Last week we issued the abridged version of the monthly newsletter for March.

For those who are time poor, it was a good opportunity to have a quick look at what’s happening in the world of property and finance.

However, it did not include all our usual deeper and grittier article content.

So, below is our full newsletter – with all the articles you love to love – plus more depth, more analysis and more “A ha, I see!” moments.

This month includes:

- Best interest rates at 2 March 2026

- Thinking of selling? Photo prep that sells – the simple steps that make buyers click (and inspect)

- First home buyers just surged – and that changes the timing conversation

- Contracts of Sale – don’t sign blind – the one check that can save you thousands

- Inflation is proving persistent – why that matters for property decisions

- Rate pressure may not be over – the ‘pass-through’ detail that really matters

- Investment buyer advocate update – Melbourne in the spotlight

- Investment property entity structures – this can matter more than the property itself

- Victoria’s new rental rules – landlords: don’t be caught out

- Car repairs just got more competitive – what that matters for car finance

Get a cuppa, relax and enjoy!

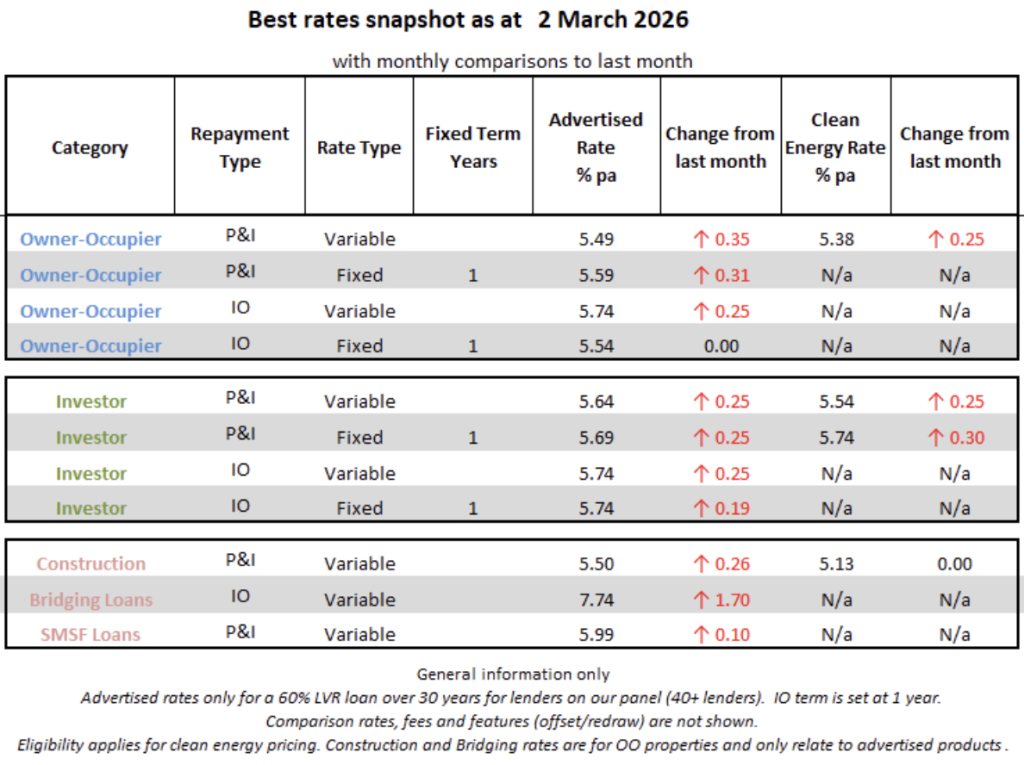

Best Interest Rates

Key comments and observations

- The headline move isn’t the whole story. Last month we noted the key is how each lender passes changes on across products and how pricing gaps widen or narrow.

- Practical takeaway: if your rate rose more than the headline cash-rate move, it’s often margin/funding and competitive positioning showing up in the “real world”, not just the RBA decision.

- This month’s snapshot shows that clearly: some categories moved more than others, even over the same period.

- Timing still matters for borrowers. As we said last month, the timing of lodgement and assessment matters because lenders assess borrowing power using the rate in place when the application is assessed (plus a servicing buffer).

- If you’re close to a borrowing limit, small repricings can change outcomes.

- Variable owner-occupier P&I moved the most in the “core” home loan categories.

- Owner-occupier P&I variable is now 5.49% (up 0.35% month-on-month). The clean-energy equivalent is 5.38% (up 0.25%).

- Fixed rates lifted again at the 1-year point. Owner-occupier P&I fixed 1 year is 5.59% (up 0.31%). Investor P&I fixed 1 year is 5.69% (up **0.25%). This aligns with last month’s point that fixed pricing often reflects wholesale funding and hedging costs in the background.

- Interest-only remains priced above P&I in most places. Owner-occupier IO variable is 5.74% (up 0.25%). Investor IO variable is 5.74% (up 0.25%). Owner-occupier IO fixed 1 year is 5.54% (unchanged), while investor IO fixed 1 year is 5.74% (up 0.19%).

- Clean-energy pricing is patchy and not readily available from most lenders, but where it shows up it can be sharp. In this snapshot, clean-energy rates appear for a few categories (not all). The standout is construction clean energy at 5.13% (unchanged), which is materially lower than standard construction variable (5.50%, up 0.26%).

- The outlier is bridging. Bridging (IO variable) is 7.74% (up 1.70% month-on-month). Bridging is specialist credit and it is not well-advertised. Price can move quickly, and the total cost is not just the rate — fees, timing, and exit plan matter. Plus, where offered, your current lender may be able to provide a more competitive rate.

- SMSF lending stayed relatively steady compared to others. SMSF P&I variable is 5.99% (up 0.10%). Whilst it’s still priced above standard owner-occupier lending, the month-on-month move here is modest.

If you would like a rate check, drop me a line –

just say ‘Rate Check’ and I will follow you up.

Photo Prep That Sells: The simple steps that make buyers click (and inspect)

Key Message: Most buyers meet your home online first. If your photos look bright, calm and spacious, you’ll typically get more clicks, more inspections, and a cleaner campaign run.

I have prepared this article with input from one of the current masters of real estate photography, video and drone footage – Brendan Rossmen, who along with Craig Sillitoe, is a co-owners of Pitch Digital. They do real estate photography, video and drone – the complete package. Plus, they compile all their finished product in a neat online-web-based folder for you and your agent to view (and, I am guessing it can even be distributed to potential buyers, such is the quality).

Of course, if you are staging your home for sale then a lot of this will done by the staging consultant but having said that, there are many good tips here which will help you make sure you are primed and photo-ready.

You’ve probably felt this shift yourself: marketing has become more visual, and buyers compare homes quickly. The camera is also brutally honest — it magnifies clutter, highlights glare, and makes small messes look like big problems. That’s why “photo prep” isn’t just about being tidy. It’s about helping the home show space, light, and flow.

In last month’s newsletter I talked about how “Clean and Light” work as a low-cost, high-impact lever in renovations.

This is the same idea — just focused on one specific moment that matters: shoot day.

What good photographers want (and why it works)

Pitch Digital’s checklist is a great guide because it focuses on the basics that consistently improve listing photos:

- Deep clean (floors, carpets, surfaces).

- Clean windows to maximise light.

- Declutter surfaces and remove personal items/photos.

- Open blinds/curtains and turn on all lights.

- Turn off ceiling fans, TVs and monitors (motion + reflections are photo killers).

- Remove extra furniture and position mirrors to avoid reflections.

Best-practice takeaway: the goal is neutral, bright, spacious — so the buyer’s brain can relax and imagine living there.

Room-by-room “do this, not that”

Exterior (your first impression photo)

- Close garage doors and remove vehicles from driveway.

- Mow/trim, clear paths, remove cobwebs around doors/eaves.

- Pack away hoses, toys, sports gear; consider a pot plant at entry.

Kitchen (the most judged room online)

- Clear counters — leave 1–2 “nice” appliances only.

- Add a bowl of fresh fruit (simple styling, no fuss).

- Remove fridge magnets/notes/photos; hide bins; no dishes in sink.

Dining

- Clear the table; add a simple centrepiece; straighten chairs evenly.

Living areas

- Clear shelves/TV stands; hide remotes; fluff pillows; remove toys.

- A couple of healthy plants can lift the feel (don’t overdo it)

Bathroom

- Clear vanity; remove shampoos/soaps; toilet seat down.

- Fresh towels; a small plant or simple soap works.

Bedrooms

- Make beds properly; keep bedside tables minimal.

- Remove personal photos; clear anything visible under the bed.

- Kids’ rooms: tidy shelves; remove wall stickers if they dominate the room.

Pets (commonly forgotten, always visible)

- Hide bowls and beds; vacuum pet hair; keep pets out during the shoot.

- Yard: clear pet waste and pet toys.

Don’t miss this: tell the photographer what to “hero”

This is a simple but powerful best-practice habit: call out special features you want captured (so they don’t get missed in the shoot flow). Brendan suggests flagging things like display shelves, fireplaces, pools or spas (clean and photo-ready).

The easiest shoot-day run sheet (low stress, high result)

If you want a smoother shoot and better photos:

- 48 hours before: declutter + remove personal photos

- 24 hours before: deep clean + glass + bathrooms.

- Morning of: lights on, fans/TVs off, beds made, benches cleared.

- On arrival: walk through the “hero features” with the photographer

It’s simple — but it’s the difference between “nice photos” and “buyers feel something.”

A note for agents

A good checklist helps agents get consistent results without guesswork. It’s not just the photography — it’s the system around it: preparation guidance, quality control, and making sure the hero features are captured. That’s how an agent’s marketing looks premium and the campaign runs smoother.

Like an intro to Brendan?

Just shoot me an email and I will put you in touch. He is not only a smart guy who is growing fast, he is also a nice guy to boot!

First Home Buyers Surged: And that changes the timing conversation

Key message: Entry-level competition can move faster than you expect. If you’re buying in 2026, the key is not just “can I get approved?” but “can I hold it comfortably if rates or life changes?”

The Australian Bureau of Statistics (ABS) reported new first home buyer loan commitments rose 6.8% to 31,783 in the December quarter 2025.

That’s a meaningful quarterly lift — and it’s usually a sign that more buyers have decided not to wait for “perfect conditions”.

What’s going on behind the numbers

- Affordability is pushing buyers to act in the bands they can still reach, rather than waiting for prices or rates to magically get easier.

- Low-deposit pathways including the federal government’s 5% Deposit Scheme (and 2% Scheme for single parents) can bring buyers forward in time (great if you’re ready; risky if you rush and overpay).

- Treasury expects more mortgage defaults may occur if higher rates place pressure on some borrowers. In other words, affordability buffers matter more than they used to.

Before you sign, consider this

Approval is one thing. Sustainability is another.

If rates rose by 0.50%, would your repayments still feel comfortable? Would your budget absorb insurance, maintenance and everyday costs?

To give a real example, on a $500K mortgage with principal and interest repayments for a 30 year term, a 0.5% increase in rates from 5.5% to 6.0% equates to an extra $159 per month – or $1,906 per year. It adds up. And if your mortgage was $1.0M, just double the numbers.

Sustainability questions are worth answering before signing anything.

I run those scenarios upfront, compare lender policy differences and make sure the strategy fits your income and risk tolerance – not just the headline rate.

Considering your first home this year? Let’s test your numbers properly before you commit.

Contracts - Don't Sign Blind: The one check that can save you thousands

Key message: Before you sign, a thorough contract review can prevent you buying a property with hidden legal or practical problems — and it can save you from expensive surprises after settlement.

I recently spoke with Dawn Barry of Skilled Conveyancing who has 42 years experience in conveyancing. She helps Victorian buyers and sellers ensure their contracts are carefully prepared so they can sign with confidence. Dawn’s practical, detail‑focused approach gives clients clarity about their rights and risks before they commit.

After the review, you’ll have the clarity and peace of mind you need to confidently sign your contract and move forward.

When you find “the one”, it’s tempting to treat the Contract of Sale as paperwork you sign so you don’t miss out. In reality, it’s the legal rulebook for your purchase. Once you sign, you’re committing to obligations that can be difficult (and expensive) to unwind.

The cooling-off myth (Victoria)

Many buyers assume the cooling-off period is their safety net. It can help, but it’s not a free “undo” button and it doesn’t apply in every situation.

Two important realities:

- It doesn’t apply to auctions. If you buy at auction, you sign immediately with no cooling-off.

- It’s not a free exit. Cooling off usually involves a financial penalty, and there are situations where cooling off may not apply depending on how the sale is run.

That’s why the best time to get advice is before you put pen to paper.

5 points to consider

1) A proper review is not a skim

An experienced conveyancer will review the Contract of Sale and the Section 32 (Vendor’s Statement) line by line to check:

- Exactly what you’re buying (and what you’re not)

- What’s been disclosed and what might be missing

- Special conditions that change the “standard” deal

- Your rights and timeframes: finance, building/pest, deposit, settlement, default

2) The Section 32 is not optional paperwork

The Section 32 is meant to disclose key information about the property and the Title so you understand what you’re committing to. It may include things like easements, restrictions, zoning, outgoings, and Owners Corporation information (if relevant).

If the Section 32 is incomplete or unclear, it can materially change your risk.

3) Special conditions can quietly remove buyer protections

This is where many buyers get stung. A review can flag clauses such as:

- Early release of deposit requests

- Harsh default interest or penalty wording

- Off-the-plan timing clauses, including sunset clause risks

- Clauses that favour the vendor in a way that isn’t obvious at first glance

Also, as my experience has taught me, ‘words matter’. You need the special conditions which are designed to protect you (subject to finance, building and pest inspections being the most common ones), worded correctly. I had one client whose Conveyancer did not properly vet the special conditions, and my client had to jump through all sorts of hoops to avoid losing her deposit and being forced to complete the sale.

4) “Property reality” can differ from the paperwork

Reviews often uncover issues such as:

- Unapproved structures or renovations

- Boundary or encroachment issues

- Flood overlays or notices you didn’t expect

- Owners Corporation rules or costs that don’t suit you (pets, renovations, short-stay)

Catching these before you sign gives you the option to negotiate, walk away, or proceed with eyes open.

5) Timing matters: private sale vs auction

Private sale or tender: Best practice is to review before signing, so you can negotiate terms and add protections like subject to finance or building and pest.

Auction: If you win, you usually sign immediately with no cooling-off. That means the contract review needs to happen well before auction day.

A small cost for major protection

A pre-signing contract review is best seen as risk management, not an optional extra. The cost is small compared with:

- The expense of trying to unwind a bad purchase (if that’s even possible)

- Unexpected repairs, disputes, or Owners Corporation surprises after settlement

- Losing leverage because you signed before you fully understood the terms

Next steps

Whilst these steps apply to Victoria, the other states and territories have similar regimes.

1. Get the contract and Section 32 reviewed before signing

2. Confirm any conditions you need are written correctly

3. Only then commit

If you would like an introduction to Dawn, let me know and I can organise this for you.

We have also prepared a Contract Review Checklist for Residential Property Buyers (Victoria – other states will follow).

Let me know if you would like a copy.

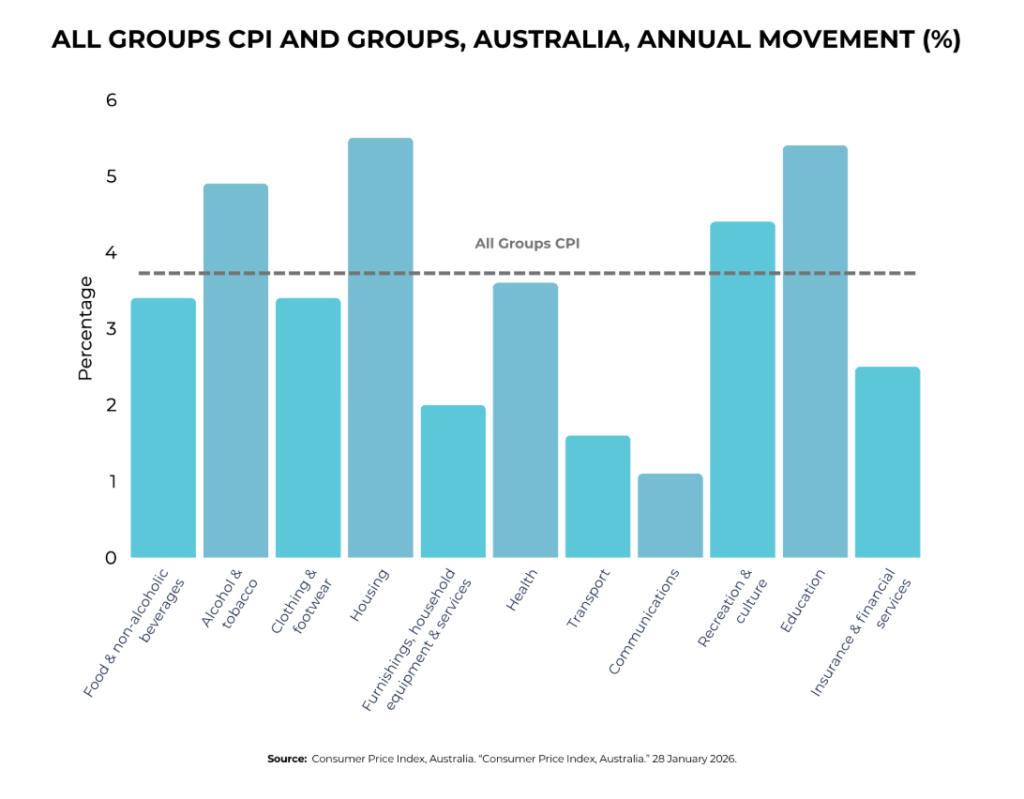

Inflation is Still Proving Persistent: Why that matters for property decisions

Key message: When inflation stays elevated, it keeps pressure on interest rates and household budgets — which flows into borrowing power, confidence, and how competitive buyers feel.

The ABS reported inflation (CPI) was 3.8% in the 12 months to January 2026, unchanged from December.

Two practical takeaways:

- Housing remains a major contributor to annual inflation (up 6.8% over the year in the ABS breakdown).

- Underlying (trimmed mean) inflation is 3.4%, still above the Reserve Bank of Australia’s (RBA) 2–3% target band.

What’s going on behind it

Inflation isn’t just a headline number. It reflects how:

- Businesses are pricing.

- Consumers are spending.

- The labour market and capacity constraints are behaving

The RBA’s own language is that inflation is expected to remain above target for some time, and its February 2026 Statement on Monetary Policy points to underlying inflation staying above the 2–3% range until early 2027.

Even though some of these pressures are seen as short-lived, policymakers also pointed out that:

- Household and business demand has picked up more than they previously thought.

- Capacity constraints are biting harder than expected.

- The labour market is still tight.

Put simply, parts of the economy are still running fairly hot.

What this means for borrowers

If you’re planning a purchase, refinance or review this year, it’s worth factoring in the bigger picture — because inflation pressure is one of the key reasons rates can stay higher for longer.

That environment influences confidence, lending conditions and long-term planning.

If you’re planning a purchase, refinance or review this year, now’s a good time to factor in the bigger picture.

Rate Pressure May Not Be Over: The pass-through detail that really matters

Key message: The headline cash rate move is only part of the story. What matters is when your lender passes it through, and what rate is used when your application is assessed.

What’s going on

Lenders don’t always move on the same day, and not always in the same way across all products. Some publish effective dates weeks later.

That means:

- Your borrowing power can shift depending on when the application is assessed, and

- Small pricing gaps between lenders can widen or narrow quickly.

How to stay ahead

- Review your household buffer, not just today’s repayment.

- Factor in possible future increases, not just current rates.

- Make sure your loan structure gives you flexibility if conditions tighten (offset, redraw, IO vs P&I strategy where appropriate).

As many of you may know, well-structured offset accounts whilst avoiding funds hitting savings accounts is one of the smartest ways to ensure you are keeping your interest costs to a minimum

If you’d like to stress-test your loan against possible future rises, contact me and I’ll help you map out a practical plan.

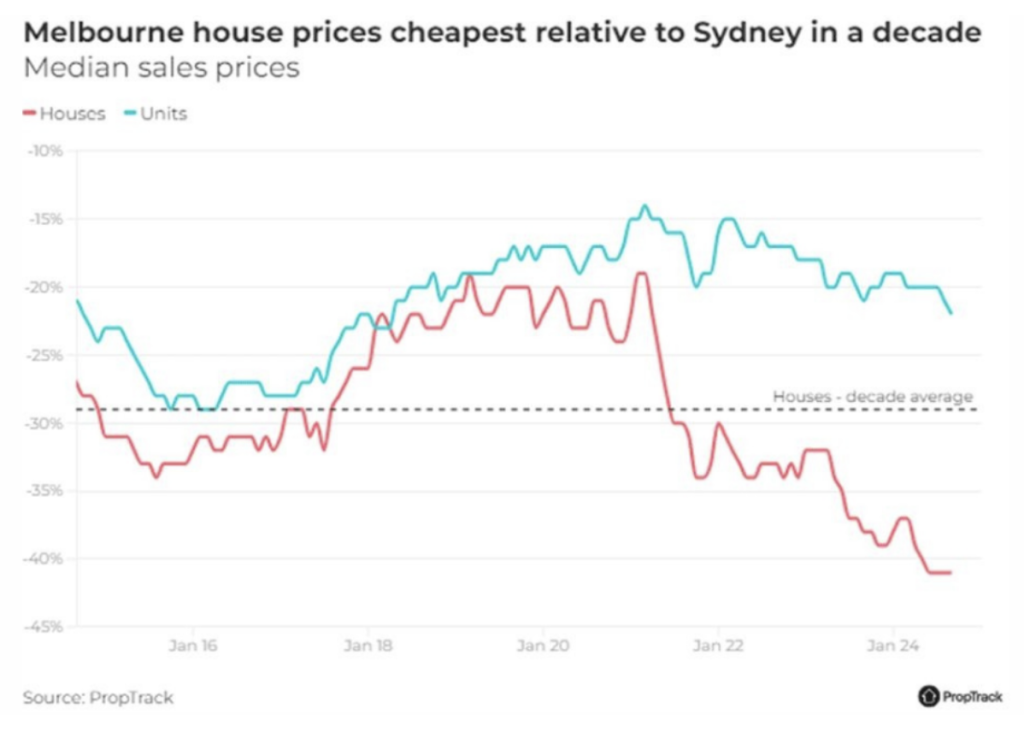

Investment Buyer Advocate Update: Melbourne in the spotlight

Key message: If you’re building a property portfolio, the biggest wins often come from getting the right market at the right point in its cycle — not just picking a nice property in your own backyard.

Joel Pritchett is a young (well, younger than me), smart guy in the investment property space. He is a Director and Head of Strategy for Tomii Buyers Agents. Along with his brother, I have tapped into his wisdom.

Buying interstate vs staying local

Australia has 15,000+ suburbs and they don’t move together. One state can go sideways for years, then surge, while another cools off. That’s why experienced investors often look outside their home state when the numbers stack up.

A helpful lens is “total runway” — what’s already happened (recent growth) and what could plausibly happen next (growth potential). In plain English: don’t chase last year’s winners just because they were hot — look for markets where the next few years have a better chance of delivering steady, boring growth.

What’s going on behind the “Melbourne value” conversation

One reason Victoria is back in the conversation is the relative value gap between Sydney and Melbourne, and the fact that buyer behaviour is now being shaped heavily by affordability bands.

A big driver of demand in Victoria is the sub-$950,000 segment in Metro Melbourne (including Geelong). That price point matters because it lines up with key first home buyer thresholds and incentives, so it’s where a lot of the “real” buyer competition tends to show up. In contrast, premium suburbs can feel slower when borrowing capacity is tighter and buyers become more cautious.

Demand isn’t evenly spread — it’s concentrated

Right now, the market isn’t moving as one. What we’re seeing is “two-speed” behaviour:

Sub-$950,000 pockets are typically seeing stronger enquiry because they’re where first home buyers and upgrader budgets can still work.

Premium suburbs can struggle more, because discretionary buyers are more rate-sensitive and often have more choice (or simply wait longer).

This is why “median price” headlines can feel confusing. The action is often happening in specific price bands, not evenly across a whole city.

Best practice: when buying interstate is smart (and when it’s a headache)

Buying interstate can be a great move when you treat it like a process, not a punt.

It’s usually smart when:

- You’re targeting a market with good runway (not just recent hype).

- You can buy an asset with multiple levers, rather than relying on growth alone. Examples include corner block/subdivision potential, granny-flat potential, cosmetic uplift, and enough yield to support cashflow.

- Your finance plan supports the holding period (buffers + cashflow).

It becomes a headache when:

- You buy remotely with weak due diligence (“looks good on a spreadsheet”).

- You ignore differences in tenancy rules, land tax, insurance, and council planning between states/regions.

- Your lending assumptions don’t match reality (valuations, postcode appetite, documentation, servicing buffers).

The “Swiss Army Knife” property idea (why it matters)

When borrowing capacity is tight, “one-trick” properties become riskier. A more resilient approach is to target a property that gives you options later — a Swiss Army Knife property.

That might be a home where you can:

- Add value with a cosmetic uplift

- Improve rental return

- Explore a future secondary dwelling (where permitted)

- Consider subdivision potential (where permitted)

The best-practice lesson is simple: if your plan relies only on market growth, you’re exposed. If your property has more than one way to win (cashflow, uplift, optionality), your plan is usually more robust.

A practical checklist before you buy interstate

1) Market and suburb

- What’s the cycle position (has it already run hard, or is it early)?

- What’s driving demand (jobs, infrastructure, population, lifestyle)?

- Is demand concentrated in certain price bands (like sub-$950k), while other segments lag?

2) Property fundamentals

- Is it a “one-trick pony”, or does it have levers (reno, subdivision, secondary dwelling, zoning upside)?

- If you’re assuming subdivision/granny-flat potential: have you checked overlays, minimum lot sizes, easements, services, bushfire/flood constraints?

3) Cashflow and buffers

- Run the numbers at +0.50% interest rate and with realistic vacancy/maintenance.

- If relying on rent, verify local rental demand and realistic rents (not best-case).

4) Lending reality

- Is the property type and location straightforward for valuation and approval?

- Do you have the right documents ready (especially self-employed or trust income)?

5) Management and execution

- Who is your “eyes on the ground” (buyer’s agent, trusted local PM, independent building/pest)?

- What’s the plan if timelines blow out (reno delays, council delays, tenancy gaps)?

BIR Finance takeaway

Interstate buying isn’t automatically smart or dumb. It’s smart when it’s deliberate: the right market, a property with levers, and a finance plan that can ride out noise.

And if you are staying local, don’t ignore where demand is actually concentrated. In Victoria, a lot of competition is showing up in the sub-$950,000 band, while premium markets can be softer — which can create both opportunity and risk depending on your strategy.

If you’re considering an interstate purchase or a Melbourne/Geelong buy, book a time with me and we’ll stress-test the numbers and the timing — so the property strategy and the lending strategy match.

Investment Property Entity Structures: This can matter more than the property

Key message: The entity type which is the purchaser on a contract can significantly influence your tax, land tax, asset protection, flexibility, and borrowing options for years to come — and can be expensive to change later due to potential CGT and stamp duty. Before you sign a contract, make sure you have obtained professional advise as to the entity which is purchasing the property.

Swati Gupta is a Registered Tax Accountant and founder of IX Advisory. When it comes to property and investments, she knows her stuff. And if she doesn’t know the answer, Swati will research the issue and provide a considered, evidence based view. I like her style!

Legal entity structures are important

In simple terms, “structure” means the legal ownership entity used to buy a property. Common examples include you (purchasing in your own name), joint names, a family trust, a company, or an SMSF (self-managed super fund).

Each structure can change the outcomes for:

- Tax (now and later)

- Land tax (ongoing holding costs)

- Asset protection (risk exposure)

- Flexibility (family and income changes over time)

- Borrowing (documents, guarantees, and lender policy)

The key point

Once you buy, changing the ownership structure later is usually costly, because it can trigger capital gains tax (CGT) and stamp duty/transfer duty (rules vary by state/territory). That’s why it’s worth thinking about before you sign.

What to think about before you buy

1) Tax today vs tax later

A property might create deductions now (for example, where deductible rental costs exceed rent received), but a taxable capital gain later when you sell.

What matters is:

- Who earns the rent (and claims the deductions).

- Who is taxed on the gain when the property is sold.

- Whether the structure suits your broader plan (income, family, retirement).

Key takeout: A structure that looks “tax effective” in Year 1 can become expensive or inflexible by Year 10 if your circumstances change.

2) Land tax and portfolio growth

Land tax often surprises investors — especially once they own more than one property.

Land tax is:

- State/territory based.

- Affected by thresholds, rates, and surcharges.

- Sometimes different depending on whether the owner is an individual, trust, or company

Key takeout: Even if your first property looks fine, the second or third can change your land tax outcome significantly — so think ahead.

3) Risk and asset protection

If you’re a business owner, director, or professional, owning property personally can increase exposure if something goes wrong in business.

A structure can help separate assets and risks, but it’s not a “set and forget” solution. The benefit depends on correct setup and your broader legal and tax position.

4) Flexibility for the future

Over 10–30 years, incomes change, families change, and retirement planning becomes real.

Some structures may provide more flexibility for:

- Managing income and tax over time.

- Planning for succession and estate outcomes.

- Adjusting to life changes (new partner, time out of work, adult kids, etc).

5) Borrowing implications

From a lending perspective, structure can affect:

- How income is assessed (especially trust income).

- What documents are required (more moving parts = more paperwork).

- How liabilities and guarantees are treated (policy varies).

This isn’t inherently ‘good’ or ‘bad’ — it just means you want your structure and lending strategy aligned early, so you don’t paint yourself into a corner.

Using your SMSF

Buying property in a Self Managed Super Fund (SMSF) can work in the right circumstances, but borrowing is only allowed in limited situations, usually via a Limited Recourse Borrowing Arrangement (LRBA), and there are strict compliance rules.

Two common “gotchas”:

- Residential property in an SMSF cannot be used for personal or family living purposes under the usual ATO rules.

- Related-party arrangements have specific rules (and commercial property is a different discussion again).

If SMSF property is on the table, get advice early — and definitely before any contract is signed.

State tip

Because land tax and duty are state/territory matters, here are a few general pointers to discuss with your accountant and broker.

Every state and territory has its own land tax rules – and they can change – so always check your local rules.

Borrowing + real-world practicality

From the lending side, structuring isn’t just a tax conversation — it can change how smooth (or painful) your finance journey is.

Points to note:

- Structure can change your borrowing options. Some ownership types can mean extra steps, extra documents, or different assessment rules — so it’s worth checking early, not after you’ve signed.

- Align structure with the next 5–10 years. If you might refinance, upgrade, buy again, or restructure business income, the “best” structure today should still work in your next chapter.

- Plan so you avoid expensive reversals. A structure that doesn’t fit later can be costly to unwind due to duty/CGT triggers — so a short planning conversation now can save real money later.

If you want, we can work with your accountant to sanity-check the proposed structure against your lending plan — so the tax strategy and the finance strategy match.

Practical takeaway

Property investing isn’t just a property decision — it’s also a structuring decision with a property attached. Getting it right upfront can have a lasting impact on tax, land tax, risk, flexibility, and borrowing options.

Before you sign, ask your accountant:

- Who will be taxed on rent and any future capital gain?

- If the property runs at a loss, who can use the deductions?

- How will land tax apply over time in your state — especially if you buy again?

- Do you need asset protection, and what’s realistic for your situation?

- Does the structure still work if incomes change or family circumstances shift?

- Will the structure support your borrowing plans, and what extra documents will be needed?

An intro to Swati

If you would like to have a chat with Swati, just let me know – she is a real whiz in this area but what I particularly like about Swati is that if she doesn’t know something, she will research it to get the right answer for you.

Victoria's New Rental Rules:

Landlords: Don't be caught out

Renting is now a longer life stage for more Australians, not just a quick stop before buying. At the same time, cost‑of‑living pressure and low vacancy rates make it harder for renters to push back when a property is unsafe, sub‑standard or when the application process turns into a bidding war.

Across Australia, the trend is towards clearer minimum standards, safer homes and less “game‑playing” in rental applications. Victoria has moved early and hard on some of these changes – especially the rule that a property must meet minimum standards before it’s advertised, not just before keys are handed over.

From 25 November 2025, the reforms aim to:

- Lift minimum safety and amenity.

- Stamp out “grey area” practices such as rent bidding.

- Make compliance easier to verify through clear obligations and penalties.

Further minimum standards start in December 2025, with additional energy‑efficiency standards phasing in from March 2027.

I spoke to three professionals in the investor property industry to seek their views on the changes and reforms. Not surprisingly, there was support but also caution as to the unintended consequences.

Kaz Marker, Marker Realty, is a highly regarded Real Estate Property Manager whose business focuses solely on the rental market. She believes it is important for those in the industry to recognise that things have changed. “Owners need to protect their investment and stay on the right side of the law — every time.”

Trish Moore, Hidden Gems Property Scouts, a Buyer Advocate, was of the view that whilst minimum rental standards are important, overly rigid enforcement with massive fines may prove counterproductive. “If a small fix like a showerhead blocks advertising, enforcement becomes counter-productive. Go after poor operators — don’t scare responsible landlords out of the market.”

Yanal Shyamji, Triple Zero Constructions, works for many real estate property managers as well as landlords, fixing and maintaining both home owners’ and investors’ properties . He is an ace renovator, and he likes to make sure everything is done ‘just right’. Yanal’s observation: “Downtime is expensive. Proactive maintenance keeps a rental compliant and ready to re-let quickly.”

Top 10 costly traps (and penalties)

Please note: the penalties are shown using the 2025–26 Victorian penalty‑unit value; Consumer Affairs Victoria can also issue lower on‑the‑spot fines, and amounts can change.

1) Advertising a property that doesn’t meet minimum standards

- Obligation: The property must meet the prescribed minimum standards before it’s advertised.

- Max penalty: $12,210 (individual) / $61,053 (company).

- Hidden cost: rush repairs, compliance checks, vacancy, re‑advertising, tenant disputes.

The big risk is assuming you can hand over keys and “fix it later”. Under the Residential Tenancies Act 1997 (Vic), the rental provider must ensure minimum standards are met on or before the day the renter moves in – and now effectively before the listing goes live.

If standards aren’t met, renters may be able to: end the agreement before moving in without fees, or move in and request urgent repairs (and in some cases organise repairs under $2,500 and seek reimbursement if you don’t respond). VCAT can also divert rent to a special account until issues are fixed, turning “we’ll sort it after move‑in” into vacancy, urgent trade call‑outs, reimbursements and a dispute.

2) Rent bidding / taking more than the advertised rent

- Obligation: Advertise a fixed rent; do not solicit or accept offers above that figure.

- Max penalty: $12,210 (individual) / $61,053 (company).

- Hidden cost: refunds, regulator attention, delays and reputational damage.

3) Taking more than one month’s rent in advance

- Obligation: You must not require – or accept – more than one month’s rent in advance if the weekly rent is $900 or less.

- Max penalty: $12,210.

- Hidden cost: repayments, ledger corrections, disputes.

4) Charging an excess bond

- Obligation: You must not demand or accept a bond of more than one month’s rent when rent is $900/week or less.

- Max penalty: $12,210.

- Hidden cost: refunding the excess, re‑issuing paperwork, disputes.

5) Not giving the renter the signed condition report before move‑in

- Obligation: Give the renter two signed copies (or one electronic copy) of the completed condition report before they move in.

- Max penalty: $5,087.

- Hidden cost: harder bond claims, more VCAT risk, arguments about “existing” damage.

6) Not giving the renter a signed copy of the agreement within 14 days

- Obligation: Provide a signed copy of the rental agreement within 14 days.

- Max penalty: $5,087.

- Hidden cost: uncertainty over terms, admin clean‑up, weaker VCAT position.

7) Not lodging the bond within 10 business days

- Obligation: Lodge the bond with the Residential Tenancies Bond Authority (RTBA) within 10 business days of receiving it.

- Max penalty: $30,526.

- Hidden cost: complaints, refund pressure, reputational damage and potential regulator interest if it’s systemic.

8) Entering the property without following the rules

- Obligation: Only enter in line with the Act (proper reason, notice and process).

- Max penalty: $12,210.

- Hidden cost: compensation, VCAT orders limiting entry, repeat inspection costs.

9) Not providing proper rent receipts and records

- Obligation: If rent is paid in person, receipt immediately; otherwise keep and provide records and receipts as required.

- Max penalty: $5,087.

- Hidden cost: arguments over arrears, extra admin, weaker evidence trail.

10) Mishandling renter information

- Obligation: Take reasonable steps to protect renter information and destroy or de‑identify it within required timeframes.

- Max penalty: $12,210 (individual) / $61,053 (company).

- Hidden cost: breach response, IT work, complaints and reputational fallout.

How smart landlords will stay out of trouble

Most penalties come from poor process, not bad intent. A simple compliance folder per property – backed by a switched‑on property manager – can save you a lot of money and stress.

- Do a minimum‑standards check two to three weeks before advertising.

- Book trades early and keep dated invoices and photos.

- Re‑check the property the day before move‑in.

- If something slips, email the renter straight away, agree a fix, and consider whether the start date needs to move.

- Keep dated photos, safety certificates, the signed condition report and lease, the bond‑lodgment receipt, entry notices and a detailed rent ledger and receipts together.

Landlord checklist

If you’d like a one‑page tick‑box compliance checklist to give your property manager (or to keep in your own file), reply “VIC checklist” and I’ll send it through.

This is general information only – if you need advice about a specific property, I can connect you with someone who can help – or, you can reach out to Kaz, Yanal or Trish.

Car Repairs Just Got More Competitive: Why that matters for car finance

Key Message: The “true cost” of a car isn’t just the interest rate — it’s servicing, maintenance, insurance, depreciation, and how competitive repairs are.

A federal review of Australia’s “right to repair” settings found the scheme has been associated with a $2.4 billion increase in automotive industry turnover annually, and that consumers have more choice and fewer barriers when servicing modern vehicles.

What’s going on behind it

When independent workshops can access repair information more fairly, it tends to:

- Increase competition

- Improve service options outside dealer networks

- Reduce “single-channel” pricing power over time

That won’t make every repair cheap — but it can shift the long-run ownership equation, especially if you service properly and keep records.

The hidden costs most buyers miss

When you finance a vehicle, the real cost isn’t just the loan. It includes:

- Servicing and maintenance

- Insurance

- Depreciation

- The cost of downtime (and unexpected repairs)

This matters even more for:

- Balloon payment loans

- Novated leases

- Anyone planning to sell within 3–5 years

I assess vehicle finance through a total-cost lens, so you’re not surprised by ownership expenses later.

Planning an upgrade? Let’s look beyond the interest rate. Reach out and I’ll run a full cost breakdown before you commit.