Using BIR Finance, Santa has arranged financing for his elves’ holiday wages and transportation costs while he waits to be paid for his deliveries. Based on prior years, he will probably get paid in February by those worldwide residents who believe in Santa and have not maxed out their credit cards.

Meanwhile, the Christmas break might be close, but the property and lending world hasn’t clocked off – yet.

As we approach the silly season, it is fair to say that first-home buyers are the big recipients of the Government’s largesse this Christmas. However, for those FHBs who overextend themselves, 2026 may be a tough year. We have covered this below when we look at the various government schemes and how they can work for FHBs.

And as we wind down for Christmas, remember that lenders and real estate agents also like to take holidays, and many of them will be doing the Slip, Slop, Slap and heading off to destinations near and far. So any loans and property sales not completed before the Christmas week will be subject to skeleton staff until the second week of January or thereabouts.

In this edition:

- It’s Christmas time – a time to spread the love and joy

- Best interest rates

- Investor lending climbs to record highs

- First-home buyers – the 5% deposit pathway just got way bigger

- Government shared equity Vs 5% deposit scheme – who wins?

- Property prices – back to record highs

- Car finance – ASIC uncovers real problems

- Australia’s immigration wave and property prices – what’s really going on?

- “I’m an AI junky” – find out what AI thinks about AI

- Holiday tips from the experts – fun, sun and home sweet home

Ready to read on? And of course, if anything raises a question about your own plans, just hit reply and we’ll talk it through.

It's Christmas time a time to spread the love and joy and support one another!

Women of Oz

Uniting the community to drive monumental social change that ensures the safety, respect, and well-being of women and girls.

Let this be the summer that changes it all.

100 Days. 100,000 People. One Formula That Ensures No Woman Walks Alone.

Destiny Rescue

Rescuing children from sexual exploitation and human trafficking.

Join the mission to rescue 690 more lives this Christmas.

Orange Sky

Positively connecting communities and supporting people experiencing homelessness and hardship through access to free laundry, warm showers and genuine conversation.

Help support the 122,000 homeless.

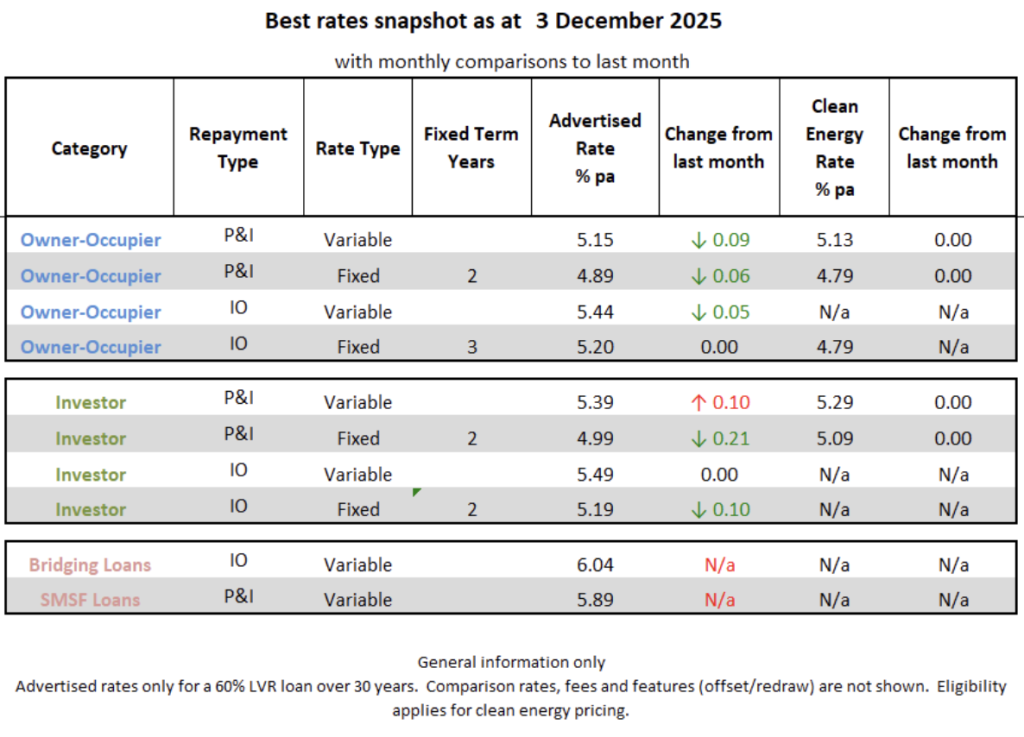

Best Interest Rates

Themes to watch in this month’s pricing

This month’s pattern – modest easing for most home-owner and several investor fixed rates, a small rise in the sharpest investor variable rate, and steady premiums on specialist loans – is consistent with a market where competition is intense but bounded by APRA settings and serviceability tests. Strong, lower-DTI borrowers are being courted; highly leveraged or complex borrowers are still paying a clear premium.

Specifics

- Owner-occupier best rates have edged down again this month, with principal and interest variable down about 0.09% and two-year fixed down 0.06%. That fits with lenders competing hard for lower-risk home-owner business while prices are still rising nationally.

- Investor pricing is more mixed: the sharpest move is a 0.10% rise in the best investor principal and interest variable rate, while the sharper cuts are actually in fixed rates (around 0.21% lower for two-year P&I and 0.10% lower for two-year interest-only). This suggests lenders are nudging up the cost of day-to-day investor borrowing while still using sharper fixed offers to win selected deals.

- The gap between the headline owner-occupier and investor variable P&I rates is now only around a quarter of a percent (about 5.15% vs 5.39%), at a time when investor loans make up roughly 40% of all new housing loans and are growing much faster than owner-occupier loans.

- APRA’s new cap on high debt-to-income (DTI) loans, which takes effect from February 2026, limits loans with a DTI of six or more to 20% of new lending for both owner-occupiers and investors. While APRA expects little short-term impact (only about 6% of loans are currently above that level), lenders are likely to preserve room under that cap for their strongest, most profitable borrowers – especially investors, who tend to borrow at higher DTI ratios.

- Clean-energy rates have not moved this month, even though the equivalent standard owner-occupier rates have fallen. That means the gap between the “green” and standard offers has narrowed slightly, but the clean-energy options are still in the market as a way for eligible borrowers to shave a little off their rate while upgrading to more efficient homes.

- Specialist products such as Bridging and SMSF loans remain priced well above the sharpest owner-occupier and investor rates (around the high-5s to low-6s), and there is no sign of these niches following the small cuts in mainstream pricing. That lines up with lenders staying cautious on more complex or capital-intensive lending while affordability is still stretched.

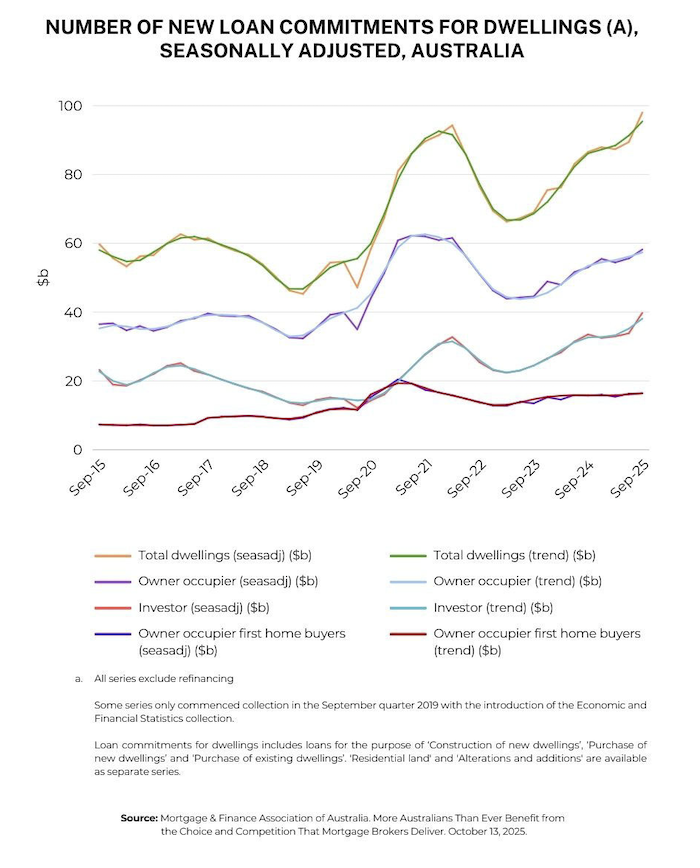

Investor Lending: Climbs to record highs

Investor activity hasn’t just picked up – it’s now at record levels around two in every five new home loans

According to the Australian Bureau of Statistics, 57,624 new investment loans were approved in the September quarter 2025, up 13.6% on the previous quarter, with the value of new investor loans rising 17.6% to $39.8 billion.

That’s a strong signal that many investors are positioning for the next phase of the cycle.

What’s driving the renewed interest?

Rental markets are tight: vacancy rates remain low in many areas, giving investors confidence they can keep properties tenanted.

Rents are rising faster than inflation: rental income has grown strongly in recent years, helping underpin yields even with higher borrowing costs.

Prices are climbing again: with values rising across most capitals, many investors prefer to buy into a rising market rather than chase it later.

Population growth is fuelling demand: strong migration and household formation are adding to the number of people needing somewhere to live.

Tax settings remain supportive: for eligible investors, interest, maintenance and depreciation can often be deducted – improving after-tax returns when the structure is set up properly (but please check with your tax adviser before proceeding).

How this could apply to you

If you’re eyeing an investment property, it’s worth:

- Checking your borrowing power under today’s policies.

- Comparing loan structures (interest-only vs principal and interest, offset accounts, splits).

- Modelling your cash flow with buffers for higher costs or vacancies.

I can run side-by-side scenarios

and show you, on screen,

how different options affect your cash flow and risk

before you commit.

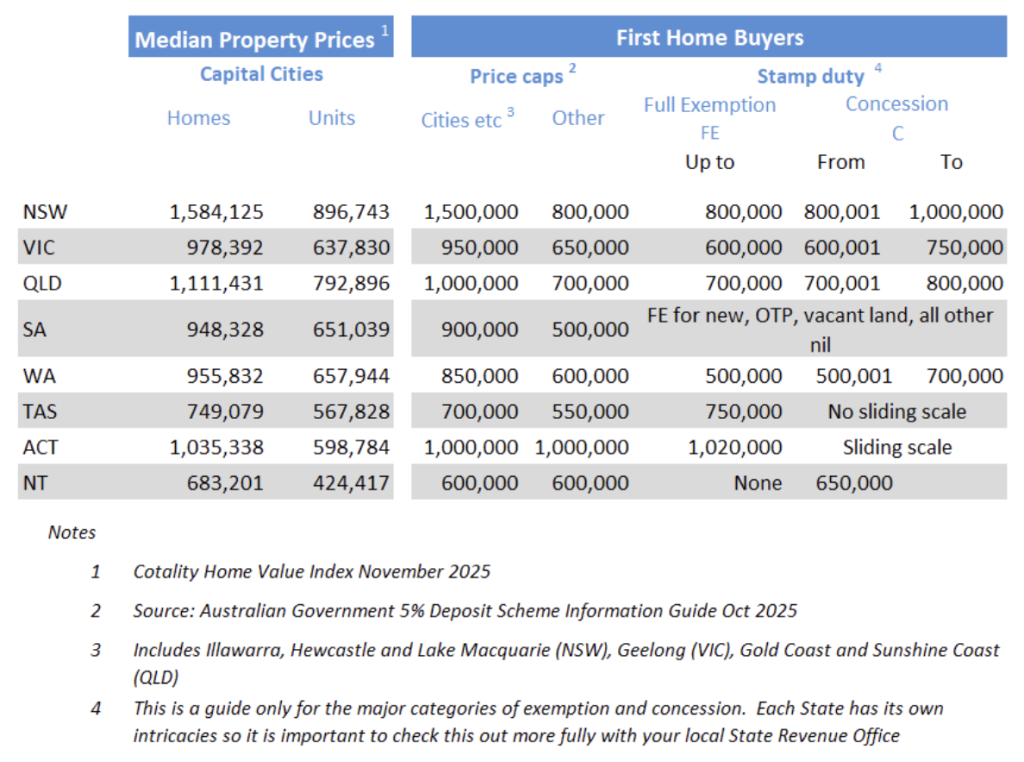

First Homebuyers: The 5% Deposit Pathway Just Got Bigger

From 1 October 2025, the federal government has significantly expanded the 5% Deposit Scheme (previously the Home Guarantee Scheme).

The changes are designed to bring more first-home buyers into the market sooner, by tackling the deposit and LMI hurdles.

Key changes

Unlimited places: there’s no longer a hard cap on the number of guarantees issued each year.

No income caps: all first-home buyers can potentially qualify, subject to standard credit and serviceability checks.

Higher property price caps: thresholds have been lifted across cities and regions to reflect higher property values.

Still just a 5% deposit – with no LMI: the government effectively guarantees up to 15% of the property value, so eligible buyers can avoid lenders’ mortgage insurance with only 5% down.

What this means in practice

For many first-home buyers, the biggest barrier hasn’t been the repayment – it’s saving a full 20% deposit plus stamp duty and costs.

With the expanded scheme, you may be able to:

- Buy with a 5% deposit instead of 20%.

- Avoid an LMI premium that can run into tens of thousands of dollars.

- Access a wider range of properties that now sit under the higher caps.

But there are still some important checks:

- You must meet the lender’s normal credit criteria.

- A high loan-to-value ratio means you should keep a sensible buffer in your budget.

- Not all lenders offer the scheme, and products, policies and rates differ.

- You also need to allow for stamp duty where the property falls outside of the exemption and concessional stamp duty rates (and this can be quite hefty).

I can help you work through whether the scheme fits your situation,

what a comfortable price range looks like,

and how repayments might move if rates change again.

Government Shared Equity VS. 5% Deposit Scheme: Who wins?

Having covered in depth the revised and broader 5% deposit scheme, let’s have a sneaky look at the other new scheme, which is just about to swamp the property market headlines. The Fed’s shared equity scheme.

We now have:

- A federal shared equity scheme (Help to Buy).

- An uncapped 5% Deposit Scheme.

- State-based shared equity schemes in parts of Australia.

And they are all sitting atop a market where prices are at or near record highs, and borrowing rules are still tight.

The 5% Deposit Scheme - a quick summary (details above ☝️)

The expanded 5% Deposit Scheme (government guarantee):

- Lets eligible first-home buyers purchase with a 5% deposit.

- Removes the need for Lenders Mortgage Insurance (LMI).

- Leaves you with a standard home loan for up to 95% of the property price.

- A reasonably wide pool of lenders, but in practical terms, nowhere nearly as wide as a broker’s panel (40 to 60 + lenders)

You:

- Keep 100% of the equity and future growth.

- Carry a larger mortgage, higher repayments and more exposure to rate rises.

- Are still tested on the full loan amount under normal serviceability rules

It’s a strong fit when deposit, not income, is your main hurdle.

How shared equity works (Federal Help to Buy)

The new federal Help to Buy scheme is a national shared equity program:

- You contribute at least a 2% deposit.

- The Commonwealth contributes up to 40% of the price for a new home, or 30% for an existing home, as an equity partner.

- You then borrow the remaining 58–68% as a home loan.

You live in the home and pay no rent on the government’s share, but:

- The government owns that share alongside you, and

- You share gains (and losses) in proportion when you sell or buy them out over time.

Key settings (at launch):

- 10,000 places per year for four years

- Income caps – generally up to $100,000 for singles and $160,000 for couples/single parents

- Price caps based on where you’re buying (up to about $1.3m in Sydney).

- Available via CBA (no broker involvement) or Bank Australia (direct to bank or via the broker channel).

Compared with the 5% Deposit Scheme:

- Your loan is smaller, repayments are lower, and your serviceability looks better.

- But you trade away a slice of future growth and need a plan to buy that share back later.

- Brokers can only assist you if you borrow from Bank Australia. The other lender, Commonwealth Bank, which has been set up to handle the Help to Buy scheme, has not offered this to its broker channel. (This restriction also applies to some of the various State-based schemes).

5% deposit vs shared equity: which problem are you trying to solve?

The decision is less about which scheme is “better” and more about what’s holding you back.

If your main barrier is the deposit, the 5% Deposit Scheme tends to suit buyers who:

- Have solid, stable income.

- Could service a 95% loan at today’s assessment rates.

- Want to keep 100% of the capital growth.

You’re using the guarantee to clear the deposit/LMI hurdle, not to reduce the loan size.

If your main barrier is borrowing power and cash flow, shared equity (federal or State) can make sense where:

- Serviceability is tight under standard tests.

- You need the loan amount itself to come down so the numbers work.

- You want lower monthly repayments and more breathing room, even if that means sharing future upside.

Shared equity directly reduces your debt. For some households – especially in higher-priced cities – it may be the only way to get a suitable home without overstretching.

Keeping it honest: these schemes are not “free money”

From a wealth-creation and financial-empowerment point of view, a few truths need to be front and centre:

- Shared equity is not free money – it’s an equity partnership designed to help with upfront affordability in exchange for a share of future value.

- The 5% Deposit Scheme still leaves you highly geared; it solves deposit and LMI, not long-term repayment risk.

- In some cases, the best option is still to wait, build a bigger deposit, or adjust the property brief, rather than forcing a purchase into a structure that doesn’t fit.

My role isn’t to push a particular scheme. It’s to broaden your options, show the trade-offs in numbers, and help you choose the path that aligns with your risk tolerance and long-term plans.

So, who “wins” – shared equity or 5% deposit?

Both shared equity and the 5% deposit guarantee can be powerful tools where:

- Prices and rents are high.

- Investor activity is strong.

- Borrowing rules are still tight.

If your key problem is saving a deposit, the 5% Deposit Scheme often wins.

If your key problem is borrowing power and cash flow, shared equity (federal or State) may be the safer way to get a suitable home without over-stretching.

If you’re not quite comfortable with either, waiting and building a buffer may be the smartest move.

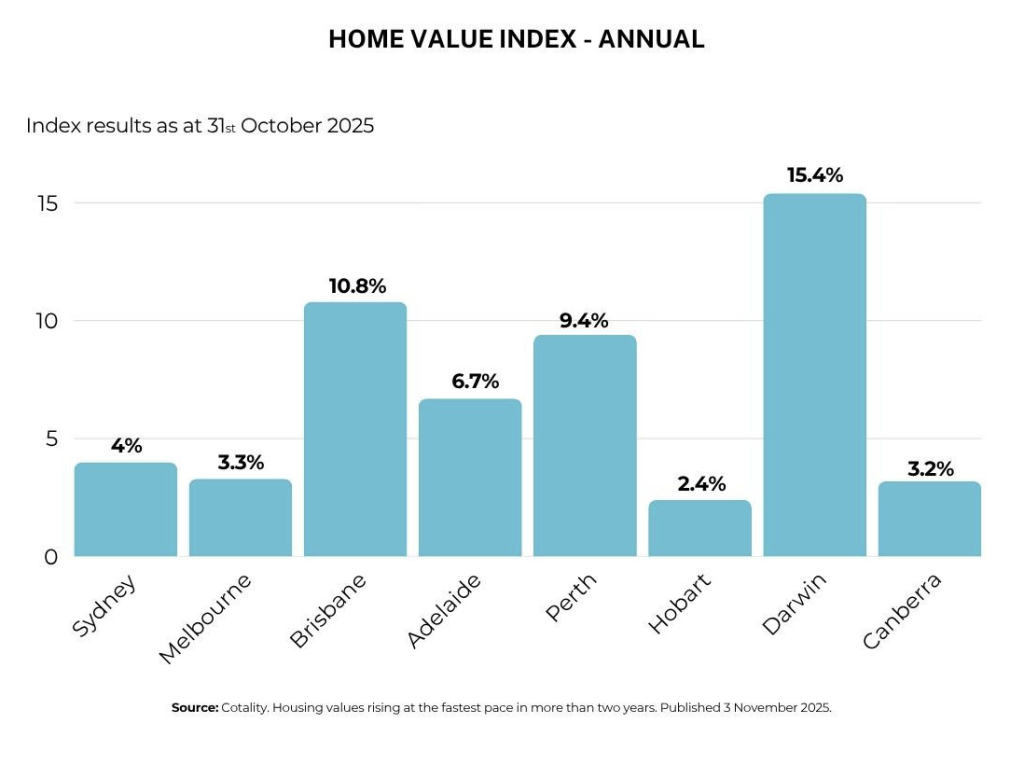

Property Prices: Back At Record Highs

Home values haven’t just bounced – they’re back at all-time highs, with momentum still strongest outside Sydney and Melbourne.

Cotality (formerly CoreLogic) reports national home prices rose 1% in November, after a 1.1% rise in October, taking the median dwelling value to about $889,000 and leaving prices roughly 7.5% higher over 2025 so far.

Darwin has surged, with Brisbane and Perth continuing to grow rapidly, while Sydney and Melbourne are rising more modestly. Melbourne is the outlier in the sense that it’s median property price is at comparatively historical lows.

What’s pushing prices higher?

Very low listings

In several cities – especially Perth and Brisbane – the number of homes for sale is well below average, which concentrates competition per property.

Weak new supply

Building approvals and completions have been lagging, so new stock isn’t keeping up with population growth.

Demand helped by rate cuts and schemes

The RBA’s rate cuts through 2025, and the expanded 5% Deposit Scheme, have helped some buyers back into the market and brought more first-home buyers forward.

At the same time, housing affordability is at or near a record high, with dwelling values sitting at close to eight times average household income in some indexes. That means borrowing power is constrained, and careful budgeting really matters.

How to buy well in this market

In a low-stock, rising-price environment, the buyers who tend to do best:

- Know their maximum safe budget before they start bidding

- Set clear price guardrails for each property and stick to them

- Have their pre-approval and loan structure sorted early, so finance isn’t holding them back

- Use a quality buyer advocate. We have a few you can choose from and they have a network of interstate colleagues for areas they do not specialise in.

- Have a chat with Trish Moore, who heads up our Property Concierge service – free, practical and professional advice for our clients.

And if you would like a practical view of “what you can safely spend”, with different lender options and structures laid out side-by-side, I can walk you through it on a Zoom screen share.

Car Finance: ASIC Undercovers Dealer Finance Problems

Car finance often gets treated as an afterthought – something you sign at the dealership so you can drive away quickly.

ASIC’s current review of Australia’s motor vehicle finance sector suggests that’s risky, especially for regional and First Nations borrowers.

In November 2025, ASIC reported:

- Cracks in lenders’ oversight of car finance distributors

- Problematic sales tactics at the point of sale

- Poor monitoring and auditing of dealers and introducers

Consumer advocates have also highlighted high rates of early default, and cases where some consumers still owed more than half the original amount after their car was repossessed – leaving them with a debt but no vehicle.

What’s the real risk?

The biggest risk isn’t car finance itself; it’s signing up when:

- You haven’t seen the true total cost of the loan over its full term.

- You haven’t compared the dealer’s offer with independent options.

- The repayments push your budget too far once you factor in your home loan, other debts and future plans.

That’s where getting advice first can make a big difference. Our experts can:

- Compare a range of car-loan options, not just the one offered at the dealership.

- Explain fees and structures (like balloon payments and different terms) in plain English.

- Check how a new car loan fits into your overall borrowing capacity and goals.

Want to avoid costly car loan mistakes?

Australia's Immigration Wave and Property Prices: What's Really Going On?

You’ve probably seen the headlines about a “migration surge” pushing up property prices and rents.

At the same time, we’re seeing record investor lending and house prices at or near all-time highs in many cities.

But the story is more nuanced than “more people = higher prices”. It’s about who is coming, why they came in such large numbers after COVID, and how policy is already turning the tide.

Here’s a plain-English look at what’s happening – and what it could mean if you’re thinking of buying, investing or holding off.

The headline numbers – and why the surge is already easing

The best way to measure migration’s impact on housing is Net Overseas Migration (NOM) – arrivals minus departures over 12 months.

From the ABS data:

- NOM peaked at around 536,000 people in 2022–23.

- It eased to about 446,000 in 2023–24, as rules tightened and more people left.

- By March 2025, annual NOM had dropped further to roughly 316,000, about 36% lower than a year earlier.

So yes, we had a genuine surge – especially in 2022–23 – but it’s already past its peak and is now moving back towards more normal levels.

Why it matters: NOM is the number that feeds directly into population growth, housing demand and infrastructure planning. Airport arrival tallies can look scary, but they often double-count short trips and tourists.

Who’s actually coming?

The migration mix matters just as much as the total.

1. Students and recent graduates

The largest group during the surge was international students – about 207,000 people in 2023–24.

Many stayed on afterwards via Temporary Graduate visas to work and gain local experience.

Recent reforms have tightened English requirements, lifted financial tests, and introduced a planning level for student places, so future flows should be more steady and more “genuine-study” focused.

2. Skilled workers

The permanent Migration Program is heavily skills-focused – roughly 70%+ of places go to the Skill stream.

Temporary skilled visas fill specific gaps in health, construction, energy and technology.

These groups are smaller than students by headcount, but important for hospitals, infrastructure, renewables and digital roles.

3. Working Holiday Makers and other temporary cohorts

Provide flexible labour in hospitality, agriculture and services.

Numbers move with the economy and policy, but they’re not the main driver of population growth over the medium term.

Why did migration surge after borders reopened?

Three big drivers:

COVID catch-up

When borders reopened, there was a backlog of people who’d been waiting to come – especially students. A few years’ worth of demand landed in a short window.

Education as a major export

Universities and VET providers ramped up recruitment quickly; international education is one of Australia’s biggest export industries. Student volumes hit new highs before reforms kicked in.

Very tight labour market

Employers needed staff in health, construction, hospitality and services. Skilled and temporary visas helped fill those gaps while local training and apprenticeships play catch-up.

What changed in 2024–25 – and why NOM is easing?

The government has already moved to “cool” migration without slamming the brakes:

- Student visa reforms – tougher integrity tests, higher English standards, more proof of genuine study, and a national planning level for student places (295,000 for 2026).

- More students finishing or leaving – as the backlog clears and conditions shift, departures have normalised, bringing NOM down from its peak.

- Treasury and RBA outlooks now assume migration trends lower, closer to historical averages, rather than 2022–23 surge levels.

In short: the policy pendulum has already swung. Future growth is expected to be smaller and more managed, with a focus on quality and skills.

How migration feeds into rents and prices

Migration shows up in the housing market in a few specific ways:

1. Immediate pressure on rentals

New arrivals generally rent first. That means:

- More demand for rental properties in inner-city and student-heavy areas.

- Tighter vacancy rates and faster rent growth, especially when supply can’t flex quickly

The RBA has consistently flagged that population growth is a key driver of underlying housing demand, particularly in the rental market.

2. The build-rate challenge

Australia’s housing target under the National Housing Accord is 1.2 million well-located homes by mid-2029 – about 240,000 per year. The problem is:

- Planning and approvals can be slow.

- Construction costs are high.

- Builders and trades are still stretched.

When migration jumps quickly but construction can’t keep pace, you feel it in rents first, then prices, especially in the cities where jobs, universities and infrastructure are concentrated.

This lines up with what we’re seeing now:

- Record or near-record prices in many capitals.

- Very tight rental vacancy in a lot of suburbs.

- Investor lending at record levels, as investors respond to strong rents and limited stock.

Migration is one part of that story. Limited supply, slow build-rates, and investor behaviour are the other big pieces.

The longer-term economic impact

From a budget and broader economic point of view:

- Higher migration can improve long-term fiscal sustainability, because it usually adds more working-age taxpayers.

- Outcomes depend on the skills mix, employment rates and how well people settle into the labour market – and into their local community.

- International education remains a big export and employer, but policy is now trying to balance that benefit with system integrity – keeping out “ghost” enrolments that are really just a pathway to work.

What this means for you (in simple terms)

If you’re renting / first-home buying:

- Expect ongoing pressure on rents, even as migration cools, because supply is still catching up.

- The expanded 5% deposit pathways and targeted government schemes matter more when rents are rising.

- Getting clear on borrowing capacity and realistic price ranges is key – especially in cities where migration is concentrated.

If you’re upgrading or downsizing:

- Population growth and low supply can support prices in many areas, but conditions are patchy by suburb and property type.

- A careful sell-then-buy or buy-then-sell strategy matters more when markets are tight and moving.

If you’re investing:

- Migration fuels long-term demand for housing, particularly in high-jobs, high-study regions.

- The real question isn’t “will people come?” so much as “where will they need housing, and how much new stock is being delivered there?”

Cash-flow, buffers, and the right structure (loan type, offset, splits) matter more than trying to guess next year’s NOM number.

I'm An AI Junky! Find Out What AI Thinks About AI

I love the fact AI can give me far more information, far more quickly, than my old Google searches could ever manage in hours or even days.

And, dare I say it, AI is transforming the broker world. With really smart software tools and analytics, the world has changed massively over the past year or two. I can now present a deal faster and more confidently that it is right, with a higher level of research and lender choice included. The bad old days of ‘You are a CBA customer’ are dead – long live the king!

So, back to the topic, I asked my AI “buddies” to analyse which AI programs they’d actually recommend, and why. I even got them to challenge each other so we could narrow it down to the “best of the best”.

Now, we all know things change fast, so think of this as a snapshot in November 2025. By November 2026, the AI landscape will almost certainly look very different – but this gives you a practical “state of play” right now.

Why choosing the right AI matters

Most people now have access to AI in some form – on their phone, inside their email, or via a website.

The trick is not “should I use AI?”, but “which AI is best for this job?”

Pick the right one and you:

- Save time.

- Get better, more reliable information.

- Write clearer messages and documents.

- Avoid oversharing personal data in the wrong place.

A simple rule of thumb

Here’s the short version my AI helpers agreed on:

Perplexity – best for up-to-date info with links you can click and check.

ChatGPT – best for clear, well-structured writing (emails, letters, blogs, applications).

Claude – great for very clean, human-sounding writing and neat lists/checklists.

Gemini – handiest if you live in Google (Gmail, Docs, Drive).

Copilot – handiest if you live in Microsoft 365 (Word, Excel, Teams, Windows).

Examples of how to use AI in day-to-day life:

Trip planning

- Perplexity to get recent travel info, ideas, and links.

- ChatGPT or Claude to turn that into a simple 3-day or 7-day plan with times, rough costs, and options.

Shopping decisions

- Perplexity to compare products and pull in reviews/specs from current sources.

- ChatGPT/Claude to summarise the trade-offs and give a short “If you’re this kind of person, choose X; if you’re that kind of person, choose Y.”

Writing better emails and letters

- ChatGPT for the main structure and tone (complaints, requests, school notes, job emails).

- Claude if I want it to sound extra natural and calm.

Study help for kids (or adults!)

- ChatGPT/Claude to simplify tricky topics and generate practice questions.

- Perplexity if we need sources or references to cite.

Home and life admin

- Claude to turn chaos into checklists – packing lists, weekly routines, renovation steps.

- ChatGPT to create variations (gluten-free meals, 30-minute dinners, “holiday version” of a schedule).

Tech troubleshooting

- Perplexity in finding the latest fixes from forums and support sites.

- ChatGPT to rewrite those fixes into a simple, step-by-step checklist I can follow. I have also used Chat to provide complex Excel formulas (“I want the spreadsheet to show xxxx. Can I give you the spreadsheet and can you please create the formula to give this result?’ eg the coloured arrows in the Best Rates section – all Chat-generated!.

Using AI safely and sensibly

A few non-negotiables my AI “panel” all agreed on:

Protect your privacy: don’t paste in tax file numbers, card details, licence/passport images, or extremely personal info into public chats.

Ask for Australian and recent info: for anything time-sensitive, say “prefer Australian sources, use exact dates” so you can see what’s current.

Check before you act: if health, legal issues or serious money decisions are involved, treat AI as a starting point only and verify with proper sources or a professional.

Keep a record: save important AI outputs and the links you relied on, especially for big decisions.

Remember you’re in charge: AI drafts – you decide. If something feels off, ask it to show its assumptions or to try a different angle.

Free vs paid – when is it worth it?

In most cases, free is enough if you:

- Ask a few questions a week.

- Just need short emails, summaries, or one-off help.

- Don’t upload big files or run very long chats.

It can be worth going paid if you:

- Write a lot (reports, proposals, long emails) and want better reasoning and tone control.

- Keep hitting limits on message length, file size, or speed.

- Want deeper integration (Gemini in Google Workspace, Copilot in Microsoft 365).

- Do regular research and need citations and bigger context windows.

Easy rule:

Start free. If you keep bumping into limits or wasting time, trial a paid version for a month and see if it earns its keep.

A few prompts for you

Some ready-made prompts that work well across tools:

Perplexity (for research with links):

“Past 60 days: simplest explanation of <topic>. Give 5 bullet points with source links.”

“Compare three reputable sources on <question>. What do they agree on? Where do they differ? Include links.”

ChatGPT / Claude (for drafting and clarity):

“My business is xxxx, and I am an expert in xxx” – the more detail about you, your customers, target markets, website links, etc, the better.

“You are an expert in xxx.” – use this in every prompt!

“Rewrite this in friendly Australian English, Year 10 reading level. Keep it to about 200 words. Add a 1-line summary at the top.”

“Turn these dot points into a clear email. Keep it polite but firm. Add three options for next steps.”

“I need this article to be created into a social media post. Please complete this post with headings, call-to-actions, and hashtags.”

Gemini / Copilot (inside Docs/Word):

“Add headings, shorten long sentences, and include a 3-bullet ‘What this means for me’ section.”

For now (late 2025), the sweet spot looks like this:

- Use Perplexity to find and verify.

- Use ChatGPT/Claude to reason and draft.

- Use Gemini or Copilot to finish inside the tools you already use every day.

And if you’re still unsure, start with just one or two, stay on the free plans, and let them “earn their way” into your daily routine.

Holiday Tips From The Experts: Fun, Sun, and Home Sweet Home

Justine Daly, Hypnotherapist and Website Developer – You Hypnotherapy and Happy Path (respectively)

- Use AI to sketch out your trip, but always double-check the details before you lock anything in.

- When using AI, check and confirm opening hours, ticket prices, and addresses on the venue’s website so you do not turn up at a museum that never existed or a theme park that closed five years ago.

- If you have a fear of flying, hypnotherapy is your passport to freedom (and yes, in her role as a hypnotherapist, Justine can assist you).

Ashton Wilson, Osteopath – Alpha Sports Medicine

- Keep your body moving (but don’t overdo it).

- Stay consistent with gentle daily movement – a walk with the family, a swim with friends, or a light stretch.

- Avoid going from “couch to hero” with holiday sport; warm up properly and build up slowly to reduce the risk of injury.

- Stay hydrated and take regular breaks if you’re out in the heat.

Yanal Shyamji , Renovator Kitchens and Bathrooms – Triple Zero Constructions

- Protect your home before you go away.

- If you’re heading away, turn the water off at the mains to reduce the risk of a burst pipe while you’re gone.

- Do a quick walk-through before you leave: check windows and doors are locked, and appliances that don’t need to be on are switched off at the wall.

- If you’ll be away for a while, ask a neighbour to keep an eye on the property and collect any mail, or pause mail deliveries at Australia Post.

- Don’t leave your bins out – if they hang around for too long, everyone will know you are not there.

Marianne Davies, Strategic Bookkeeper – Ideal Calculations

- Get your business cash flow holiday-ready.

- Create a simple cash flow forecast so you know you’ve got enough funds to cover general expenses and staff annual leave over the Christmas/New Year period.

- If the forecast is tight, talk early to your bookkeeper, accountant or finance broker about short-term funding to carry you through the break.

- Don’t forget to allow for slower debtor payments over the holidays – many customers close or run skeleton staff.

Trish Moore, Buyer Advocate – Hidden Gems Property Scouts

- Use the quieter weeks to get property-smart.

- Review your landlord and building insurance so you’re clear on what is and isn’t covered during storm and holiday periods.

- Get ahead of potential plumbing issues (slow drains, ageing hot water, dripping taps) before trades go on break.

- Take advantage of the quieter property period – motivated sellers and less competition can mean better buying opportunities if you’re ready to move.

Andrew Forder, Commercial and Resi Plumber – WPG Plumbing

- Holiday plumbing and home-maintenance checklist.

- Clean all gutters around the house so they’re clear before the next summer storm.

- Turn off or isolate the water when leaving home – braided flexi-hoses can fail without warning, causing major flooding.

- Turn off hoses and irrigation if they’re on timers, so you don’t come back to a flooded or overgrown garden.

- Check for leaks in taps, toilets and under sinks; fix small issues before they become emergencies.

- Inspect appliances (dishwasher, washing machine, fridge water line) for signs of wear on hoses and connections.

- Turn off the hot water system if you’re away for an extended period (check the manufacturer’s advice).

- Check pumps and pits (sump pumps, stormwater pits) and clean them out so they can cope with heavy rain.

- Disconnect garden hoses from outdoor taps to reduce pressure on fittings.

- Update insurance and emergency contacts so you know exactly who to call if something goes wrong while you’re away.