If you’ve been watching property prices Australia and thinking, “Surely prices can’t rise when interest rates are high,” you’re not alone. It sounds like common sense. But Australia’s housing market doesn’t always behave the way people expect — and history is a good reminder not to base big property decisions on one factor alone.

When property growth defies “common sense”

Many people assume the rule is simple:

Higher interest rates should slow borrowing, which should slow price growth.

Sometimes that happens. But a long-run view of Australian housing results shows something more interesting: some of the strongest growth years occurred in conditions that most of us would expect to cool the market.

Research commentary from Cotality puts it plainly: home values can surge when you least expect it.

The standout years

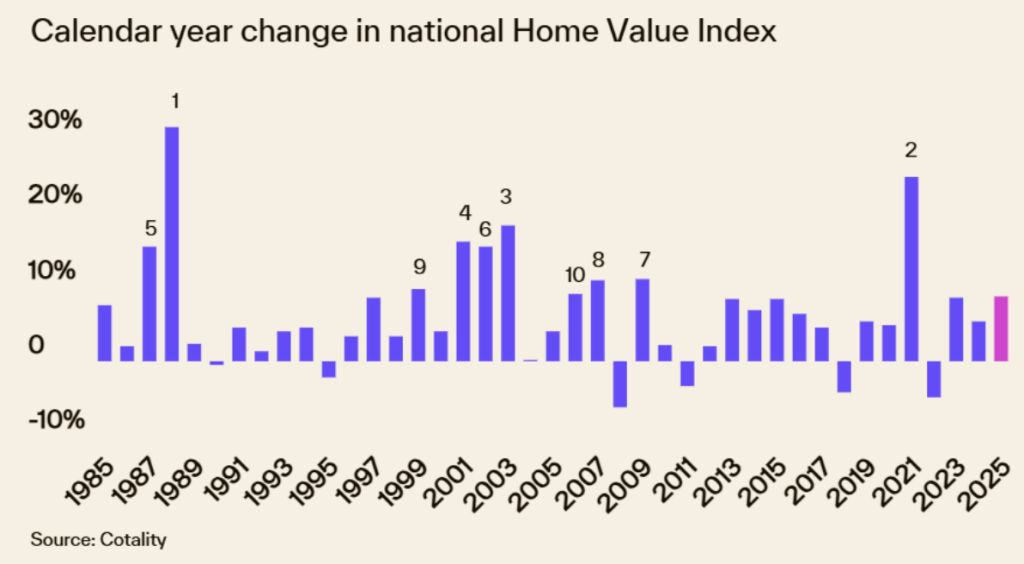

Cotality’s strongest calendar-year growth results over the past four decades include:

1988: +31.2% (with interest rates near 15% and rising)

2021: +24.5% (during the pandemic and closed borders)

2003: +18.1%

2001: +15.9%

1987: +15.3%

And 2025 still ranked strongly: Cotality’s Home Value Index rose 8.6% across 2025, making it the 11th highest calendar-year gain over the last 40 years.

When property growth defies “common sense”

The big takeaway from the data is that interest rates are only one lever. Housing outcomes are often shaped by a mix of forces, including:

Fiscal settings and confidence

When households feel more secure — and when government settings support spending power — demand can stay stronger than expected.

Credit availability

How easy it is to get a loan matters just as much as the rate itself. Lender appetite, assessment settings, and the way servicing is calculated can all expand or shrink borrowing capacity.

Migration and population growth

More people means more demand for housing and rentals. Even when migration normalises after a surge, the flow-on impacts can stick around.

Supply constraints

If there aren’t enough listings, or building capacity is tight, buyers end up competing harder for fewer homes.

Shocks

Big events (global crises, policy changes, sudden sentiment shifts) can change behaviour quickly — and not always in a neat, predictable way.

This mix helps explain how two very different periods (like 1988 and 2021) could both produce unusually strong growth.

A “calm down” stat (with a reality check)

Cotality also notes that over the past 40 years there were only six periods where home values fell.

That doesn’t mean prices can’t drop — they can, and they do. But it’s a reminder that broad downturns have been less common than many people expect, especially when viewed across long time frames.

What this can mean for 2026

Early thinking is that 2026 may be a softer year after a strong 2025. Affordability pressures and uncertainty around rates can take some heat out of momentum.

At the same time, credit settings still matter. For example, the mortgage serviceability buffer remains in place, and the broader stance from regulators can influence whether credit remains available or tightens quickly.

In plain English: if credit doesn’t suddenly dry up, the market can stay more resilient than the headlines suggest.

The practical takeaway

This isn’t a message to ignore interest rates.

It’s a message to zoom out.

Rates matter — but the market is often moved by the bigger bundle:

Supply

Credit policy

Migration and demand

Household confidence

If you’re making a property decision, focus on what you can control

Your borrowing buffer: How comfortable repayments feel, not just “can you get approved”

Your holding costs: Especially if you’re an investor

Your time horizon: Short-term noise matters less if your plan is long-term

Want a sanity check on your next move?

If you’d like to run the ruler over your numbers — buying, refinancing, or planning ahead — we can keep it simple and practical.

Book a chat and let’s do a quick sanity check on your options.

You can check our other blogs: Here!