Easter celebrations Vs the conflict in the Middle East…

Life has certainly appeared more uncertain for many Australians — and the property and finance markets are feeling that uncertainty too.

The question is:

do you do nothing, or do you keep moving carefully?

The articles below are designed to help with that question. In some cases, the right move may be to wait. In others, it may be to act — but with better information, better timing and a clearer understanding of your options. Doing nothing can sometimes be the right short-term decision, but if left unchecked for too long, it can also become its own risk.

As one example, this month we have not included our usual Best Interest Rates analysis. A number of lenders are still updating their rates following the Reserve Bank of Australia (RBA) rate increase a few weeks ago. That means some of the lowest rates currently showing may simply reflect lenders who have not yet updated their pricing. Rather than publish something that may be misleading, we think it is better to hold off for a few weeks and then reassess once the market has settled and the data is more meaningful.

Topics in this edition:

- Interest rates: why the outlook feels less settled again

- Properties selling at a loss: where the pain is showing up — and where it isn’t

- First Home Buyers: family support is changing the playing field

- Building a new home: back on the radar, but not a free ride

- Deposit bonds; when they can help – and when to be careful

- Private lending and smarter broking: how technology is speeding up a once-manual process

- 5% deposit buying: more accessible but not automatic

- Buying a property with an existing tenant: what to check before you sign

Read more below.

Interest Rates:

Why the outlook feels less settled again?

Key message: The next rate move is no longer just about local inflation. Oil, freight and supply costs are back in the picture, which could keep pressure on prices even as parts of the economy soften.

If the rates conversation feels murkier again, you’re not imagining it.

The Reserve Bank lifted the cash rate in March, and while inflation has eased from its highs, it is still not fully back where the RBA wants it. On top of that, the global backdrop has become more complicated again.

The conflict involving Iran, the US and Israel has pushed energy markets higher, with the Strait of Hormuz back in focus. When that route is under pressure, oil and gas markets react quickly. That matters here because higher oil prices do not just affect petrol. Diesel, freight and transport costs can rise too, and those costs can flow into groceries, household goods and some building inputs.

The issue for borrowers is this.

If transport and input costs lift again, inflation can stay sticky for longer than expected. That does not automatically mean rates will rise again. But it does mean the path to lower rates may be bumpier than many borrowers were hoping a few months ago.

There is still a case for rate cuts later in 2026 if inflation keeps easing and the labour market softens further. But there is also a reason for caution: if higher fuel, shipping and supply costs linger, they can slow the return of inflation to target.

The practical takeaway is simple.

Do not make big finance decisions based only on what the media says the RBA “might” do next. What matters in real life is your actual lender rate, your repayment buffer, and the assessment settings in place when your application is reviewed.

Properties Selling At A Loss:

Where the pain is showing up — and where it isn't

Key message: Most Australian sellers are still making money, but losses are clustering in some Melbourne and Sydney unit markets. Queensland, Western Australia and South Australia, by contrast, remain much more profit-skewed.

If you read a headline about owners selling at a loss, it is easy to assume the market is broadly weakening.

That is not really the story.

The broader national picture is still one of strong resale profits. Cotality says 95.9% of Australian resales in the December quarter made a profit, the strongest result since 2005, with a median gain of $365,000. Loss-making sales were far more concentrated in units and in a smaller number of softer markets.

What is changing is where the pain is showing up.

In Victoria, some inner-city and unit-heavy markets are standing out for the wrong reasons. Reporting based on Cotality’s Pain & Gain data identified the City of Melbourne as the least profitable market nationally, with 45.9% of resales making a loss and a median loss of $64,500. Other Victorian examples included Stonnington at 25.5% loss-making resales with a median loss of $54,250, and Port Phillip at 25.4% with a median loss of $30,000. In New South Wales, Parramatta was also on the list, with 23.9% of resales making a loss and a median loss of $53,000.

That matters, because the national averages can hide a lot.

Why some properties are more exposed

One of the clearest dividing lines is houses versus units.

Cotality says 98.1% of house resales nationally were profitable, compared with 91.2% of unit resales. It also noted that loss-making sales were much more concentrated in parts of the Sydney and Melbourne unit markets. In plain English, weaker unit markets have been carrying much more of the pain.

The other major issue is hold period. Cotality says profit-making sales had a median hold period of 9.2 years, compared with 8.2 years for loss-making sales. In plain English, the less time owners have had for values to rise, the less margin there is for buying costs, selling costs, softer conditions or a weaker asset type.

Victoria and New South Wales are not telling the whole story

This is where Queensland, Western Australia and South Australia are useful as a contrast.

Domain’s March 2026 Profit and Loss Report shows that Brisbane remains far more profit-skewed than Melbourne and, in some respects, even stronger than Sydney on breadth of profitability. For houses, 99.5% of Brisbane resales made a profit, compared with 97.9% in Sydney and 95.9% in Melbourne. Brisbane units were also very strong, with 99.1% of resales making a profit. Sydney still had the highest median house profit at $750,000, but Brisbane’s median house profit was also substantial at $580,000, while Melbourne’s was lower at $390,000.

Western Australia and South Australia help reinforce the same point. Domain says Perth houses had a median resale profit of $528,000 and Perth units $226,050, while Adelaide houses had a median profit of $539,500 and Adelaide units $290,000. That is a reminder that loss-making sales are concentrated in specific markets and asset types, not spread evenly across the country.

Timing can change even when the long-term story has not

It is also worth keeping one eye on the broader backdrop.

Global events can change the timing of growth, even when they do not change the longer-term direction. Higher oil prices, inflation pressure and weaker confidence can temporarily slow buyer demand or make markets feel more fragile than they really are. That can spook the market in the short term, especially in weaker pockets, even if the underlying housing story for quality assets remains intact.

There are also signs that buyers have gained more negotiating power in softer markets. Recent reporting suggests a large share of Melbourne homes are now selling below asking price, which points to sellers having to adjust expectations and buyers having more room to negotiate. That does not automatically mean widespread losses — many owners are still selling at a profit — but it does reinforce the point that weaker markets can feel softer in real time, even when the longer-term profit story remains intact.

The Reserve Bank of Australia (RBA) has warned that a prolonged Middle East conflict could hit growth and unsettle inflation expectations, while recent reporting shows buyer confidence has softened and auction clearance rates have fallen as higher rates and uncertainty weigh on the market.

That does not automatically mean prices must fall sharply.

But it does mean timing can shift, sentiment can wobble, and some markets can pause or temporarily retrace before the longer-term trend reasserts itself. Growth may still prove to be the dominant long-term story for quality assets, but external shocks can change when that growth shows up. That is an important distinction.

The practical takeaway

If you own property, or you are thinking about buying an investment, the better question is not:

“Is the market up or down?”

It is:

- What type of property am I holding?

- How long am I likely to hold it?

- Is this market still supported by owner-occupier demand?

- If I had to sell sooner than planned, how exposed would I be?

- If broader confidence weakens for a period, do I have the buffer to ride that out?

That is the part that often gets missed.

Most owners are still selling at a profit. But the pain is real in some pockets, and it is showing up most clearly where shorter hold periods, weaker unit performance and softer market conditions overlap. At the same time, stronger markets such as Brisbane, Perth and Adelaide show that the national picture is still broader and more resilient than the headline “selling at a loss” story suggests.

If you want to pressure-test a property strategy, or review whether your current property still fits the job, shoot me an email and we can run through the numbers.

First Home Buyers:

Family support is changing the playing field

Key message: For some first home buyers, the real advantage is no longer just a bigger deposit — it is better strategy, better guidance and fewer mistakes.

For many first home buyers, the challenge is not just saving a deposit. It is competing well once they are in the market.

One interesting shift this year is how some families are helping. Instead of only gifting cash or going guarantor, some parents are now paying for buyer’s agents to help their children search, negotiate and avoid costly errors.

This can make sense in the current market.

When prices are high, supply is patchy and buyers are moving quickly, support is not always just about money. It can also be about confidence, decision-making and process. A good plan, a clear budget and the right advice early can stop a buyer overreaching or buying the wrong property in a rush.

This matters even more now because entry pathways have widened for some buyers. With the expanded 5% deposit government guarantee settings, more first home buyers may be able to enter sooner than before if they qualify.

But easier entry does not mean an easy market.

Cost-of-living pressure is still real. Fuel, freight and general household costs remain part of the picture, and lenders still assess whether a borrower can hold the loan comfortably. That is why preparation matters so much.

Not everyone needs a buyer’s agent. Plenty of first home buyers succeed by doing strong suburb research, attending enough inspections, understanding contract risk and getting pre-approval lined up early. But whether the support comes from family, an adviser or your own homework, the buyers doing best right now are usually the ones who prepare properly before they bid.

That is also where the BIR Finance Property Concierge service can help.

Our Property Concierge service is operated by Trish Moore of Hidden Gems Property Scouts. As a buyer’s agent, Trish can help buyers ask better questions, think more clearly about the right suburbs for their needs, and work through the issues that can easily be missed when you are moving quickly.

Next steps

- If you would like more information about Trish’s buyer’s advocate services, just ask and I can put you in touch.

- If you would like a copy of the BIR Finance Checklist: Plan your first home purchase, use the link below or shoot me an email.

Building A New Home:

Back on the radar, but not a free ride

Key message: Building is looking more attractive again for some buyers, but the smart play is to treat it as a project with timing, finance and cost risk — not just a cheaper alternative to buying established.

As established homes remain expensive in many areas, more buyers are taking another look at building.

That renewed interest is understandable. For some buyers, building can offer a more modern home, better energy efficiency and less direct competition than a tightly held established-home segment. In some areas, it can also be one of the few ways to get the kind of property you want without being dragged into repeated bidding contests.

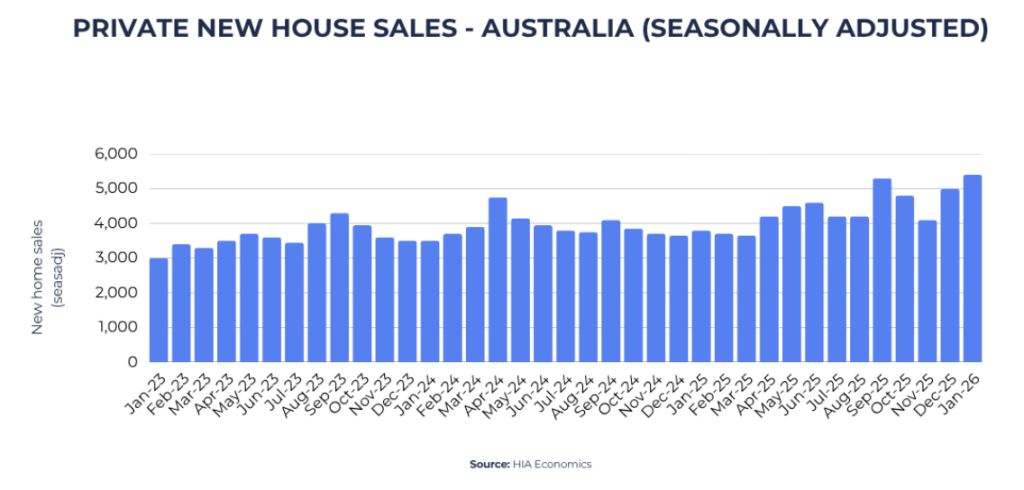

The latest HIA data shows detached new home sales remain well above a year ago, even though the month-to-month path is not smooth. HIA said sales fell 20.3% in February 2026 after a strong January, but still remained 27.3% higher than the same quarter a year earlier. That tells us demand has improved, but buyers and builders are still dealing with a stop-start environment rather than a straight-line recovery.

The chart below helps tell that story. It shows that new house sales have lifted from their softer period, but they are still moving in jumps rather than in a clean, steady climb. In plain English: interest has returned, but conditions are not yet easy or predictable.

The pros and cons of building

Building a home can offer real advantages:

- Modern layouts and better energy efficiency

- Less direct competition than many established-home markets

- The chance to customise the design, finishes and liveability features to suit your needs

But there are trade-offs too.

Land availability, project timing, finance structure and build costs all matter. HIA has also been warning that land remains a major constraint on home building in Australia, which affects affordability, project feasibility and how quickly supply can actually come on.

Then there is the broader macro backdrop. When oil and diesel prices rise, freight and transport costs can rise with them. That does not mean every building input suddenly jumps overnight, but it does mean builders, suppliers and buyers are operating in an environment where cost pressure can reappear quickly if disruption drags on. Reuters reports that higher energy prices are already affecting transport and industrial supply chains.

Buyers also need to plan for land purchases, construction contracts, progress payments and the possibility that timelines move. That matters because the build itself is only one part of the project. The finance structure, the contract detail and the cash buffer can matter just as much.

Financing a new build

A construction loan works differently from a standard home loan. Funds are usually released in stages as the build progresses, and lenders assess the project, builder, contract and valuation more carefully than many first-time builders expect.

That is why guidance matters. A build can look straightforward on paper, but the finance side often gets harder once you factor in timing, cash buffer, valuation risk, variations and the practical steps between land purchase and handover.

Prefabricated and modular homes: gaining ground, but finance is still catching up

Prefabricated and modular homes are also worth watching more closely.

They can offer faster delivery, better quality control and less site disruption, which is why they are becoming more accepted as a housing option. The finance side, however, is still catching up. One of the practical issues is that traditional stage-payment models were designed for on-site construction, not for rapid off-site builds where much of the value is created before the home reaches the site.

There are some passionate people working hard to make prefabrication part of the future of building. That matters because construction is still one of the few major industries where much of the core product is assembled in a highly site-based, almost artisan way.

Prefabrication offers a more efficient alternative, with the potential for faster delivery, less waste, stronger quality control and better use of sustainable materials and methods.

One of those advocates is Sameer Ramgoolam, founder of SMARTBuild Engineering. Through his involvement with Prefab Council Australia (PCA) in Victoria, he is helping push the case for homes that can be delivered faster, with less waste and stronger sustainability outcomes, without compromising quality. If you would like to know more about the Prefab Council or would like an introduction to Sameer, just let me know.

At this stage, Commonwealth Bank is the clearest publicly confirmed major-bank example in Australia. It has explicitly said it will fund eligible prefabricated homes during the off-site construction phase, subject to policy settings and manufacturer requirements.

Other lenders may still consider modular or prefab homes once the dwelling is fixed to the land, or via standard construction structures adapted case by case. But based on current public information, those positions appear to come more from builder and broker commentary than from clear lender policy pages. That caution can become even stronger where components are being manufactured offshore, because lenders may be less comfortable releasing funds against a finished product that is not yet on site in Australia.

If modular or prefab is on your radar, it is worth checking finance options early, before you commit.

Granny flats and small second homes: easier in more states, but still check the detail

Granny flats, small second homes and similar backyard dwellings are back in the conversation, and not just in Victoria. Several states have made them easier to build, rent out or approve, although the rules still vary a lot. New South Wales has a recognised pathway for secondary dwellings. Queensland removed family-only occupancy restrictions in 2022. Western Australia allows some ancillary dwellings without planning approval if they meet the deemed-to-comply rules, and South Australia has expanded the size and rental flexibility of ancillary accommodation. Victoria’s small second home reforms sit within that broader shift.

In Victoria, for example, a small second home of up to 60m² can often be built without a planning permit, but a building permit is still required and site-specific controls can still matter.

That is why these buildings are attracting more attention from homeowners and investors. They can create space for family, a home office, guest accommodation or future rental income, and they may offer a simpler path than a full-scale development.

But easier does not mean automatic.

The key nuance is that the rules are still highly state-based, and often site-based as well. Size limits, approval pathways, setbacks, services, title restrictions, overlays and building permit requirements can all differ. So while the broad trend is towards more flexibility, you still need to check your State’s rules and the actual constraints of the property before assuming the block will work for your plan.

I recently introduced Rhys Davies of RD Building Design and Sameer Ramgoolam of SMARTBuild Engineering after meeting them separately and thinking they should have a chat. Both are passionate about smarter building methods and where this part of the industry is heading. One of the themes that came through clearly was the push towards faster, more standardised and potentially more cost-effective building pathways. In that context, Rhys has also launched Boxed Buildings, which offers smaller additional buildings supplied as a complete kit “in a box”, ready to be constructed on site.

If granny flats, small second homes or boxed building solutions are on your radar, it is worth checking the rules, costs and finance options early — before you assume the approval path, the budget and the site will all line up the way you hope.

The practical takeaway

So yes, building can be a smart move.

But it works best when you go in with open eyes, realistic timeframes and enough flexibility in the numbers to deal with delays, cost changes and lender requirements. The opportunity is real. The homework is too.

Thinking about building, modular, or land plus construction?

Let’s run through the finance, timing and risks before you commit. Shoot me an email so we can have a chat.

Deposit Bonds:

When they can help — and when to be careful

Key message: A deposit bond can be a smart way to solve a deposit timing problem without tying up cash, but it is not a shortcut around settlement risk. The key is knowing when it genuinely helps, what it does not do, and how to use it to your advantage.

A deposit bond can be a useful tool when a buyer is ready to proceed, but the cash deposit is tied up, inconvenient to use, or better kept available for another purpose.

In simple terms, a deposit bond is a guarantee accepted by the vendor instead of paying the deposit in cash upfront. The buyer still needs to complete the purchase and pay the balance at settlement. That means a deposit bond is not a loan and it is not a substitute for having a proper funding plan. It is really a timing tool.

When a deposit bond may be worth considering

A deposit bond can make sense where the buyer is good for the deal, but the deposit cash is not ideally placed to be handed over at exchange.

That can include situations such as:

- Sale proceeds from another property are coming, but have not yet been received

- Cash is sitting in an offset account and the buyer would rather keep it working for them

- An off-the-plan purchase has a long period between exchange and completion

- SMSF rollover funds have not yet reached the new fund bank account

- A buyer in retirement wants to avoid unnecessary short-term debt or more complexity than needed

In one retirement-phase scenario, the key issue was not long-term borrowing capacity but how to move forward with confidence while sale proceeds and settlement timing were still in play. That is exactly the kind of situation where a deposit bond may be worth exploring.

How a deposit bond can work to a buyer’s advantage

The biggest advantage is flexibility.

If a buyer can keep cash in an offset account, term deposit or other controlled environment rather than handing over a deposit months or years before settlement, that can be financially useful. Deposit Power’s commentary points out that in some off-the-plan scenarios, the cost of the bond may compare favourably to the interest savings achieved by leaving the deposit funds in offset. The cost of a deposit bond is usually a one-off fee based on the deposit amount and the length of the bond, rather than ongoing interest like a loan. Where agreed in advance, a deposit bond can also be used to cover the deposit at auction, so the buyer does not need to immediately hand over a large amount of cash.

There is also a risk-management angle.

Handing over a cash deposit means relying on other parties and processes before settlement. Tash Hibberd’s comments raised practical risks buyers should at least be aware of, including cyber fraud, trust-account issues, and disputes over release or refund of deposit money. A deposit bond does not remove contract risk, but it can reduce the amount of cash sitting exposed before settlement.

For off-the-plan purchases, deposit bonds may also help where the buyer wants to preserve liquidity over a long project period. If the development does not proceed, the buyer may at least have avoided having a large sum tied up in cash for years while waiting for an outcome.

The limits buyers need to understand

A deposit bond is not a magic solution.

It does not reduce the purchase price. It does not reduce stamp duty. It does not solve a weak borrowing position. And it does not remove the obligation to settle.

If the buyer cannot complete, the bond provider may pay the vendor and then recover that amount from the buyer under its own agreement. In other words, the bond helps with timing, but it does not make the underlying obligation disappear.

Other things to keep in mind include:

- There is an upfront fee

- The vendor must accept the bond

- The bond must match the contract requirements

- Expiry dates and settlement timing matter

- If a straightforward cash deposit is available and causes no issues, a bond may not be the best tool

That is why a deposit bond should be seen as a specialist solution for a specific problem, not the default answer in every purchase.

A common obstacle: agent resistance

One of the more practical issues that came through strongly is that some agents do not like deposit bonds.

In Victoria especially, this can be linked to long‑standing practice where deposits are paid in cash into a trust account and may later be released early under Section 27 of the Sale of Land Act, which is also the mechanism through which many agents are accustomed to having their commission paid from the deposit. Tash Hibberd’s comments suggest two practical ways to deal with this.

One is to structure the deposit with a smaller cash component and the balance by bond. The other is for the purchaser’s conveyancer to deal directly with the vendor’s conveyancer, because acceptance of a deposit bond is really a contract issue between the parties rather than simply an agent preference.

That is an important point for buyers.

If a deposit bond is otherwise suitable, the discussion should focus on whether:

- The vendor will accept it

- The contract allows for it

- The conveyancers are comfortable with the wording and mechanics

- There is a commercial middle ground if some cash is still needed

The goal is not to “beat” the agent. It is to structure the deal in a way that still works for the parties.

Where this can be especially useful

Deposit bonds can be particularly useful where the buyer is asset-backed but cash-timing constrained.

That may include:

- Retirees buying before sale proceeds are available

- SMSF trustees waiting on rollover funds

- Upgraders who have equity but want to avoid bridging unless needed

- Off-the-plan buyers who would rather preserve liquidity until settlement

In SMSF scenarios, there may be structures where members or related entities arrange a deposit bond outside the fund while rollover funds are pending. However, SMSF borrowing and security rules are complex, and any use of deposit bonds must be carefully structured so the fund does not provide inappropriate security over its assets, breach the borrowing or in‑house asset rules, or inadvertently create contribution or early‑release issues. In practice, this is a specialist area and should always be checked with the relevant SMSF, legal and tax advisers before proceeding.

The practical takeaway

A deposit bond can be a very good solution when the problem is timing, not capacity.

It can help a buyer preserve cash, avoid tying money up too early, reduce some forms of deposit risk, and create flexibility in scenarios where a conventional cash deposit is awkward or inefficient.

But it only works well if:

- The buyer still has a strong settlement plan

- The contract timing and bond expiry line up properly

- The vendor accepts it

- The conveyancers are on top of the wording and mechanics

- Everyone is clear that the bond solves a timing issue, not a funding shortfall

That is where good structuring matters.

For some buyers, a cash deposit will still be the simplest option. For others, bridging finance may still be the better answer. But in the right scenario, a deposit bond can be the cleaner and more efficient way through.

If you are wondering whether a deposit bond could help in your situation, shoot me an email and we can work through whether it is the right tool — and how to structure it properly

Private Lending And Smart Broking:

How technology is speeding up a once manual process

Key message: Private lending has often been slower, less transparent and more manual than it should be. New broker technology is helping change that — and that means BIR Finance can assess suitable private lending options faster and more efficiently where the scenario calls for it.

Private lending has traditionally been one of the more manual corners of the lending market.

That was not always because the deals were especially complex. Often, it was because the process itself was clunky. A broker might need to contact multiple lenders one by one, explain the same scenario repeatedly, wait for indicative terms to come back, and then try to compare very different pricing structures, fees and appetites.

That is where technology is starting to make a real difference.

I recently caught up with the co-founders of ThinkPrivate, Matthew and Joshua Cottam. ThinkPrivate offers a broker-only platform designed to help mortgage brokers compare private lenders more quickly, request indicative terms and access private credit options in a more structured way. For brokers, that means less time spent chasing blind alleys and more time focused on the lenders and structures that may actually suit the client’s scenario.

For BIR Finance, that matters because private lending is something we already do.

The value here is not that a platform suddenly creates a new service line for us. The value is that it can help us deliver that service more efficiently. In the right scenario, that means faster comparison, quicker filtering of lender appetite, and a more organised starting point for working through private lending options.

Why this matters for clients

For clients, the biggest benefit is usually not the technology itself. It is what the technology can improve.

In private lending, speed can matter. So can clarity. A client may need a short-term solution for a property matter, a time-sensitive commercial transaction, a refinance that mainstream lenders will not handle quickly enough, or a funding gap that needs a more flexible credit approach.

A better broker platform can help make that first stage more efficient. Instead of treating private lending like a mystery market that only a few insiders can navigate, tools like this can help brokers compare lenders side by side and move to indicative terms more quickly.

That does not mean private lending becomes simple or automatic.

Private lending still needs judgement. It still needs careful scenario analysis, security assessment, exit planning and a clear explanation of the costs and risks. But better tools can reduce friction in the process, and that is a real benefit.

A sign that broking is finally catching up

This also points to a broader issue in broking.

Parts of the industry have been slower than they should have been to adopt technology in areas where manual work has hung around for too long. Private lending is a good example. For years, too much of the process depended on broker memory, lender relationships, spreadsheets, email chains and “who do I know who might look at this?” thinking.

There is still real value in experience and relationships.

But the smarter model is to combine that experience with technology that improves speed, comparison and consistency. That is where platforms like ThinkPrivate are useful. They do not replace broker judgement — they support it.

Another reason this matters

This matters even more because private credit is becoming a bigger and more visible part of the finance landscape.

As that market grows, brokers need better ways to navigate it. Better technology can help brokers move faster, compare more cleanly and create a more transparent process for clients.

It also fits our broader approach at BIR Finance: using technology where it genuinely improves speed, transparency and client choice.

The practical takeaway

Private lending is not for every client, and it should never be treated as a casual substitute for mainstream finance.

But where it is appropriate, broker technology is making the process sharper. It can help brokers compare options faster, identify likely lender fit earlier and move clients through the first stage of the process with more structure and less wasted motion.

For BIR Finance, that is the real point.

It is another example of how we use technology to improve the way we research, compare and deliver lending options for clients — especially in areas where the industry has historically been too manual, too slow and too opaque.

If you have a scenario that may need a private lending solution, shoot me an email and we can talk through whether it is worth exploring.

Key message: Buying with a 5% deposit is more achievable than it used to be, but the smaller deposit is only one part of the puzzle — you still need a strong application and a plan that can handle real-life costs.

One of the biggest shifts for first home buyers over the past year has been easier access to low-deposit entry.

The Australian Government 5% Deposit Scheme, administered by Housing Australia, now has unlimited places, no income caps, and higher property price caps from 1 October 2025. Eligible first home buyers may be able to purchase with as little as a 5% deposit without paying lenders mortgage insurance, while eligible single parents and legal guardians may be able to buy with as little as 2% deposit.

That is a meaningful change, because it can bring home ownership forward for buyers who are otherwise ready but have not yet reached a 20% deposit.

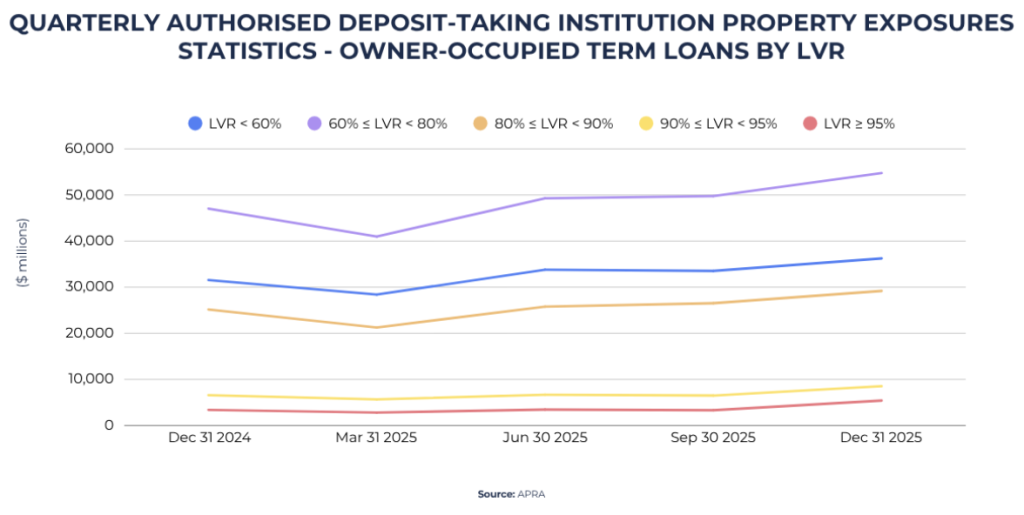

APRA’s latest quarterly ADI statistics also show that higher-LVR lending remains a meaningful part of the market. The share of new loans funded with an LVR of 80% or more rose to 32.2% in December 2025, up from 31.0% a year earlier. That does not mean all of those loans were scheme loans, but it does show that lower-deposit borrowing remains active.

The chart helps put that into context. It shows that low-deposit buying is not a fringe idea — it is a real and growing part of the market. But it also points to a second truth: easier entry does not mean easier credit.

How the scheme works

Normally, buyers who purchase with less than a 20% deposit may need to pay Lenders Mortgage Insurance (LMI). LMI can be expensive and a very real cost, even if capitalised and added to your loan balance.

Illustrative example only: At 95% lending, the upfront premium is about $14,872 on a $500,000 purchase and about $35,931 on a $900,000 purchase. And if you capitalise the premium, as many cash-strapped buyers do, the extra interest cost over a 30-year loan at 6.00% p.a. is close to $17,227 on a $500,000 purchase or $41,622 on a $900,000 purchase. Add that to the premium itself, and LMI becomes a very weighty cost over the life of the loan.

Under the government scheme, Housing Australia provides a guarantee to the participating lender, which can allow eligible buyers to purchase with a smaller deposit without paying LMI.

For many first home buyers, that can mean entering the market years earlier than expected.

That is the upside.

What buyers still need to remember

A smaller deposit does not remove the need for a strong application.

Lenders still assess income, living expenses, repayment capacity and the overall strength of the file. That matters even more in a market where rates are still relatively high, inflation has not fully settled, and cost-of-living pressure remains part of everyday life.

That is the part some buyers miss.

A smaller deposit can help you get in sooner. But it does not remove the need for a sensible budget, genuine cash discipline and a realistic price range. If petrol, groceries, insurance and general household costs keep rising, that can change how comfortable a loan feels after settlement, even if the approval looked fine on paper.

APRA’s data also shows that higher debt-to-income lending has lifted, which is one reason regulators are keeping a close eye on riskier parts of the market. In plain English: lower-deposit entry may be easier than before, but lenders and regulators still care a lot about whether the loan is sustainable.

The practical takeaway

So the real question is not just:

“Can I get approved?”

It is also:

- Can I complete comfortably?

- Can I hold the loan if costs rise?

- Am I buying at a level that still gives me breathing room?

The good news is that low-deposit buying is more accessible than before. The caution is that entering sooner only works well when the application is strong and the plan is sustainable.

That is the difference between getting in sooner and getting in well.

Want to know whether a 5% deposit pathway could work for you?

Let’s check your borrowing power, scheme fit and funds to complete before you commit.

Key message: If you buy a tenanted property, you usually inherit the lease and many of the landlord responsibilities that come with it. The key is to make sure the tenancy fits your plans before you commit.

I spoke with Dawn Barry, Founder of Skilled Conveyancing, about one of the issues buyers can easily overlook: purchasing a property with an existing tenant in place. While the comments below are framed by Victorian property law and State-based tenancy rules, the broader lesson applies anywhere — if you are buying a tenanted property, proper due diligence matters.

The first question is simple, but important: does the tenancy suit your plans?

If you are buying as an investor and are happy to keep the tenant, that may be fine. But if you want to move in, renovate quickly, or re-let at a different rent, the existing tenancy can materially affect timing, flexibility and cashflow.

That is because when you buy a tenanted property, you usually step into the vendor’s shoes as the new rental provider. The lease generally continues on its current terms, and you take on the legal responsibilities that come with it. In Victoria, rental providers cannot simply end a tenancy without a valid reason, even at the end of a fixed term. Consumer Affairs Victoria says the ban on no-fault evictions took effect on 25 November 2025, and notices to vacate now require a valid reason and the correct notice period.

Fixed term or periodic lease: it matters

One of the first things to check is whether the tenant is on a fixed-term lease or a periodic (month-to-month) arrangement.

If it is fixed term, the renter will usually have the right to stay until the end date unless the tenancy ends in accordance with the law. If it has rolled to a periodic tenancy, that may give you more flexibility, but not a free hand. In Victoria, a notice to vacate still needs a valid legal reason, and in many cases the notice period is 90 days.

Do not just read the contract — read the tenancy too

Before you sign, make sure the lease and related tenancy documents are included with the contract so they can be reviewed properly and you can understand the implications.

At a minimum, you should check the following:

- The signed lease or residential rental agreement

- The rent amount and frequency

- Whether the rent is in arrears

- The bond amount and Residential Tenancies Bond Authority (RTBA) details

- The lease end date

- Any special conditions, such as pets, repairs or inclusions

- The condition report

- Any notices served

- Any repair history, unresolved maintenance or active disputes

- Any tribunal applications, dispute resolution processes or unresolved issues already on foot

That last point matters more than many buyers realise. Consumer Affairs Victoria says Rental Dispute Resolution Victoria can now deal with disputes about issues including repairs, rent increases and bonds before or instead of VCAT in some cases. If there is already a dispute on foot, you want to know before settlement, not after.

Check whether the rent actually suits the property

A tenanted property does not always mean the rent is at market level.

The rent may be below market, or there may be limits on when and how it can be increased. In Victoria, the minimum notice period for rent increases is now 90 days. That means even if the rent looks light, you may not be able to change it quickly.

It is also worth checking what type of tenancy is in place. If the renter is on a fixed-term lease, the rent and other lease terms will usually continue until that term ends unless changed in accordance with the law. If the tenancy is periodic, there may be more flexibility to increase the rent after settlement, but only if the correct legal process and notice periods are followed.

So part of your due diligence should be checking:

- Whether the current rent is in line with local market evidence

- When the rent was last increased

- Whether the lease timing suits your plans

- Whether the property still stacks up if the tenant stays longer than you hoped

Bond transfer and records matter too

Make sure the bond records are handled properly.

In Victoria, RTBA transactions are managed online, and rental providers must use the RTBA system to manage bond transactions. Consumer Affairs Victoria says rental providers must have a registered RTBA account to transact, and bond or agreement transfers need to be updated through the RTBA process.

In practical terms, that means you want confirmation that the bond amount, renter details and rental-provider details are all correct and capable of being updated properly after settlement.

The practical takeaway

If you are buying a property with an existing tenant, do not treat the tenancy as a side issue.

It can affect possession, renovation timing, rent, cashflow and your legal obligations from day one. That is why it is worth having both the contract and the tenancy documents reviewed before you sign.

We have also prepared a checklist on this topic.

If you would like a copy of the BIR Finance Checklist: Buying a property with an existing tenant (Victoria), just shoot me an email and I’ll send it through.