Want to invest in property but not sure where to start?

You’re not alone. Many Aussies are searching for property investment tips that cut through the noise and offer real value. In this guide, we cover essential strategies every investor should know—from how to assess your financial position to setting clear goals and knowing when to hold, upgrade, or sell.

- Best interest rates

- Women of Oz – a worthwhile cause

- Wills – Simple Trusts Vs Testamentary Trusts

- Buffett’s wisdom

- Renewable benefits you won’t see in the mainstream media

- Your property investment journey guide

- Starting a business? Three innovative contributions

- Sharemarket rises and falls are not new

- The future of cars (and it’s not Cars 4)

- ATO debt defaults & business failures

- Home loan deals for essential workers

- High LVR loans – good or bad for you?

- More listings hitting the market

- 5 ways to add equity to your home

- RBA keeping eagle eye on inflation

Best Rates

- All lenders on our panel have now reduced their rates since the RBA Cash Rate reduction of 0.25% pa on 18 February. That was over a month ago.

- Some lenders only reduced their rates on 26 March (for example).

- If / (when?) rates drop again, then based upon recent experience, you might find you are waiting up to six weeks to get your rate cut.

- Plus, when a lender announces their rate decrease and when they implement the rate cut…. well, there can be three or four weeks in between. No doubt lenders will have good logistical reasons for this delay but I do wonder about the potential positive impact of this delay on their profits (just saying….).

- The rates below exclude clean energy rates, first home buyer rates and packages and construction loan rates and an offset feature (where applicable).

- Interestingly (and I am not sure why), the rates below for Owner Occupiers are slightly higher than last month. Profit taking by lenders? Global uncertainty? Election fever? Who knows!

Owner Occupiers

- Fixed Rates: from 5.64% pa – 2 and 3 year terms – last month: 5.49%

- Variable Rates: from 5.64% pa – last month: 5.58%

- Fixed Rates: from 5.74% pa – 2 year term (last month: 6.24%)

- Variable Rates: from 6.14% pa (same as last month)

Investors

- Fixed Rates: from 5.74% pa – 2, 3 and 5 year terms (same as last month but now includes 3 and 5 years at this rate)

- Variable Rates: from 5.79% pa (same as last month)

- Fixed Rates: from 5.64% pa – 2, 3 and 5 year terms (same as last month but now includes 3 and 5 years at this rate)

- Variable Rates: from 6.09% pa (last month: 6.08%)

Women of Oz: a worthwhile cause

Wheels 2 Freedom Fundraiser

Wills - Simple Trusts Vs Testamentary Trusts

- To ensure your assets are managed and distributed according to your wishes.

- Affording asset protection and tax effectiveness for your beneficiaries.

- The most common form of will.

- Good for simple and smaller estate distributions – cost effective and timely.

- Distributes assets directly to the named beneficiaries.

- Outlines how your assets are to be distributed – often as ‘simple gifts’ to your beneficiaries.

- One or more trusts are created upon your death.

- A trustee manages and controls these trusts as well as the distribution of the assets and income to the beneficiaries of the trust.

- Good for when beneficiaries are under what you have deemed their preservation age – or they are a minor – so the trust assets are held until they reach the required age.

- Beneficiaries have the option of taking their inheritance inside a trust structure or taking their inheritance in their personal names.

- Beneficiaries can stream income and capital (i.e. assets) generated by the trust to other beneficiaries (such as partners or children). This is good for tax planning.

- The beneficiaries’ inheritance (income and assets) is protected from their creditors as well as legal claims and potentially family law-related issues.

Buffett's wisdom

His guiding principles

Integrity is a non-negotiable

He once said, “In looking for people to hire, you look for three qualities: integrity, intelligence, and energy. And if they don’t have the first one, the other two will kill you.”

Honesty pays off

Being honest isn't just about moral integrity—it's also a powerful productivity tool. Honesty saves energy that would otherwise be spent on hiding mistakes, bending the truth, or fearing discovery. It sharpens focus, boosts efficiency, and enhances confidence in every task. Moreover, honesty cultivates clearer communication. By being upfront, you sidestep needless conflicts and misunderstandings, paving the way for smoother teamwork and more effective leadership.

Generosity leads to more success

Generosity may not boost your bank account directly, but it has a powerful impact on your career, reputation, and happiness. Studies show that giving to others increases happiness, and happier people are more motivated, productive, and successful. In fact, people find more joy in spending money on others than on themselves, which encourages further generosity. Generosity also strengthens relationships. It fosters deeper connections and creates opportunities for collaboration, mentorship, and growth

Recent articles on deciphering Buffett's investment strategy

- In 2024, Berkshire Hathaway sold $134 Billion of stocks and built up its cash pile.

- Berkshire Hathaway has built up cash reserves of $334 Billion (yep, you read that correctly).

- Berkshire Hathaway has repurchased its stock for 24 consecutive quarters (that’s 6 years straight) – before breaking this streak in the last two quarters of 2024 – is his own stock too expensive?

- Over the last 6 weeks, Berkshire Hathaway’s increased its holdings of 8 of its ‘forever stocks’ (stocks he has no plans to sell): Coca-Cola, American Express, Occidental Petroleum and 5 Japanese trading houses (Mitsubishi, Itochu, Mitsui, Sumitomo and Marubeni.

- 47% of Berkshire Hathaway’s $283 Billion stock portfolio is invested in just 3 companies: Apple, American Express and Bank of America.

Closing observations

- Most media tipsters get it wrong more often than they would care to admit. (It’s a bit like most bank economists get the housing cycle wrong when there is a movement in interest rates).

- Tipsters may have self-interest at heart.

- They are like a sophisticated taxi driver. Listen to what they say then do the opposite.

- Fundstrat Global Advisors cofounder Tom Lee noted: in 2024, the market’s 10 best days added up to 20 percentage points for the S&P 500. But excluding those 10 days, the index was only up 4%.

Renewable benefits you won't see in the mainstream media

- Glass Almanac: A groundbreaking study at a large solar installation in the Talatan Desert shows that solar panels do more than capture the sun’s energy. They also impact soil conditions, promote vegetation growth, and influence the local climate. These findings could shift our understanding of how renewable energy interacts with the environment.

- news.com.au: In a one-minute clip on TikTok, the Chinese-made SUV backs into the exchange station, which is about the size of a car mechanic’s bay and waits as a new battery is uploaded from a basement below the station – all within one minute. Just think about that for a minute.

- Renew economy: as batteries become bigger, and with longer storage durations, their influence on the balance of supply is becoming more obvious. In South Australia’s evening peak, up to 20.8% has been supplied by batteries. This is only going to grow – fast.

- Sustainability Times: Chinese scientists have unveiled a new battery material (Niobium Tungsten Oxide – who would have thought…. 😉 ) that charges in seconds without compromising capacity or lifespan, promising to dramatically reduce charging times and enhance energy efficiency.

Your property investment journey guide

Decision #1: Hold

The property is showing the anticipated income and capital returns and no changes are expected in the near future.

Decision #2: Upgrade

The property needs maintenance and/or capital works to retain the anticipated income and capital returns.

Decision #3: Sell

The property is no longer considered capable of retaining the anticipated income and capital returns and it is better to reallocate your equity to a project more in line with the returns you are seeking.

Assess Your Financial Stability

Before making any big decisions, make sure you're financially secure. Buying an investment property involves significant upfront costs and ongoing maintenance, so it’s important to ensure you're prepared for this commitment.

Set Clear Investment Goals

Have a clear idea of what you're aiming to achieve. It’s crucial to discuss your goals with a financial advisor. Remember, all investments carry some level of risk, and real estate is no exception. Know your objectives and align them with your financial capacity. This is where the research starts to kick in.

Consider the Time Commitment

Property management requires time and effort. Are you ready to take on the responsibilities of being a landlord, or would you prefer hiring a property manager to handle the day-to-day tasks?

Get Pre-Approved

Securing pre-approval from a trusted lender is crucial. It helps you understand your budget, streamlines the buying process, and gives you peace of mind knowing what you can afford.

Understand Market Trends

The real estate market can be tricky to navigate. Stay informed about current market trends to make educated decisions about your investment.

You need a team

Think of property investment as being a business as that is what it is - it's a business based upon property generating you a return on income (via rent) and a return on capital (via property price increases). When you think of property investment as a business, you need the right professional team before you start. Gaurav requires clients to have the following professional advisors:

- Tax accountant – for tax effective structures and tax planning.

- Financial Planner – for risk mitigation via insurance.

- Broker – to organise the finance pre-approval so you can buy with confidence.

- Property Manager – to manage the property to make sure the income stream stays strong and consistent.

- Legal advisor – to handle the conveyancing as well as the more complex documents which can be part of the purchasing process.; plus of course important documents like Wills and Estate planning.

- Property Investment Advisor – which is what Gaurav does.

The right mindset is probably the most important part

As with most things in life, the right mindset can help you succeed whereas the wrong mindset will hold you back. Gaurav wants to work with those clients who want long term growth and long term relationships underpinning that growth.

Only 10% of what Gaurav does is involved in the purchase of property

Gaurav spends most of his time with the Planning and Assessment phases. Once he understands your objectives and he can see what you want is feasible and achievable, he will then go to work to find the right property which will fit your objectives.

Starting a business?

Three innovative contributions

- “I’m thinking about starting ‘X’. Can you find me a business model?”

- “Who should be my first customers?”

- “What do they care about most?”

- “Who should I test these hypotheses on and how can I find them?”

- Underprice your services: it is difficult to raise prices once you have set a low cost precedent. Jenny had to close.

- Failing to accurately account for your time: scalability gets you a return on your time.

- Value your time: the opportunity cost of your time needs to always be a touchpoint when you are doing something. What else could I be doing which could be creating more value?

Sharemarket rises and falls are not new

- Corrections often deepen: a 10% drop turns into a 13% decline about 80% of the time.

- 48% of corrections since 1945 escalated to a fall of 15% or greater.

- The data shows that less than 30% of corrections turn into bear markets.

- Bear markets are definitely not fun but corrections can be considered just a ‘cost of doing business’ as on average they’re recovered in just 4 months.

- Bear markets typically require a recession or a couple of quarters of negative GDP and earnings to take hold.

- The average bear takes two years and two months to come out of hibernation and regain their highs.

- The good news? Markets tend to roar back after hitting bottom.

The future of cars (and it's not Cars 4)

- Some Chinese brands may struggle to establish themselves in Australia and could eventually withdraw from the market as well.

- It is highly likely that some established brands will exit the Australian market, unable to compete with Chinese counterparts.

ATO debt defaults & business failures

- Electricity, gas, water and waste services: 52% of defaults

- Information, media and communication: 47%

- Mining: 42%

- Food: 41%

- Retail: 36%

Lenders Offering LMI Waivers To Some Essential Workers

- High LVR loans come with a higher interest rate and more than likely, LMI – an insurance premium paid by the borrower to protect the lender.

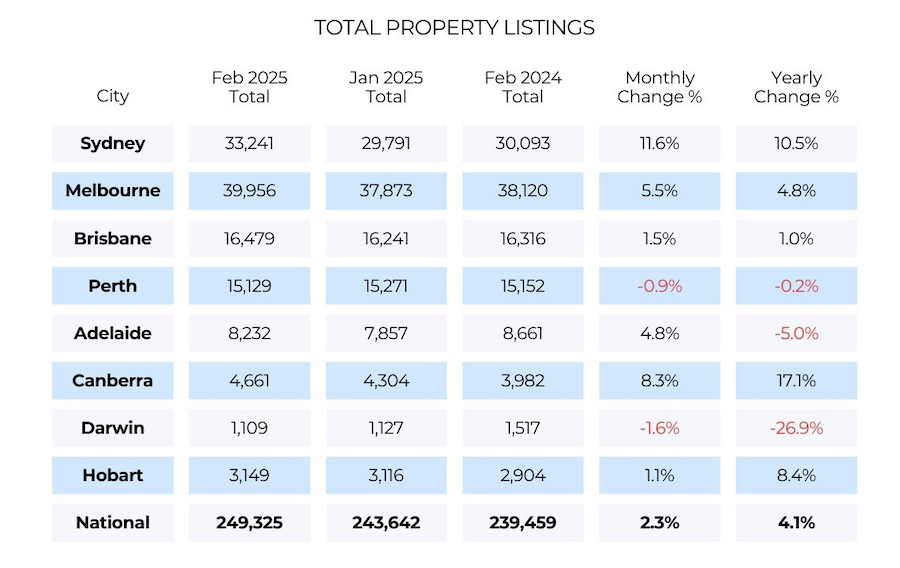

More Vendors Listing Their Home For Sale

How To Increase The Value Of Your Property

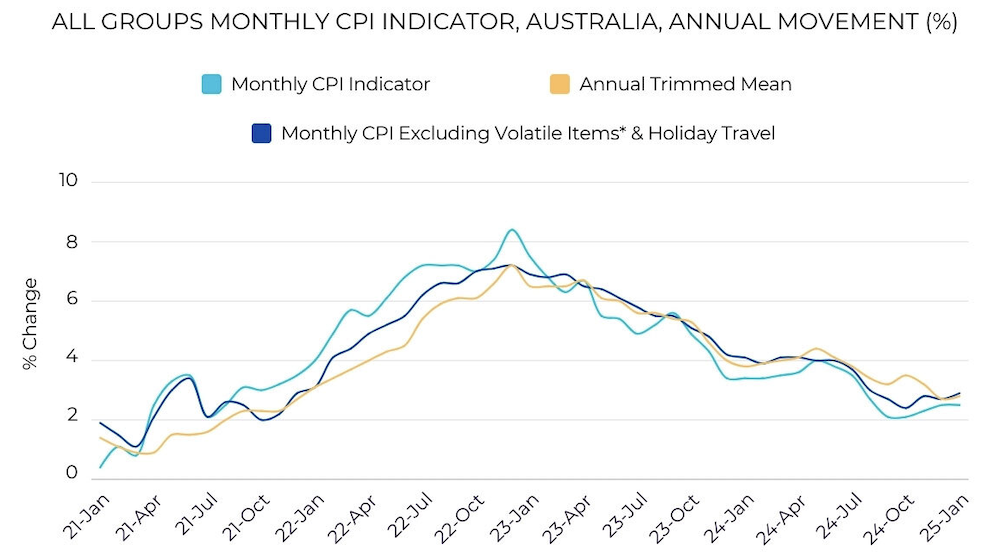

RBA Keeping Eagle Eye On Inflation