investment purpose

- A redraw or top-up used only for income-producing investments

- A former home becoming a rental property

- Renting out part of your home

- Using part of the home as a genuine place of business, in limited cases

The detail matters.

For example, if you redraw money from your home loan and use it for a private purpose, such as a car, holiday or school fees, that part of the loan is generally private. It does not usually become deductible just because the property later becomes a rental.

That is why loan splits, offsets, redraw history and clear records can make a big difference – and why you should always consult with your tax advisor before commencing the process.

Offset versus redraw — the trap many people miss

This is one of the most important parts of the whole topic.

An offset account and redraw can both reduce interest while money is sitting against the loan, but they are not the same for tax and record-keeping purposes.

An offset account usually holds your own cash. It reduces the interest charged on the loan, but the loan balance itself does not usually change.

Redraw is different. If you pay extra into the loan and later redraw funds, you are generally borrowing money again. The tax treatment then depends on what the redrawn money is used for.

That difference matters in two common situations.

1. Your home may later become an investment property

If there is a chance your home may later become a rental property, keeping surplus cash in an offset account attached to the main home loan is usually cleaner than paying down the loan and later redrawing for private use.

Why?

Because private redraws can create a private, non-deductible portion of the loan. If the property later becomes a rental, that private portion does not usually become deductible just because the property is now rented.

So, if future rental use is possible, the cleaner approach is often:

- Keep surplus cash in an offset account linked to the main private home loan

- Use the offset to reduce interest on the non-deductible debt

- Avoid private redraws

- Preserve the original loan purpose

- Keep good records

The practical message is simple:

Use offset to reduce private home loan interest while keeping the loan purpose cleaner.

2. You want to use existing home loan funds to invest

If you simply withdraw money from offset and use it to buy shares or another investment, you have usually used your own cash. That does not usually make the home loan interest deductible.

To create interest linked to an investment purpose, there usually needs to be a borrowing event.

The cleaner approach is often to set up a separate split under the existing home loan, then redraw or re-borrow from that split and use those borrowed funds only for the investment.

This does not always mean changing lenders or taking out a completely new loan. In some cases, it can be done as part of the original loan setup or by restructuring the existing loan with the current lender.

But the details matter.

The “set and forget until needed” option

If a client has a high degree of certainty that they will invest later, one option is to set up the loan with future flexibility from day one.

For example, the loan might be structured as:

- Main loan split: private home loan

- Offset account: linked to the main loan split, so spare cash reduces non-deductible interest

- Smaller second split: kept separate and available for a future investment purpose

The offset account should generally be linked to the main private home loan split first. That way, while the client is building cash, the offset is reducing interest on the non-deductible home debt.

Then, when the client is ready to invest, the intended process may be:

- Use the offset funds to reduce the smaller investment-purpose split

- Redraw or re-borrow from that smaller split

- Use those redrawn borrowed funds only for the income-producing investment

- Keep clear records showing the money trail

The benefit is that much of the structure can be prepared when the original loan is set up. That may make it more “set and forget until needed”, rather than trying to rebuild the loan structure later.

But this only works neatly if the second split is close to the amount the client actually intends to invest.

The Goldilocks problem

The second split needs to be a bit like Goldilocks:

Not too high. Not too low. Just right.

If the split is too small, the client may not have enough available for the investment and may need another restructure.

If the split is too large, they may be left with unused debt capacity, or they may be tempted to use part of the split for something else. That can create mixed-purpose debt and messy record keeping.

If the client invests in multiple stages, or uses the split for both investment and private spending, the interest may need to be apportioned. That is where the clean structure can quickly become untidy.

So this “day one” setup should usually only be considered where:

- The client has a clear plan to invest later

- The likely investment amount is known with reasonable confidence

- The second split can be sized appropriately

- The client will not use the investment split for private purposes

- The accountant is comfortable with the structure before funds move

Offset funds versus investing — the after-tax question

There is another issue that should not be skipped.

Before using offset funds as part of an investment strategy, the client needs to compare the benefit they are giving up with the return they hope to earn.

Money sitting in offset reduces interest on the home loan. If the home loan interest is private and non-deductible, that saving is usually an after-tax benefit.

For example, if the home loan rate is 6% pa, money in offset is effectively saving 6% after tax on that amount.

If the client takes that money out of offset and invests, the investment needs to justify giving up that saving.

That means looking at:

- The expected investment income

- The expected capital growth

- Tax on the investment income

- Possible capital gains tax

- The interest cost on any investment borrowing

- Whether that interest is deductible

- Fees, risk and time frame

- The client’s cashflow and comfort level

The practical question is not just:

“Can I make some interest deductible?”

It is also:

“Is the investment likely to leave me better off after tax, after costs and after risk?”

That is why this area needs tax advice and, where investment decisions are involved, licensed financial advice. A loan structure can support a strategy, but it should not drive the investment decision by itself.

The practical takeaway

The cleanest rule is:

Use the offset account to reduce non-deductible home loan interest. Use a separate loan split if you want to re-borrow for investment. Avoid mixing private and investment purposes in the same loan account.

If the investment plan is clear from day one, the structure may be built into the original loan setup. But if the likely investment amount is uncertain, it may be cleaner to wait and set up the right split closer to the time.

How To Stay Ahead As Rates Keep Rising

Key message: Higher rates, higher living costs and global uncertainty are making loan reviews more important. The answer is not panic. The answer is knowing your numbers.

With the Reserve Bank of Australia (RBA) now lifting the cash rate for the third time this year, borrowers are facing a tougher environment.

The May decision lifted the cash rate target to 4.35%, returning it to its post-COVID peak. That does not mean every borrower should panic, but it does mean loan reviews matter more than they did a few months ago.

There is also a useful point that can get lost. During earlier rate cuts, many borrowers did not reduce their repayments when their minimum repayment fell. If that is you, the latest rate rise may reduce your repayment buffer rather than immediately increasing your direct debit. But this depends on your lender, loan type and repayment setup.

The May decision came after headline inflation rose to 4.6% in the 12 months to March, while trimmed mean inflation sat at 3.3%. In plain English, inflation is still above the RBA’s comfort zone, and fuel, transport and broader supply pressures are making the path forward harder to read. The Australian Bureau of Statistics reported March headline CPI at 4.6%, with Transport up 8.9% and Housing up 6.5%.

The difficulty right now is that sentiment and fundamentals are pulling in different directions. Higher rates, global uncertainty and cost-of-living pressure are making people cautious. But employment remains relatively strong and rental vacancy remains tight, which means the broader property market is not behaving like a simple downturn.

That does not mean every borrower should refinance immediately.

But it does mean your current loan should not be left on autopilot.

The main issue is not just the cash rate. It is the total pressure on household cashflow. Fuel, groceries, insurance, rent, building costs and general living expenses are all part of the same household budget.

So the practical question is simple:

Is your loan still doing its job?

Where you still have control

There are still practical steps you can take:

- Review your current interest rate and product features

- Check whether your lender is still competitive

- Compare your current loan against realistic alternatives

- Revisit your offset, redraw and repayment structure

- Check your buffer before things feel tight

My usual suggestion after an RBA rate rise is not to rush into a refinance unless your situation is urgent. Lenders can move at different times, so waiting a couple of weeks can make comparisons cleaner once more rate decisions have flowed through.

That does not mean doing nothing. It means checking your rate, repayments, buffer and loan structure now, so you are ready to compare properly once the market has settled.

Even a small change can matter when rates and costs are rising.

And as I often say to clients:

“If there’s a possible saving available,

would you rather keep it in your bank account —

or hand it to your lender?”

If things get tight

If repayments are starting to feel uncomfortable, early action usually gives you more choice.

That may include speaking with your lender, reviewing your loan structure, checking hardship options, or seeing whether refinancing is realistic.

The earlier you act, the more room you usually have to move.

The practical takeaway is this:

Do not make big finance decisions based only on what the media says the RBA “might” do next. What matters is your actual rate, your actual repayments, your buffer and your options.

If you want to sense-check your loan in today’s market, I can help you review where you stand.

What Rising Rents Mean For Your Buying Plans

Key message: Rising rent can make saving a deposit harder, but it may also push some buyers to review their plans sooner rather than waiting for the “perfect” time.

Rental costs are still putting pressure on many households.

For renters trying to save a home deposit, that is a real problem.

Higher rent can slow deposit savings. At the same time, higher interest rates can reduce borrowing capacity. The latest RBA increase only adds to that pressure, because buyers now need to test their repayments against a higher-rate environment. That combination can make the path to buying feel harder, even for people who are doing the right things.

But harder does not mean impossible.

Why this is getting harder?

There are three pressures working together:

- Rent is taking a larger slice of income

- Higher rates can reduce borrowing power

- Living costs can make lenders more cautious about serviceability

That means a buyer who looked comfortable six months ago may need to reassess their numbers now.

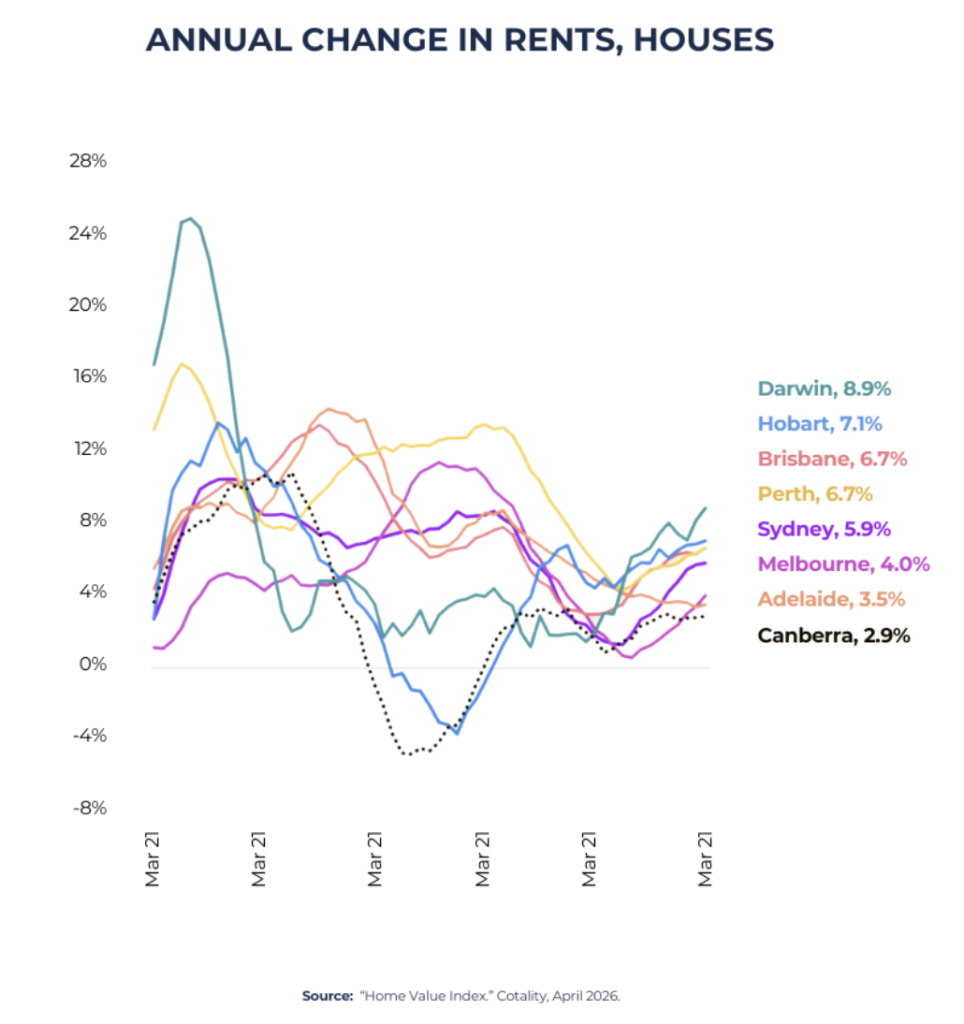

A recent newsletter issued by Gaurav Bhatia, Equimax Property Group, a firm of property investment advisors, also highlighted the following data showing that recent rental data reinforces the pressure. National annual rental growth was 5.7%, while the national vacancy rate sat at 1.6%. Every capital city recorded a vacancy rate below 2.0%, which tells us the pressure is not confined to one or two cities.

For renters trying to buy, this creates a double squeeze. Higher rent can slow deposit savings, while higher interest rates can reduce borrowing capacity. That does not mean buying is impossible, but it does mean the plan needs to be more specific.

Practical ways forward

Some buyers are adjusting rather than waiting.

That might mean:

- Looking at different suburbs

- Considering a smaller or lower-maintenance property

- Exploring rentvesting, where appropriate

- Buying with a partner, friend or family member

- Getting pre-approval before starting serious negotiations

- Building a stronger savings record before applying

As identified in an article by Joel Pritchett, Tomii, a pro-active firm of buyer agents, rental yield is usually treated as an investor measure, but it can also help renters understand the gap between renting and owning in a particular market.

When rent rises and property prices soften or stabilise, the rent-versus-owning gap can narrow. That does not automatically mean buying is affordable. Buyers still need a deposit, borrowing capacity, purchase costs and a realistic repayment buffer.

But it may be the point where a renter should re-check their borrowing position rather than relying on assumptions from six or twelve months ago.

The biggest step is to understand your position today, not guess where the market might go.

If you are renting and trying to buy, the right question is not just:

“Can I buy now?”

It is also:

“Where can I buy safely, and what would the repayments look like after settlement?”

Get in touch if you want to see what you can borrow and what is realistic right now.

Plan Your Property Purchase:

Before Emotions Set Your Budget

Key message: Buying property is not just about finding the right place and getting the loan approved. A better purchase starts with a better plan — before you sign, bid or transfer a deposit.

Buying property can feel exciting, stressful and slightly overwhelming — sometimes all in the same hour. There is the search, the budget, the loan, the contract, the inspections, the settlement date and, somewhere in the middle of all that, the hope that you are making a good decision.

That is why a clear plan matters. Not because it removes every risk — it does not — but because it helps you slow down, ask better questions and avoid letting emotion make the decision for you.

I was prompted to prepare this article following receipt of a checklist, kindly supplied by Avanthi De Alwis, the Principal Solicitor at the conveyancing firm HDH Legal. As a conveyancer and also a licenced legal practitioner, Avanthi has put a lot of work into assisting her clients make the right decisions when they buy a property and her insights have proved invaluable.

Start with the buying plan

Before getting too deep into open homes and online listings, it helps to be clear on what you are actually trying to buy. Are you buying a long-term home, a stepping-stone property, an investment, or a home you may later keep as a rental?

That answer matters because it can affect the location, property type, budget, ownership structure, loan setup and future resale value. It also helps you set your walk-away rules early, which is important because emotion can push buyers beyond their comfort zone, especially at auction or after missing out a few times.

Know your real budget

Borrowing capacity is not the same as comfort. A lender may assess what you can borrow under their rules, but that does not automatically mean the repayment will feel comfortable in your household budget.

A better budget should include the full cost of buying and owning, not just the deposit and loan approval. This may include stamp duty or transfer duty, conveyancing costs, building and pest inspections, loan costs, moving costs, insurance, repairs, maintenance and a post-settlement cash buffer.

That last point matters. The goal is not to become property rich and cash poor on day one.

Check government support early

First-home buyers should check whether any grants, concessions or low-deposit pathways may apply before setting their final budget. These can make a meaningful difference to the funds required to complete, but eligibility depends on the buyer, property type, location and timing.

This may include support such as the Australian Government 5% Deposit Scheme, state-based first home owner grants, duty concessions, the First Home Super Saver Scheme and shared equity options where relevant. These rules can change, so they should be checked early and confirmed before relying on them.

Sort the finance strategy before making offers

A pre-approval can be useful, but it is not the same as formal approval. Before making serious offers, buyers should understand how much they can borrow, what deposit is needed, whether lenders mortgage insurance may apply, whether a finance clause is required and whether the property type suits lender policy.

The loan structure also matters. Depending on the buyer’s goals, this may include principal and interest, interest-only where suitable, fixed, variable, split loans, offset accounts or redraw facilities. The goal is not just to get approved; it is to structure the loan in a way that supports the buyer’s broader plan.

Get the right team around you

A property purchase usually involves more than one professional. Depending on the buyer and property, the team may include a mortgage broker, conveyancer or property lawyer, building and pest inspector, insurance broker or insurer, accountant, financial planner, buyer’s agent or property advocate.

Investors may also need a quantity surveyor and property manager. SMSF buyers need specialist SMSF, legal and lending advice before signing anything. Getting the right people involved early can help avoid problems that are much harder to fix later.

Do smarter due diligence

The property itself needs careful checking. This can include title, zoning, overlays, easements, covenants, flood or bushfire risk, owners corporation records, cladding risk, asbestos risk, contamination risk, heritage listing and unapproved works.

For units, townhouses and apartments, owners corporation records are especially important. Fees, minutes, insurance, disputes, defect reports and planned works can tell you a lot about future costs. For tenanted properties, the lease, bond, rent, condition report and property manager handover should be checked before settlement.

None of this is glamorous, but it is better to find the issue before you sign than after you own it.

Off-market properties can also be worth considering, especially when a seller wants a quieter sale or fewer public inspections.

But off-market does not automatically mean under-market.

It simply means the property is not being marketed in the usual public way. The buyer still needs to do the same homework: recent comparable sales, contract review, finance readiness, valuation risk and a clear walk-away number.

The risk is mistaking “not publicly listed” for “good value”. That is not always true.

Understand the contract before signing

The contract is not just paperwork. It sets out what each party must do, when it must happen and what can go wrong if deadlines are missed.

Buyers should check the finance clause, cooling-off rights, deposit rules, settlement date, fixtures and fittings, special conditions, GST issues where relevant, nomination rights, early access, sunset clauses for off-the-plan purchases and vendor termination rights.

A conveyancer or property lawyer should review the contract before signing. A verbal promise from an agent is not enough. If something is important, it should be properly written into the contract.

Prepare for settlement

Settlement may feel like the final administrative step, but it still needs active management. Buyers should confirm lender timing, sign loan documents promptly, review the settlement statement, complete a pre-settlement inspection and verify payment details through a secure channel.

Payment redirection fraud is a serious risk in property transactions. Do not rely only on email instructions when transferring money. The final inspection is also important because it gives you one last chance to check that the property is in the agreed condition and that included items are still there.

Different buyers need different checks

A first-home buyer may need more support around grants, pre-approval, deposits and auctions. An investor needs to check cashflow, rental demand, tax structure, land tax and landlord insurance. An upsizer or downsizer needs to think carefully about sale timing, bridging finance and settlement coordination.

An SMSF buyer needs specialist advice before signing anything. That is why one checklist can help, but the detail still needs to match the buyer and the property.

Final thought

Buying property is a major financial decision. The right plan can help you avoid rushed choices, missed costs and contract issues that only appear when it is too late.

Before you sign, check the numbers, the property, the contract, the loan and the settlement plan. It is not about making the process complicated; it is about being properly prepared.

Tax Depreciation Schedules:

What Property Investors Should Check Before Year End

Key message: If you own an investment property, a tax depreciation schedule may help your accountant claim eligible deductions for the gradual ageing of the building and some assets. The best time to get organised is before tax time, not when your accountant is already chasing documents.

I was reminded by Tuan Duong, Duo Tax, that as 30 June gets closer, many property investors start thinking about rent statements, loan interest, repairs, insurance and property management costs.

One item that can easily be missed is the tax depreciation schedule.

A tax depreciation schedule is usually prepared by a qualified quantity surveyor. It sets out depreciation and capital works deductions that may be available on an income-producing property. In simple terms, it helps your accountant work out what may be claimable for the building structure and eligible assets over time.

It is not a magic tax trick.

It is a practical report that helps your accountant claim what the rules allow.

And if you scroll to the end of this article, you will see a special offer for readers of our newsletter from Duo Tax. This may be especially relevant if you are aiming to finalise your 2025 tax return before the ATO’s 15 May final lodgement due date.

Why it matters

When people buy an investment property, most of the attention usually goes to the loan, rent, interest rate, suburb and purchase price. Fair enough — those things matter.

But depreciation can affect after-tax cash flow, and a good schedule can reduce guesswork for your accountant.

A schedule may help identify:

- Capital works deductions, such as eligible building structure and fixed improvements

- Plant and equipment items, such as eligible appliances, carpets, blinds or air-conditioning

- Renovation history that may still have claimable value

- Items that need to be treated differently for tax purposes

- Year-by-year deductions for future tax returns

The Australian Taxation Office (ATO) says capital works deductions are generally claimed over time, and capital works are commonly claimed over 40 years from when construction was completed.

New property versus established property

Brand-new properties often have clearer depreciation potential because the building costs, completion dates and new assets are easier to document.

Established properties can still be worth checking, especially if they have been renovated or improved. However, the rules are more limited for second-hand plant and equipment.

The ATO says that, in most cases, investors cannot claim a deduction for second-hand depreciating assets in residential rental properties after 1 July 2017.

That does not mean an older property has no deductions. Capital works, later renovations, common property items in strata complexes, and new assets you personally buy and install may still matter.

Renovating? Check before you start

Renovations are one of the main reasons to speak with your accountant and quantity surveyor before work begins.

Some costs may be treated as repairs. Others may be capital works or depreciating assets. Initial repairs are a common trap because fixing damage that existed when you bought the property may not be treated the same way as an ordinary repair that happens while you own and rent the property. The ATO notes that some repairs are capital in nature and must be claimed over several years, including some initial repairs.

Before renovating, it may also be worth recording items that will be removed or replaced. Photos, invoices and dates can make life easier later.

After renovating, the depreciation schedule may need to be updated.

What to gather before tax time

A tax depreciation schedule is only one part of your rental property records, but the better your records, the easier it is for your accountant to prepare your return.

Useful information may include:

- Settlement date

- Contract of sale

- Building age, if known

- Construction start and completion dates, if available

- Renovation invoices and descriptions of works

- Photos before and after major changes

- Strata records, especially for common area works

- Council approvals or building permits

- Details of new assets installed after purchase

- Dates when items were installed, removed or replaced

- Any plans for future renovations

These are the same practical records included in the checklist we have been preparing for property investors.

Do you need one before this tax return?

Maybe.

It is worth asking your accountant if:

- You bought an investment property during the year

- You converted a former home into a rental property

- You renovated the property

- You bought an established property with previous renovations

- You replaced assets such as carpet, blinds, appliances or air-conditioning

- You own an older property but are unsure whether anything is still claimable

- Your accountant has asked for better records

The cost of a schedule itself may be deductible, but the real question is whether the likely deductions justify the cost over the period you plan to hold the property.

The finance angle

A depreciation schedule does not directly make the bank lend more or change a lender’s borrowing-capacity formula.

But it can still help your broader investment position.

If depreciation and capital works deductions improve after-tax cash flow, that can reduce some of the pressure of holding the property. It can also help you plan your cash buffer, tax position and future loan strategy with your accountant and finance broker.

For property investors, cash flow is not just rent minus the loan repayment. It also includes tax, insurance, strata, maintenance, land tax, repairs, vacancies and future upgrades.

The practical takeaway

A tax depreciation schedule is not about being aggressive with tax.

It is about being organised and making use of rules that already exist.

If you own an investment property, now is a good time to check whether you have the right records ready for your accountant.

*** Duo Tax offer: a tax depreciation schedule at a reduced fee of $525 incl GST for those who respond to this newsletter before end of May 2026. ***

Tax Depreciation Schedules:

What Property Investors Should Check Before Year End

Key message: Australia does need more homes in the right places, but supply alone does not explain the housing affordability problem. We also need to ask whether our tax system has made existing housing too attractive as an investment asset — and whether that has come at the cost of lower home ownership for younger Australians.

I was prompted by an article in The New Daily to question the issue around housing supply Vs other factors which may be driving up house prices in Australia. The research produced some surprising results and led me to develop the thought piece below.

I have written a fuller article on this topic, including the supply argument, investor demand, capital gains tax, negative gearing, rent concerns and the intergenerational wealth gap.

Australia’s housing debate often comes back to one familiar line:

“We just need to build more homes.”

That sounds sensible.

And partly, it is.

Australia does need more homes in the right places. We need better zoning, more medium-density housing near transport, faster approvals and fewer construction bottlenecks.

But the data does not support a neat, supply-only story.

The bigger question is this:

Have we built a tax system that helps people buy homes as investment assets more than it helps people buy homes to live in?

That is an uncomfortable question, but it is the one we need to ask.

Supply matters, but it is not enough

Supply is part of the problem, especially in suburbs where people want to live but new homes are hard to add.

Some suburbs are effectively full under current zoning. Others have the transport, schools, jobs and local services people want, but not enough apartments, townhouses or smaller homes for the people who would happily live there.

So yes, supply matters.

But supply does not explain everything.

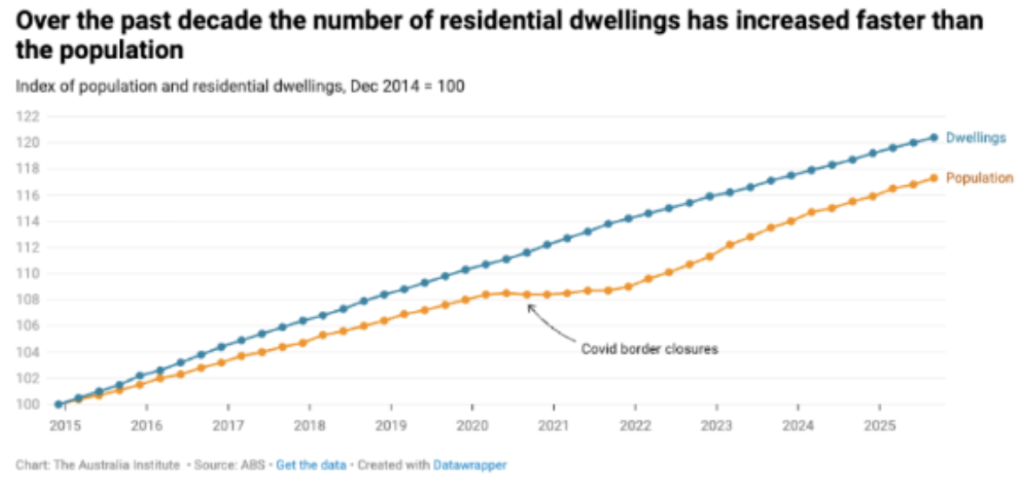

Over the past decade, Australia’s population grew by about 16%, while the number of residential dwellings grew by about 19%. Over the longer 2001 to 2021 period, population grew by about 34%, while dwellings grew by about 39%.

That does not mean there are no local shortages.

There clearly are.

It also does not ignore recent pressure from migration, smaller household sizes and weaker construction completions.

But it does weaken the simple claim that house prices have pulled away from incomes only because Australia failed to build enough homes.

Residential dwellings have increased faster than population over the past decade. This does not remove local housing shortages, but it does challenge the idea that Australia’s house price problem is only a supply problem.

The better answer is more layered.

Interest rates matter. Credit access matters. Migration matters. Planning rules matter. Construction costs matter. Government grants can matter too.

But tax settings also matter — and they have been doing a lot of heavy lifting in the wrong direction.

The market is not one market

This is where the supply argument needs some care.

The Australian housing market is not one single market. Conditions can look very different between cities, regions, suburbs and price points.

A suburb with limited land, strong schools, good transport and high owner-occupier demand can have a very real supply problem. A city with weak buyer confidence may soften at the same time another city is rising strongly because listings are tight and population demand is stronger.

That tells us something important.

Supply pressure is often local.

But tax settings are national.

That means supply can help explain why particular markets are expensive, or why particular suburbs remain tightly held. But supply does not fully explain why housing across Australia has become such a powerful investment asset over time.

For that, we need to look at the incentives.

The tax system changed the reward

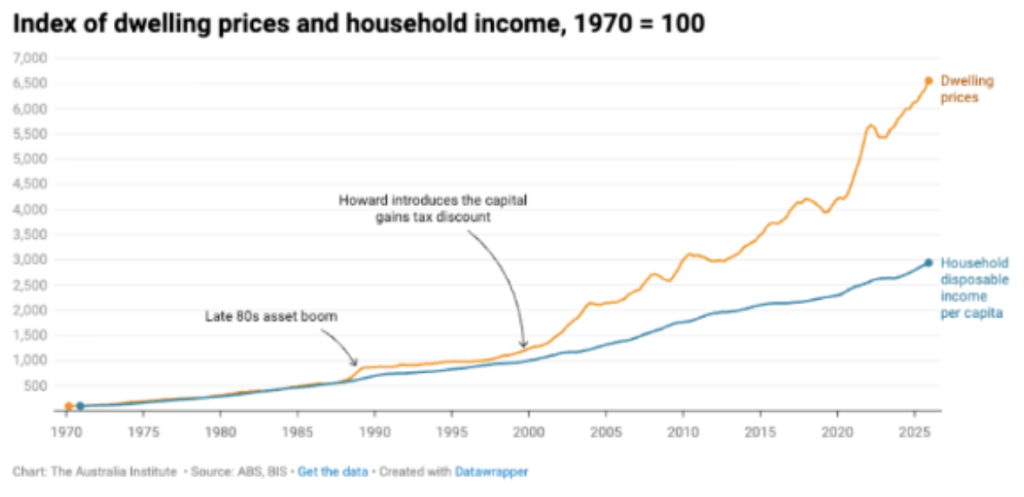

The capital gains tax (CGT) discount was introduced in 1999.

Before then, capital gains were adjusted for inflation. After the change, eligible individuals could generally discount a capital gain by 50% if the asset was held for more than 12 months.

That changed the reward for owning assets that produce capital growth.

Housing was an obvious winner.

Negative gearing then works alongside that system. In simple terms, some investors can claim rental losses against other income while waiting for a future capital gain — and that future capital gain may then receive discounted tax treatment.

That is not a small technical detail.

It changes behaviour.

It makes existing housing more attractive as a long-term investment asset.

Dwelling prices have risen far faster than household disposable income over time, with a clear breakaway after the late 1990s. The timing does not prove tax settings caused the entire shift, but it does show why the capital gains tax discount deserves serious attention.

The graph does not prove that tax settings explain everything.

They do not.

But it does show why the “just build more” argument is too simple. Once you look at the long-term gap between house prices and incomes, it is hard to ignore the role of incentives that reward capital growth.

Existing-property investment does not create a new home

This is the part of the debate that often gets blurred.

There is a big difference between:

An investor funding a genuinely new dwelling

An investor buying an existing dwelling and hoping for capital growth

The first can add to housing supply.

The second does not.

If an investor buys an existing property from another owner, Australia does not get an extra home. The ownership changes, but the number of dwellings stays the same.

That matters because tax settings often support both types of investment in a similar way.

If the goal is to create more housing, then it makes sense to ask whether the tax system should treat new supply differently from existing-property speculation.

Because if tax settings encourage investors to bid harder for existing homes, that does not solve the supply problem.

It changes who wins the bidding contest.

Too often, the person priced out is a first-home buyer.

This is not about blaming investors

This is not about investor bashing or saying investors are bad people (they’re not – and I’m not!).

Most investors are acting rationally under the rules available to them. If the system rewards capital growth, allows some losses to be deducted along the way, and then discounts the eventual gain, people will respond.

That is the point.

The problem is not that people respond to incentives.

The problem is the incentives.

A first-home buyer is usually trying to buy shelter.

An investor is often buying a tax-effective asset.

They may be bidding on the same property, but they are not playing the same game.

That is not a neutral outcome.

It is a policy choice.

The benefits are not evenly shared

The “mum and dad investor” line gets used a lot in this debate.

And yes, many investors are ordinary households.

But that does not mean the tax benefits are evenly shared.

The largest benefits generally flow to people with the largest gains and the highest marginal tax rates. Parliamentary Budget Office material has shown the top 10% of income earners receive about 82% of the CGT discount benefit, while the top 1% receive almost 60%.

That is a major fairness issue.

Older and wealthier Australians often already have the equity, income and borrowing capacity to invest. The tax system can then amplify that advantage.

Meanwhile, many younger Australians are trying to save a deposit while prices keep moving away from them.

That is not just a market issue.

It is an intergenerational issue.

Rentvesting is one example of how younger buyers are trying to work around the problem. It can be a smart individual strategy: rent where you want to live, and buy where the numbers make more sense.

But it is also a sign of the deeper issue. When people who want a home to live in feel pushed into becoming investors somewhere else first, the housing system is not working as cleanly as it should.

That may be rational at an individual level, but at a system level it shows how deeply property investment has become embedded in Australian wealth creation — even for people whose first preference may simply be to own a home to live in.

Is lower home ownership what we really want?

This is the bigger social question.

Home ownership has long been one of the main ways Australians build security. It gives people stability, helps families plan and gives retirees more options later in life.

It is not perfect, and not everyone wants or needs to own a home.

But if ownership keeps drifting further out of reach for younger Australians, we should at least be honest about the trade-off.

Do we really want a society where more people become long-term renters because the tax system has made existing housing more attractive to investors?

Do we want a system where older, wealthier Australians can use tax settings, equity and borrowing power to build more property wealth, while younger buyers are told to be patient and “just save harder”?

That does not feel like a neutral outcome.

It feels like a choice we have made without properly admitting what it costs.

The practical takeaway

The evidence does not say supply is irrelevant.

It says supply is not enough.

Yes, build more homes where they are needed.

Yes, fix planning.

Yes, support better construction and more housing near transport.

But also ask the harder question:

Why has our tax system made existing housing such a powerful investment asset — and has that helped push home ownership further away from the people trying to buy their first home?

That is the issue we need to face.

Because a housing system that rewards people for owning more property, while making it harder for others to buy even one, is not just a market outcome.

It is a community problem.

If you are trying to buy your first home and feel like the market is working against you, reply and I can help you understand your borrowing position.

Planning To Build?

Costs Are Changing

Key message: Building or renovating can still make sense, but rising costs mean the project should be tested before you commit. Scope, staging, budget, finance and contingency need to line up early — not after the drawings, quotes and emotions have taken over.

Construction costs were already under pressure, and new global pressures may add to the squeeze.

Recent inflation and building-cost data show that the cost of a new home has been rising faster again, after a period of relative easing.

For anyone planning to build or renovate, that matters.

It does not mean every project becomes unworkable. But it does mean your finance, contract, timeline and buffer all need to be checked carefully. With rates now higher as well, the borrowing structure and contingency need even more care.

What is happening on the ground

Builders and renovators are dealing with:

- Rising material costs

- Higher transport and fuel expenses

- Labour shortages

- Longer lead times for some inputs

- Less certainty around final project timing

That can make quoting, budgeting and finance approval more complex.

New dwelling costs are still rising, which makes early budgeting, staging and finance planning more important.

Test the project before you commit

As Audrey highlighted, in a rising-cost environment, the first decision is often not:

“Which loan do we need?”

It is:

“What are we actually building?”

That might sound simple, but it is where many projects become clearer.

A proper feasibility process can help test the project before the expensive commitments begin. That means looking at the scope, likely cost, site constraints, staging options, council issues, contingencies and finance timing before you move too far down one path.

Sometimes the answer is to build now.

Sometimes it is to stage the works.

Sometimes it is to renovate instead of rebuild.

And sometimes the right short-term decision is to pause, knowing the decision has been properly tested.

That may sound cautious, but it can be the difference between a project that works and a project that becomes stressful halfway through.

One of the big risks for homeowners is quote shock. A project can feel affordable in broad terms until the design, engineering, builder margin, consultant fees, contingency, temporary accommodation and finance costs are properly added up.

That is why the design plan, cost plan and finance plan need to speak to each other early.

A lender will not simply fund every extra idea because it is attractive or useful. The valuation, contract, borrower contribution, contingency and progress-payment structure all matter.

Where planning makes the difference

If you are thinking about building or renovating, it helps to plan for:

- A realistic cash buffer

- Possible delays

- Contract variations

- Progress-payment timing

- Valuation risk

- The gap between what a builder quotes and what a lender will accept

A construction loan is different from a standard home loan. Funds are usually released in stages as the build progresses, and lenders will look closely at the builder, contract, valuation and borrower position.

Construction loan or equity release?

There is also a finance-structure question to work through early.

Some projects need a construction loan. Others may be funded through an equity release against an existing property.

A construction loan is usually used where the lender needs to fund the build in stages. Payments are normally released as the project progresses, and the lender will usually want to review the building contract, plans, permits, builder details, valuation and progress-payment schedule.

An equity release loan is different.

This is where you borrow against available equity in your existing property and receive funds upfront or into a loan account, rather than through staged construction payments. This may be possible where your current home loan has been paid down, your property value has increased, and your loan-to-value ratio is low enough. In many cases, lenders may consider equity release up to around 80% loan-to-value ratio, subject to lender policy, servicing and the purpose of funds. The exact limits and requirements vary by lender, so this needs to be checked before relying on it.

Equity release loans can be useful for smaller renovations, staged works, design fees, deposits, consultants, or projects where a full construction loan may not be needed.

But it is not automatically better.

The right structure depends on:

- The size of the project

- Whether there is a fixed-price building contract

- Whether the work is structural or cosmetic

- Whether funds are needed upfront or in stages

- The available equity in the property

- The lender’s policy on renovation or construction purposes

- The borrower’s servicing position

- How much contingency is needed

The key point is that the finance structure should match the project.

A construction loan may give the lender more control over staged payments, which can be useful for larger builds. An equity release may be simpler for smaller or staged works, but it can also place more responsibility on the borrower to manage the budget and avoid cost blowouts.

Either way, the finance plan should be tested before the project is locked in.

That applies whether you are building a new home, adding a granny flat, renovating, staging works over time, or doing a larger project.

Before committing, it is worth asking:

- What problem are we trying to solve?

- Is the scope realistic for the budget?

- Could the work be staged?

- What contingencies are needed?

- How will the lender treat the project?

- What happens if costs move or the valuation comes in lower than expected?

The practical takeaway is this:

The opportunity may still be there, but the homework matters.

The goal is not to make the process harder. It is to make the decision clearer before the major commitments are made.

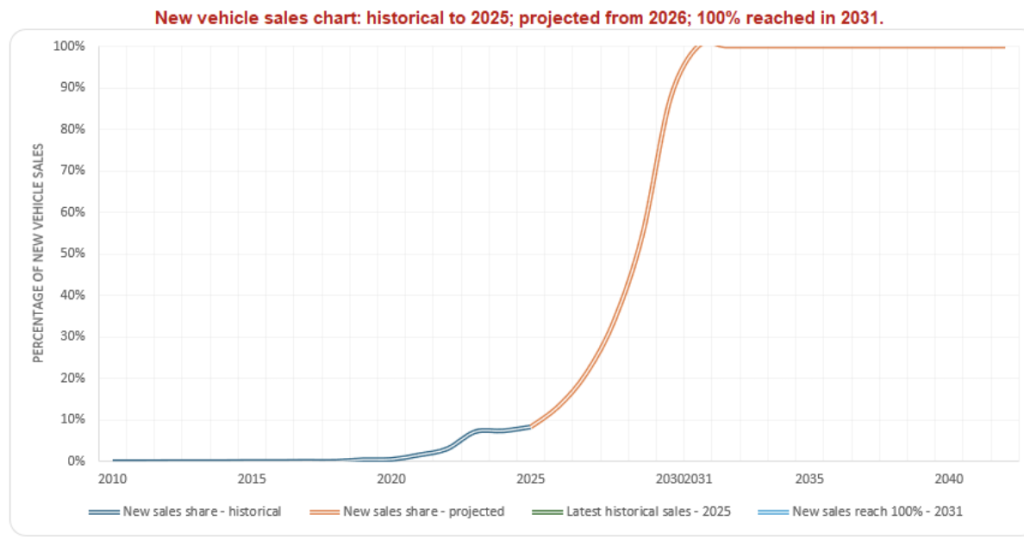

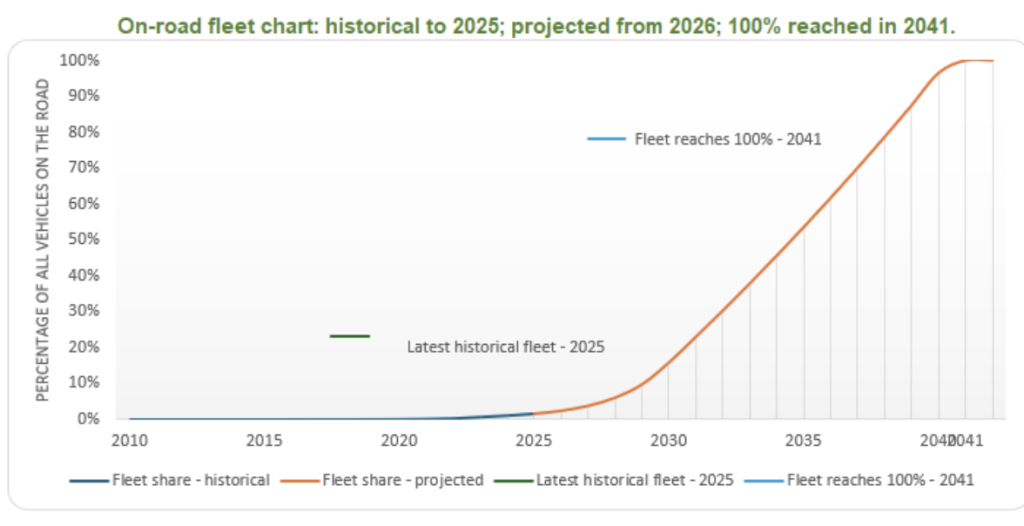

EV Sales Hit Record Share In March

Key message: EV sales may rise faster than many people expect, but the number of EVs actually on Australian roads will take longer to catch up. For households and businesses, this matters because vehicle choice can affect running costs, resale values, finance decisions and future cash flow.

Electric vehicles are no longer a fringe topic.

A recent article in The Driven argues that Australia may already be on track to reach around 75% to 80% EV new-vehicle sales by 2029 or 2030, based on the growth pattern in battery electric vehicle sales since 2010. The article notes that battery electric vehicle sales rose from just 10 vehicles in 2010 to 103,269 in 2025, with market share reaching 8.32% in 2025.

That does not mean most cars on the road will suddenly be electric.

There are two different numbers to watch:

- EVs as a share of new vehicle sales

- EVs as a share of all vehicles already on the road

The first number can move quickly. The second moves more slowly because petrol and diesel vehicles stay registered for many years.

This pattern is not unusual.

Technology shifts often feel slow at first, then suddenly obvious. Computers followed that path. Smartphones did too. Even the move from horses to cars in New York showed how quickly transport habits can change once a new technology becomes practical, affordable and widely available.

That is where the finance angle comes in.

For households, EVs may change the numbers on running costs, charging, servicing, resale value and loan affordability.

For businesses, the question is broader: when should the fleet be updated, how should vehicles be financed, and what happens if resale values for petrol and diesel vehicles change faster than expected?

None of this means every buyer should rush into an EV.

Charging access, price, range, towing, brand support, insurance and servicing still matter.

But the trend is worth watching closely.

EV technology is moving quickly, and it is not just about the car anymore. Solar, home batteries and charging systems are starting to overlap in ways that could change how households think about energy costs. China is a major leader in EV and battery development, but other countries are pushing hard too. One area to watch is bidirectional charging, where a compatible EV may be able to send power back to the home or even the grid. That could be a big shift, but it is not automatic yet — the vehicle, charger, installation, network rules and approvals all need to line up.

The real lesson is this: new sales can change quickly, but the road fleet changes more slowly. Smart finance decisions need to consider both.

Fuel Security And EVs:

Why Australia's Petrol Problem Is Bigger Than The Bowser?

Key message: EVs are often discussed as a climate or running-cost choice, but there is another angle worth considering: Australia is heavily exposed to global fuel supply shocks, and we no longer have the local oil and refining base many people assume we have.

Electric vehicles and petrol prices are usually discussed as separate topics.

They probably should not be.

When more Australians consider EVs, the conversation is not only about emissions, battery range or lower servicing costs. It is also about fuel security.

Petrol and diesel are still essential to our economy, but Australia’s ability to produce and refine its own liquid fuels is much weaker than many people realise.

A recent ABC article makes the point bluntly: Australia may be an energy powerhouse in coal and gas, but when it comes to oil, our reserves are limited and depleting. Bass Strait, once a major source of local oil production, is now nearing the end of its productive life.

Why “just produce more local oil” is not simple

When fuel prices rise because of global conflict or shipping disruption, the obvious reaction is to ask why Australia does not simply produce and refine more of its own fuel.

The answer is not that simple.

Australia does not have enough local oil to rely on for long-term fuel independence. The ABC article notes that Australia has about 1.3 billion barrels of proven or probable oil reserves, plus another 2.2 billion barrels of contingent reserves — oil that is known to exist but may not be economic to extract.

Even while Australia continues importing around 80% of its liquid fuels, the proven and probable reserves would run out in about seven years. Including all contingent reserves may add only about another two years, and some of those reserves may not be economic to extract.

So Australia may be rich in energy resources generally, but that does not mean we have enough local oil to shield motorists from global fuel shocks.

Queensland’s recent push to open up the Taroom Trough for oil exploration shows that governments are now taking the issue seriously. In February 2026, Queensland progressed petroleum and gas exploration in parts of the Taroom Trough by awarding exploration permits to industry, and further areas were released for competitive tender in March 2026.

That may help at the margin, but it does not change the bigger issue overnight. Current production is tiny compared with Australia’s daily fuel needs, commercial-scale production is uncertain, and deep drilling can be expensive. The attached review also notes the gap between current pilot production and Australia’s roughly 1 million barrels per day of liquid fuel consumption.

In plain English: local drilling may help, but it is not a quick or complete answer.

Refining is part of the problem too

Australia also has far less refining capacity than it once had.

Only two refineries remain: Ampol’s Lytton refinery in Brisbane and Viva Energy’s refinery in Geelong. Together, they provide about 20% of Australia’s liquid fuels. Other former refineries have been closed, converted into import terminals or decommissioned.

Queensland has also been talking to developers about a possible new refinery in Gladstone. The proposal from Resilient Energy Australia is for an $11 billion diesel-focused refinery, with a stated capacity of about 210,000 barrels per day.

That sounds significant, and it is.

But it is not the same as fuel independence.

The proposed Gladstone refinery would still need crude oil to refine. The company has said the facility would process heavy crude from overseas sources such as the Americas and West Africa, which reinforces the point: more local refining capacity may improve resilience, but it does not remove reliance on imported crude.

There is also the timing problem. A major refinery is not something that appears quickly. Even if approved, built and financed, it would be a medium-to-long-term project, not an immediate solution to current fuel pressure.

So the issue is not just:

“Why don’t we refine more fuel here?”

It is also:

“Where would enough crude oil come from, how long would it take, and at what cost?”

Fuel reserves are not as simple as they sound

There is also confusion around emergency fuel reserves.

The International Energy Agency requires member countries, including Australia, to maintain emergency oil stocks equivalent to at least 90 days of imports. But those reserves are not necessarily sitting here waiting to be used only by Australian motorists in a crisis. They are part of a coordinated international system designed to stabilise global oil markets.

Australia has also been running more on a “just in time” fuel model than a “just in case” model.

Queensland’s plan to unlock government-owned land near ports in Brisbane, Townsville, Mackay, Gladstone, Abbot Point and Bundaberg for fuel storage and potential refining proposals is a sign that storage is now part of the fuel-security discussion.

That is useful.

But again, storage is not the same as supply. It can help Australia hold more fuel locally, but the fuel still needs to come from somewhere, be refined somewhere, and move through global supply chains.

That is another reason slogans do not solve the problem.

Fuel security is not just about finding oil.

It is about reserves, refining, shipping routes, storage, pricing, government policy and global markets.

Where EVs fit into the bigger picture

This is where EVs connect back into the story.

EVs will not solve Australia’s fuel security issues overnight. Petrol and diesel vehicles will remain on the road for many years (15 plus years based upon the above graphs), and heavy transport, agriculture, mining and regional travel still rely heavily on liquid fuels.

But as more households and businesses shift part of their transport use to electricity, it may reduce exposure to imported fuel over time.

That matters because electricity can be generated locally, including through solar, wind, hydro, batteries and gas-backed generation. It is not risk-free, and it still needs grid planning, charging infrastructure and sensible policy.

But it is a different kind of exposure from relying heavily on imported liquid fuels.

For a household, the practical question is not simply:

“Should I buy an EV?”

It is also:

“What will my transport costs look like over the next five to ten years, and how exposed am I to fuel price shocks?”

For businesses, the question is broader again:

“When should we update vehicles, how should we finance them, and how do we manage fuel, electricity, tax, charging and resale risk?”

The practical takeaway

Australia’s fuel problem is not solved by slogans.

“Drill more” sounds simple, but our local oil reserves are limited, expensive to develop and not enough to provide long-term fuel independence.

“Build a new refinery” sounds simple too, but refineries still need crude oil — and much of that may still need to come from overseas.

“Store more fuel” can help, but storage does not create fuel.

EVs are not a magic answer either.

But they are part of a bigger shift in how Australia thinks about transport, energy costs and fuel security.

For households and businesses, the finance decision should not just be about the sticker price of the car. It should also consider running costs, fuel exposure, charging access, resale value, business use, tax treatment and future cashflow.

That is why this topic belongs next to the EV discussion.

It is not just about the vehicle you drive.

It is about the system that keeps it moving.

Thinking about purchasing an EV? Let’s have a chat and see how we can assist you make the shift when it is right for you.