The other day, I realised that December was almost upon us – and we all know what that means – Santa will want to get paid!

This guide brings together home loan advice on rates, buying and selling options, low-doc pathways, credit health, car finance, and a few life tools to start 2026 on the front foot.

It’s been an interesting year in so many ways. And 2026 will, I suspect, be more of a roller coaster ride.

This guide brings together home loan advice on rates, buying and selling options, low-doc pathways, credit health, car finance, and a few life tools to start 2026 on the front foot.

So let’s keep your brain cells active with another bumper edition of our newsletter.

- Take the pledge – and join me for the summer 5 drive

- Best interest rates

- Block sizes continue to shrink – but interior space holds up

- The vendor’s ultimate checklist – selling your home in 2026

- Just for buyers – our free Property Concierge service

- Buying before you sell – your funding options explained

- 77.6% of Australians choose brokers – while branches continue to close

- Lo doc loans – clearer and faster – and easier on your accountant

- Your credit file can be lender-critical – obtain our special report

- Christmas credit – how it can crimp your borrowing power

- How to choose the right car loan for your budget

- 7 skills to build resilience & mental toughness

- 12 keys to a successful career move – a practical guide for executives

Read more below.

Take the pledge and join me for the Ruby Slipper Club “Summer 5 Drive”

This campaign turns small, steady gifts into real, local protection for women and girls. The goal is bold—100,000 Ruby Slipper Club members by 28 February 2026—to fund safe spaces, legal help and practical support, fast.

What is the Ruby Slipper Club?

The Ruby Slipper Club is Women of Oz’s regular-giving program. Your recurring donation fuels their blueprint—building The Emerald Lady safe haven, expanding Housing Spaces, strengthening a legal fund, and scaling Wheels 2 Freedom (cars to women fleeing family and domestic violence).

What’s the “Summer 5 Drive”?

It’s a simple, shareable push running through summer: join, then recruit your circle of five so the movement grows exponentially. The ask is purposely doable – small weekly or monthly amounts, multiplied by community action – to reach that 100,000-member target by 28 February 2026.

Connection creates protection so no woman walks alone.

Where your steady gift goes

- Immediate safety & support: funding a purpose-built sanctuary (The Emerald Lady) and crisis responses that shorten the distance from danger to safety.

- Legal backing when it counts: a ProtectHer-style legal fund to stand with women navigating orders, custody, housing and finance issues.

- Practical mobility: Wheels 2 Freedom—road-ready cars for women rebuilding independence (work, school runs, appointments).

- Community & continuity: a predictable monthly income enables Women of Oz to scale programs and respond more quickly when the phone rings.

Why this drive is different

- Movement > one-off donations: regular gifts build the capacity to prevent harm, not just respond to it.

- A clear, measurable target: 100,000 members by a fixed date (end of summer) gives everyone a scoreboard to rally around.

- Peer-powered growth: that “five friends” model makes it easy to talk about and easy to action—today.

How to help – three quick options

- Join the Ruby Slipper Club as a recurring donor (any sustainable amount helps). Click here

- Invite five trusted friends or colleagues to join you (your “Summer 5”).

Best Interest Rates

RBA on hold; lenders not moving in lockstep

Where we are now

- Cash rate unchanged at 3.60%. The RBA kept settings steady to guide inflation (around 3.2%) back toward 2–3% while aiming for a soft landing.

- Financial conditions still restrictive—but easing at the edges. As Assistant Governor Christopher Kent noted, mortgage payments are drifting lower and housing credit is ticking up from earlier rate cuts.

Themes to watch in this month’s pricing

- Uneven competition. Some lenders are quietly trimming select rates while others are holding or lifting fixed terms. It’s a jostling market, not a uniform one—worth a check if your rate hasn’t budged.

- Short-term (1 and 2 years) fixed is back on the radar. With variables steady, 1–2 year fixed slices can help smooth cash flow over the summer period without locking you in for too long.

- Investor vs owner-occupier drift. We’re seeing selective moves by repayment type (P&I vs IO) and purpose (OO vs investor). Structure choice matters as much as the headline rate.

- Clean-energy discounts matter. Where eligible, “green” pricing continues to shave a little off the variable—useful if you’re upgrading appliances/solar anyway.

- Borrowing power is sensitive to unsecured debt. Christmas spending season is here—limits and statement balances can shrink capacity even when the RBA is on hold.

What to do now

- Sense-check your rate. If you haven’t seen movement, let’s benchmark your loan against the best of today’s competitive set.

- Consider a short fixed anchor. For budgeting certainty into 2026, weigh a 1–2 year fixed alongside variable and split options.

- Tidy cards before summer. Trim unused limits and pay down balances. It protects borrowing power for January/February applications.

- Buying soon? Do suburb-level homework. Prices are still bubbling overall, but some higher-end pockets have pulled back—local evidence beats headlines.

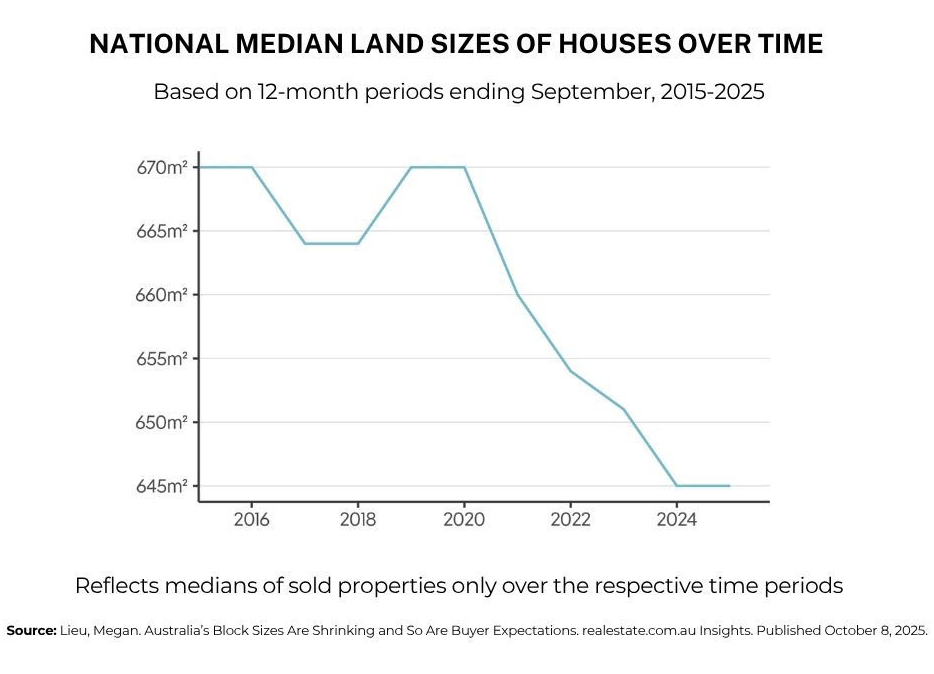

Block sizes continue to shrink but interior space holds up

Australian homes are being built on smaller blocks than a decade ago—but interior space has generally held up due to smarter floorplans and more two-storey designs.

What’s changed:

PropTrack analysis indicates the median land area of sold houses has trended down from about 670sqm (2015) to ~645sqm (2025) as population growth, land scarcity and planning rules push more infill and medium-density supply.

Megan Lieu, REA Group’s Economic Analyst, noted, “At a national level, the average floor area of a newly built house is currently 241sqm.” Megan Lieu, REA Group / PropTrack. She went on to say, “Over the past decade, the interior area of a house has consistently ranged between 230sqm and 240sqm.”

According to Ms Lieu, one key driver is population growth, which has increased by 15% since 2015. With limited land supply and planning restrictions, “land and ultimately housing costs tend to rise”, she said. To keep prices within reach, new homes are being built on smaller blocks, often through zoning reforms that promote infill development and more townhouses and duplexes.

What this means for buyers:

- Expect less yard but similar internal area and better locations/amenities.

- Designs focus on function (storage, light/aspect, multi-use rooms) instead of sheer land size.

- Being finance-ready helps you act quickly on good infill listings.

Practical tips for 2026:

- Prioritise aspect, storage and room function over backyard size.

- Compare whole-of-ownership costs (rates, utilities, maintenance, body corporate), not just list price.

- If building, check planning overlays and timelines before you commit.

Looking at townhouses or infill sites?

Book a 15-min Purchase plan—we’ll set price guardrails and structure your loan to save interest. You choose from side-by-side lender options. (What we see, you see—rates, fees, features.)

The vendor's ultimate checklist for selling your home in 2026

Based on “The Ultimate Checklist for Selling Your Home in 2025” by Kathryn Fantov, Sydney Vendor Advocates.

Selling in 2026? Use this step-by-step guide to prep with confidence—so you present well, market smart, and negotiate a strong result.

1) Research your local market

Understanding your local market is the foundation of a successful sale. Track comparable sales, attend open homes and a couple of auctions, and estimate your value from evidence—not just appraisals. Set alerts on REA/Domain, keep a simple spreadsheet (superior/ inferior/comparable), and note quoted ranges vs final prices. This keeps expectations realistic and strengthens your negotiation stance.

2) Take an objective look at your home

See your home through a buyer’s eyes. Neutralise strong colours, declutter room-by-room, and fix small maintenance issues (peeling paint, leaking taps, mould). Tip: ask a trusted friend – or a professional – to give frank feedback on your presentation. A neutral, well-kept space helps buyers picture themselves living there.

3) Prepare your home for sale

Preparation maximises appeal and sale price. Line up trades early, prioritise high-impact fixes, and consider professional styling or furniture hire if your current look is bulky or dated. If you are in Melbourne, have a chat with Susan and Rayleen from 3Two Projects. Small updates (fresh flowers, modern fixtures, tidy garden) can lift first impressions and encourage higher offers.

4) Engage a property lawyer or conveyancer

Secure legal support before listing. Decide between a solicitor (best for complex matters) or a licensed conveyancer (often fine for straightforward deals), gather quotes, and get your Contract of Sale prepared in advance so marketing isn’t delayed.

If you need a good conveyancer, let me know and I will give you a short list for conveyancers who do a great job in your State.

5) Choose the right sales agent—or use a Vendor Advocate

The agent you pick can make or break your result. Interview at least three: ask about experience, strategy, and fees—and avoid pressure tactics. A Vendor Advocate can shortlist and manage agents for you and is typically paid by sharing the agent’s commission, simplifying the choice while keeping incentives aligned.

6) Prepare for photos and marketing

First impressions happen online. Co-create a marketing plan with your agent/advocate, schedule professional photography, and make the home “inspection ready” (spotless, decluttered, styled). Decide if video is necessary for your property—some homes benefit, others don’t. Focus on hero areas: exterior, living, kitchen, bathrooms, and one or two bedrooms.

If you are Melbourne-based, arrange a call with Brendan Rossmen from Pitch Digital – he is a photographer who knows far more than just photography, videography and drones. His pitch is perfect!

7) Host a standout first open home

Set the tone on day one. Create ambience (fresh flowers, light scent, soft music), maximise natural light (curtains open, lights on), and step out early to let buyers explore comfortably. Small touches—cushions, white sheers—can make spaces feel bigger and brighter.

8) Handle offers like a pro

Choose the right sale method (auction vs private treaty) for your market. If multiple buyers emerge, structured tactics like best & final or silent auction can maximise competition. For auctions, set a realistic but aspirational reserve with your advocate—and be open to exceptional pre-auction offers if they meet your goals.

9) Settle—and celebrate

A great sale is a milestone—take a moment to celebrate it. Then switch into move-out logistics.

10) Your next property

Don’t leave finance to the last minute. Line up your finance and timing early to avoid gaps.

Just for buyers: Our FREE property concierge service

As many of you are aware, BIR Finance offers you a free property concierge service. Trish Moore from Hidden Gems Property Scouts, a buyer’s advocate, is available to assist you with all your questions about buying a property.

While Trish focuses her attention on Melbourne and the western corridor, she has access to all the data across the nation, making her a convenient one-stop shop for all those initial queries you might have.

You can use her knowledge and research to get a much better feel for what is going on in the market you are looking to buy into.

Some of the things Trish can assist you with:

- Which suburbs fit your brief and budget

- What to look for at inspections (and what to avoid)

- Pricing, auctions, and negotiation tips

- Sense-check current property values and price drivers

- Decide hold vs. renovate vs. sell (and ROI on upgrades)

- Get rent appraisal pointers or tenant-ready tips

- Plan timing if you might buy, sell or restructure next year

Would you like to have a chat with Trish now? Just reply and I will organise this for you.

Buying before you sell: Your funding options explained

Buying and selling homes can be tricky and complex – and with some hidden costs.

Do you play it safe and sell first, then move to temporary accommodation and then move again to your next dream home? Or do you risk it and sell and buy at the same time and organise bridging finance in case you buy before you sell?

These days at least, you have options.

You have the traditional bridging loan offered by the banks and then you have a couple of other choices – with pros and cons.

Let’s take a quick deep dive!

Option 1 – the traditional bridging loan

- A traditional bridging loan is a short-term, interest-only loan that helps you “bridge” the financial gap between buying a new home and selling your existing one.

- Typically lasting up to 12 months, it combines your existing mortgage with the loan needed to purchase your new property, calculated as “peak debt”—the total amount owed on both properties, including purchase costs.

- During the bridging period, you usually make interest-only monthly repayments based on this peak debt, easing cash flow while you sell your old home.

- Once your current property sells, the sale proceeds pay down the bridging loan, leaving you with a standard home loan on your new property at a more competitive interest rate.

- While bridging loans carry higher interest rates than regular home loans, they provide flexibility to secure your next property without the stress of selling first or moving twice. However, you need to demonstrate your ability to service both loans during the bridging term, and be aware of additional costs such as valuation fees and discharge fees.

Option 2 – niche funder like Bridgit

- Bridgit offers a modern, flexible alternative to traditional bridging finance, designed to make your property transition easier and less stressful. With Bridgit, you can buy your next home before you sell your existing one, and benefit from no monthly repayments or early exit fees during the bridging period, which can last up to 12 months.

- They have a quick, simple online application process that provides approval in as little as 24 hours, allowing you to move swiftly on your dream home without waiting.

- Bridgit assesses loans primarily based on your property equity rather than income verification, making it accessible to a wider range of homeowners, including those who are self-employed or retired.

- This approach also means you avoid the pressure of servicing two loans monthly, as interest capitalises and repayment is made in full once your current property sells.

- Like a bridging loan, Bridgit empowers you to buy confidently and sell later, saving on temporary accommodation and double-moving costs while unlocking your property’s equity on your terms.

- Its total cost can be a bit higher than a normal bridging loan, but it makes up for this cost with a very fast approval process.

Option 3 – Deposit Bond

- Deposit bonds offer a distinct approach by eliminating the need for a cash deposit when purchasing a property, making them a more cost-effective alternative to bridging finance.

- Instead of borrowing money, a deposit bond acts as a guarantee from an insurer to the property vendor that the deposit will be paid on your behalf at settlement, typically covering up to 10% of the purchase price. This means you don’t need to liquidate your savings or assets upfront, allowing your money to remain invested and earn interest.

- Deposit bonds are especially useful for buyers who are selling one property and buying another, but might face timing gaps in accessing funds.

- Although they do not cover the entire purchase price and must be settled in full at contract completion, deposit bonds can ease upfront financial pressure and provide flexibility when negotiating property sales.

- However, if the purchase falls through, the insurer will pay the vendor and then seek reimbursement from you; therefore, it’s essential to understand the terms and risks involved. They are often accepted for new builds, auctions, or off-the-plan purchases, where deposits may be required later in the process.

Option 4 – Equity-release facilities like Midkey

- Midkey offers a no-monthly-payment loan secured against your home equity rather than relying heavily on income or cash flow.

- This product is designed primarily for asset-rich but cash-poor homeowners who want flexible access to funds without monthly interest repayments, making it very different from traditional bridging loans. Instead of monthly payments, interest accrues and a deferral fee is payable at the end based on property value growth.

- Midkey loans can be used as either a first or second mortgage and provide borrowing limits up to around 30-35% of your home’s value, enabling you to access significant funds for renovations, property purchases, or other life needs without the usual servicing pressure. So, while it shares features with equity release products, Midkey’s bridging loans blend bridging finance flexibility with equity release principles, allowing borrowers to control timing and repayments more freely

Each bridging finance option serves different borrower needs and scenarios, making it important to select the right solution based on timing, financial capacity, and risk tolerance.

Traditional Bridging Loan – Best For:

- Buyers who want the certainty of finance to cover the full purchase price before selling.

- Those comfortable with paying monthly interest on peak debt.

- Homeowners with strong income verification and servicing capacity.

- Situations where bridging is needed for up to 12 months.

- Those willing to manage potential double repayments during the bridging period.

Bridgit Bridging Loan – Best For:

- Buyers requiring more flexible, no-monthly-repayment bridging for up to 12-24 months.

- Self-employed, retirees, or borrowers with irregular income who can demonstrate sufficient equity.

- Those who prefer fast online approval and a simple application process.

- Situations where avoiding monthly cash flow pressure and early exit fees is a priority.

- Borrowers seeking a tech-driven, customer-focused service.

Midkey Bridging/Equity Release Loan – Best For:

- Asset-rich, cash-poor homeowners needing access to equity without monthly repayments.

- Those wanting extended, flexible bridging terms beyond traditional loan periods.

- Borrowers who want to defer repayments and minimise immediate cash flow impact.

- Using the product not just for property transitions but also renovations, lifestyle needs, or debt consolidation.

- Not typical for short bridging but excellent for longer-term equity release blended with bridging purposes.

Deposit Bond – Best For:

- Buyers who need to secure a property quickly without immediate access to a cash deposit.

- Particularly suitable for new builds, auctions, off-the-plan purchases, or where deposit timing is uncertain.

- Buyers who maintain cash liquidity while satisfying contract deposit requirements.

- The ‘what next’ following a deposit bond involves arranging bridging finance or term loans to cover the actual deposit payment at settlement, as the deposit bond only guarantees the deposit to the vendor, which is paid out when the contract settles. This settling bridging finance is usually short-term (e.g., 1-3 months) to complete the purchase after sale or refinancing.

Combining a Deposit Bond with a Bridgit or Traditional Finance loan

- You can use a deposit bond initially to secure the property purchase without cash upfront.

- Then, arrange a bridging loan to finance the deposit payment when due and facilitate completion. Bridgit’s no-monthly-repayment model and flexible terms make it ideal for this follow-on finance, especially if you still need to sell your existing property.

This combination allows you to manage liquidity through purchase certainty and flexible settlement financing while avoiding cash outflow stress early in the process.

If you have a scenario you would like to discuss, let us run the numbers for you so you can make an informed decision.

77.6% of Australians choose brokers while branches continue to close

Broker growth

The share of new home loans written by brokers has climbed to record levels as borrowers seek choice, explanations and convenience—with the added legal protection of Best Interests Duty (BID).

Broker market share reached 77.6% of new residential lending in the June 2025 quarter, per data compiled by Cotality for the Mortgage & Finance Association of Australia (MFAA), reflecting an increase of over 11% from the level in 2020 (66%).

But that’s not the whole story. Since around 2010:

- The market share of brokers has more than doubled – from 33% to over 77%. The Big 4 banks have therefore seen their ‘direct to customer’ business fall substantially – both because of the growth in the broker market share and because brokers use more than just the Big 4 (more on that below).

- Broker numbers have also roughly doubled to over 22,000.

- Of this number, approximately 20% of brokers were inactive (i.e. they did not write a loan over a 6-month period).

A quick story on broker choice and why it matters

At a recent AI-in-broking conference, I asked a fellow broker which tools he uses to find the best loans for clients. His answer surprised me: “If it fits one big-bank calculator, I’m done.” That’s not how everyone works—but it’s a reminder to choose your broker carefully.

Tip when you’re interviewing a broker: ask about the range of lenders they actually use and whether any single lender dominates their loan book. As a rule of thumb, if more than 3 out of 10 recent deals went to one lender, it’s worth asking why—there may be factors other than total cost shaping the recommendation.

We prefer our three pillars approach incorporating choice, transparency, and fit—so you can decide with clear side-by-side options.

Retail bank shrinkage

At the same time, Australia’s bank branch network has continued to shrink:

- 2010: there were around 7,000 branches

- 2015: an 8% shrinkage to ~6,500 branches

- 2025: a fall to 3,205 by June 2025 – less than half from 2010, with 155 branches closed in the 2024–25 year (a 5% annual fall and 33% down over five years), reinforcing the shift to broker-assisted, digital-first journeys.

Why are more borrowers turning to brokers?

- More choice. Brokers can access dozens of lenders, not just one, giving borrowers a wider range of loan products and interest rates.

- Personalised service. Brokers take the time to understand each borrower’s goals and financial situation so that loan structures, features and policies can be matched to your goals.

- Expert guidance and policy know-how. They help navigate complex lending criteria and compare options that can be hard to decipher alone, and they can identify lender niches you won’t see on a simple rate card.

- With choice, personalised service, and expert guidance comes a better fit.

- Convenience. With many banks reducing face-to-face services, brokers provide flexible, human support online or in person. And with digital meetings, secure document flows, quick comparisons, you can get on top of your options with transparency and speed.

- Best Interests Duty. Brokers are legally required to act in their customers’ best interests – banks are not held by the same duty.

Contact me if you’d like to explore your home loan options or compare rates across multiple lenders. We’ll quickly show you how much you can borrow and who is likely to lend to you.

Lo doc loans—clearer, faster: And easier on your accountant

If you’re self-employed and your tax return doesn’t quite tell the full story, a low-doc (alt-doc) loan can still get you home sooner—without putting your accountant in a bind.

Most low-doc options ask your accountant to sign a letter. The catch? Some letters demand specific income figures (e.g., net profit, taxable income). That can clash with what’s in your files or create extra work.

We’ve reviewed the common accountant letters across banks, non-banks and private lenders and built a simple traffic-light view so you know what you’re walking into. We have also assessed these accountant letters from the perspective of the accounting professional bodies, which are putting more caution on what an accountant can sign.

Our Accountant Letter assessment

1 – Flexible (best for accountants):

The letter doesn’t require income disclosure. The accountant confirms awareness of the loan/repayments and general capacity—no numbers needed.

2 – Moderate:

The letter is close to flexible but includes lender reliance wording or a light declaration that still keeps accountants comfortable in many cases.

3 – Strict:

The letter requires specific income figures (e.g., NPBT/taxable income) and extra confirmations.

What we do with our assessment:

- Shortlist lenders quickly for your scenario

- Show pathways that are kinder to your accountant

- Avoid surprises late in the process.

When a low-doc path makes sense

- You’re self-employed, and the latest tax return understates your current performance

- You can show BAS or business bank statements but not completed tax returns

- You want to minimise your accountant’s burden and keep the letter simple

- You need a clear plan if approval is “not yet” (e.g., ABN/GST age, tidy ATO plan, adjust LVR).

Our promise

- Transparent lending: you’ll see the same matrix we see.

- Financial empowerment: we explain the trade-offs (rate vs documentation vs speed).

- Wealth creation focus: we help you pick a structure that works now and in 12–24 months when you may shift to full-doc.

If you think you might need a low-doc loan, reach out and let’s see which lender is likely to fit you – and your accountant – best. We’ll run your scenario, show you the traffic-light view, and outline the simplest document path. We will also assist you with any discussions with your accountant so you can navigate this safely and quickly.

Your credit file can be lender-critical: Obtain our special report

Your credit file is often overlooked in the lending process – until it is actually reviewed. And then everyone zeros in on what is contained within – what’s right, what’s wrong and what has been omitted.

We recently took a deep dive into the mysterious black box of your credit file, and we uncovered some amazing (and disturbing) information that every person, borrower or not, should be aware of.

You owe it to yourself to check out the blog link

and see what we found

But first, some quick tips and insights:

- There are three reporting agencies. You should obtain a copy of all three (and in this age of cybercrime, this should be done regularly).

- A cluster of credit enquiries can hurt you, especially across multiple products.

- Adverse listings can be a deal breaker for major lenders, forcing you to turn to alternative lenders as the only lending solution.

- Ensure your ID and address details are up to date and accurate.

Christmas Credit: How it can crimp your borrowing power

As a segue from your credit file, let’s examine one key component: your credit card.

You can safely say Australians are hooked on their credit cards. And Christmas time comes with a big credit card dopamine hit with gifts, travel and social events on the agenda. But if you’re planning to buy a property or refinance early next year, it’s worth keeping an eye on how much you spend.

With an interest-free period of up to 60 days, credit cards can be a valuable tool for managing cash flow and debt levels. However, not handled wisely, they can be one of the biggest traps for those who can least afford it, with very high interest rates once you miss that monthly payment deadline. Additionally, missing a payment can have a negative impact on your credit score.

Some credit card statistics:

- Aussies process over 308 million credit card transactions a month (27 transactions per card), with annual growth of around 6%.

- Our credit card debt exceeds $43.2 billion, with 41% ($17.9 billion) accruing interest at a rate of approximately 18.7%. Those accruing interest will also have a reduced credit report score, so it is a double whammy, and it can potentially limit your lender selection.

- The average credit card balance is $3,557, with an average limit of $10,487.

- Card activity typically peaks in November and December. Lenders assess your balances and your total credit limits—even on rarely used cards—which can reduce borrowing capacity in January/February applications.

Tips when applying for your next loan:

- If serviceability for your next loan might be an issue, consider reducing unused limits to increase your calculated borrowing power.

- Avoid stacking BNPL alongside high credit card limits, as it can cloud affordability.

- Keep your payments up to date. If you can’t pay your credit card bill on time, what does that say to a lender who is looking to advance to you hundreds of thousands of dollars?

Before you apply or refi, let’s check your limits and balances. We’ll model the impact and save interest where we can, so you can choose the lender after you see the numbers.

Picking the right car loan: Keep it simple and transparent

Many buyers turn to dealer finance for convenience, but brokers can often access better-value loans from a broader range of lenders and tailor repayments to your situation.

The cheapest rate isn’t always the lowest total cost. Structure matters—secured vs unsecured, term length, fees, and whether you use a balloon.

Key points to weigh:

- Secured vs unsecured: secured is usually cheaper (car as collateral).

- Term length: longer = lower monthly, higher total interest.

- Fees: application + ongoing fees change true cost (check the comparison rate).

- Balloon: lowers instalments, raises total cost and leaves a lump sum at the end.

- Early payout terms: check for fees if you’ll upgrade sooner.

Segments

- First-home buyers: don’t let car debt reduce home-loan capacity – shorter term, no balloon.

- Homeowners (P&I): match term to how long you’ll keep the car.

- Investors/business owners: check tax treatment and usage evidence; compare chattel mortgage vs consumer loan where applicable.

- Under pressure: prioritise reliability and total cost, not the sticker price alone.

7 Skills to build resilience and mental toughness

Based upon the work of John Cooksey, Confident Performance, here are some excellent tips for building resilience.

What is resilience?

It is your ability to bounce back from setbacks. Mental toughness is what helps you use that bounce—moving forward with confidence, focus and purpose. Together, they help you handle pressure, recover faster and keep pursuing what matters most. Here’s a practical guide you can use at work, at home, and in sport.

1) Understand resilience (and drop the myths)

Struggle is part of life. Resilience doesn’t mean you never feel bad; it means you feel it, learn from it, and keep going.

Common myths to ditch:

- “Resilient people don’t feel sad or stressed.” They do— they just recover differently.

- “You must grind non-stop.” Rest and self-care are part of sustainable resilience.

- “You’re born resilient or you’re not.” Resilience is a learnable skill set.

- “If you’re resilient, problems disappear.” Life still throws curveballs—you get better at handling them.

Quick start: Write one example where you’ve bounced back before. What helped? Keep that strategy in your toolkit.

2) Develop emotion regulation

You can’t control every event, but you can influence your response. Emotion regulation is noticing what you feel, naming it, and choosing a helpful next step.

Core practices:

- Re-frame the situation (cognitive reappraisal): look for other explanations instead of assuming the worst.

- Allow negative emotions: label them (e.g., “I’m feeling anxious”), accept they’re valid, give them space to pass.

- Increase positive emotions on purpose: schedule enjoyable activities, practise gratitude, and balance negative self-talk.

- Mindfulness micro-drills (2–10 minutes): Breathe and notice: set a 3-minute timer; when the mind wanders, gently return to your breath.

- Grounding walk: name five things you see, four you hear, three you feel.

- “Leaves on a stream” visualisation: imagine each thought resting on a leaf and floating past.

3) Take responsibility (with curiosity and compassion)

Responsibility isn’t self-blame; it’s reclaiming choice. Get curious about your role and what you can improve next time.

Try:

- Three questions: “What’s my part here?”, “What’s one behaviour I’ll try differently?”, “Who can help?”

- Apology checklist: say sorry; name the specific action; ask what you missed; agree on a next step.

- Forgiveness practice (repeat): identify the emotion; name the hurt; say “I forgive you”; notice the release; invite a positive focus.

- Helpful rituals: a morning routine, scheduled check-ins, reminders to pause before reacting, and a daily “what did I learn?” note.

4) Build community

Resilience grows in connection. A supportive network gives perspective, accountability and encouragement.

- Audit your circle: who energises you, who drains you, and where are the gaps?

- Strengthen ties: invite friends to shared activities; be present, listen, and put the phone down.

- Join groups: classes, clubs, community sport—consistent contact builds belonging.

- Stay accountable: tell one person your weekly goal; ask them to check in with you (and offer the same back).

5) Strengthen your relationship with yourself

- Self-compassion is not indulgence—it’s fuel for change. Treat yourself like someone worth helping.

- Start with basics: hygiene, sleep, nutritious food, and a tidy space. Small wins create momentum (yes, even making the bed).

- Watch your self-talk: write common critical phrases and rewrite them as balanced, supportive statements.

- Micro-acts of care: a kind note to yourself, an hour outside, device-free time, a solo meal you actually enjoy.

- Try this: end each day with one sentence—“Today I’m proud I ___.”

6) Exercise for brain and body

Movement is a natural mood stabiliser. It builds confidence, reduces stress and supports clearer thinking.

- Benefits: counters low mood and anxiety; releases tension; improves sleep; boosts self-worth through progress.

- Keep it enjoyable.

- Get started: begin small (10 minutes), stack it onto an existing habit, go with a friend, and track progress weekly.

- Remember: consistency beats intensity. Aim for “most days, some movement.”

7) Challenge yourself (values-led goals)

- Growth needs stretch. Set goals that align with your values so the effort feels meaningful.

- Name your values: write your top 3–5 (e.g., family, learning, health, service, creativity).

- Set one 90-day goal + three weekly mini-goals: make them specific, realistic and time-bound.

- Create accountability: tell someone you trust; schedule checkpoints; celebrate small wins.

- When stuck between options, ask: “Which choice best reflects my values?” Then take the smallest next step.

12 Keys to a successful career move: A practical guide for executives

Based on the original “12 Keys to a Great Career Move” by Russell Johnson & Associates, refreshed with practical steps you can use today.

I have known Russell for many years, and I like what he has put together. I have often said similar things to people looking to find a well-paying job, but Russell has put it all together in a nice, neat package.

If you’re considering a move—by choice or circumstance—this guide shows how to take control of your next step. It blends time-tested principles with current research on referrals, ATS screening, interviewing and salary negotiation.

Job-seeking vs Strategic Career Management

Job-seeking is reactive (chasing ads, hoping to fit). Strategic Career Management is proactive: you clarify what you want, position your value, and build relationships so opportunities come to you.

1) Think of yourself as a business

- I absolutely love this one and have used it many times.

- Treat employers as customers and yourself as a solutions partner.

- Lead with their problem, not your job title.

- Frame your pitch as outcomes you deliver (revenue, savings, risk reduction, capability).

Action: Create a one-page “offer sheet” with your top 3 outcomes, 3–5 proof points, and 2 brief case studies.

2) Know what you really want — and act accordingly

- Define the work, culture and impact you want.

- Money matters, but sustained performance comes from meaning and fit.

Action: Write a short “target brief” (industries, problems you solve, role scope, culture/values, location/hybrid).

3) Rebuild self-belief through action

- Confidence follows behaviour. Schedule weekly actions that create momentum – learning, outreach, portfolio work.

Action: Three micro-wins each week: one learning, one outreach, one asset improved (portfolio/profile).

4) Become compelling — to yourself first

- Draft your 60-second value story and rehearse it until it’s crisp and natural. Visualise success and practice.

5) Use a marketing strategy (not just applications)

- Applications are late-stage tactics. First, get known for the problems you solve in the circles that hire for them (events, communities, thoughtful outreach).

Action: Aim for 10–15 warm conversations/month with decision-makers or close adjacents.

6) Sharpen your Value Proposition

- Spell out the specific, transferable outcomes you deliver and map them to each target employer’s priorities.

7) Work with how hiring really happens (relationships reduce risk)

- Referrals shorten time-to-hire and are heavily used by employers; they reduce perceived risk and improve fit.

- Focus on authentic connections and asking for advice, not favours.

Action: Ask for 20-minute informational interviews—short, respectful conversations that surface needs and build advocates.

8) Build collateral that passes human and ATS checks

- Many large organisations screen with Applicant Tracking Systems (ATS). Use clear formatting and mirror relevant job-description language naturally so both humans and software see your fit.

Action:

- LinkedIn: headline = problem you solve; About = outcomes + proof; recent roles = quantified achievements.

- CV: two pages; outcome-led bullets; keywords woven naturally (no keyword stuffing).

9) Prepare for interviews (structure beats improvisation)

- Practice behavioural answers (Situation-Task-Action-Result) and role-specific challenges.

- Bring a one-page “first 90 days” outline to signal readiness.

- Structured approaches predict performance better than unstructured chats—prepare accordingly.

10) Prepare for negotiation (plan variables, not just salary)

- Negotiation typically leads to better total packages—pay, benefits, or both.

- Script your ask and rehearse it.

Default line: “I’m excited about the role and team. Based on scope and market, I’m targeting a total package in the $X–$Y range. How close can we get?”

11) Design a “hidden market” approach (ethical networking)

- Many senior roles emerge through relationships. Informational conversations uncover needs, reduce risk, and position you as a solution—without asking for a job.

Action: Shortlist 30–40 target organisations; schedule 6–8 quality conversations/month.

12) Execute with discipline

- Block weekly time for research, outreach, applications, and rehearsal.

- Track your pipeline (lead → conversation → interview → offer) and refine based on results.