It’s halfway through the year if you are a January to December type of person – or it could be Happy New Year to you 🥳 if you prefer the fiscal equivalent.

And, another cold snap and you gotta say, Melbourne is a great place to live! 🥶 Sometimes I wonder how those in WA and Queensland cope with the balmy weather during the winter months 😂

Last month, we promoted three businesses that we reckon are good examples of what we are doing well in Australia: Wishkeeper (all your documents and memories in one secure location), Women of Oz (looking after women in need), and Gauci & Co. Wine Tours (accessing wine tastings in Victorian regions as well as your favourite location for a byo type of wine tasting).

Let me know if you would like further information

on these three great local businesses.

In this bumper issue

We have the latest home loans and interest rates news for you, as well as a tax update for property investors given that tax season is just around the corner. Here are the headlines:

- Best Rates

- Buyer Advocates save you money and time (and stress)

- Three less common loan products

- Rate outlook remains uncertain

- Property investor tax alert – How to avoid the ATO’s scrutiny

- 23.8% of borrowers have large loans

- Banking reforms announced

Date: as at 25 June

Owner Occupiers:

- Fixed Rates from 5.69% – 3 years Fixed (Principal & Interest) and 6.19% 3 years Fixed (Interest Only).

- Variable Rates from 5.88% (Principal & Interest) and 6.34% (Interest Only – non-construction loans).

Investors:

- Fixed Rates from 5.99% – 3 and 5 years Fixed (Principal & Interest) and 6.14% 3 years Fixed (Interest Only)

- Variable Rates from 6.18% (Principal & Interest) and 6.34% (Interest Only – non-construction loans).

Buyer Advocates save you time, money (and stress)

Those who regularly read my updates on the Property Reports feature (now quarterly) will know that I am a BIG fan of using buyer advocates.

There are those advocates who specialise in investment properties. Like Gaurav Bhatia, Equimax Property Group and Sharon Taylor, Performance Property Advisory. For these professionals, it is all about the dollars and cents return you can get on your investment. They like clients who are less emotionally attached to the property and more emotionally attached to their bank account 😉

On the other hand, you have buyer advocates who focus on the home owner market. They know the decision you are making has to be right for you. Emotion is higher and they work with you and what is important for you. We work with a few in this space and recently we engaged Trish Moore from Hidden Gems Property Scouts who also heads up our Property Concierge service. This is a free service for home buyers and Trish will spend an hour (or more!), assisting you make the right decision.

BIR Finance Property Concierge

If you are looking to buy a home anywhere in Australia,

Trish and her team will work with you

to get you the right property – for you.

Plus, there are so many more excellent buyers agents we have met and who are keen to help get you into your ideal property – whether to live in or rent out.

In the meantime, to get in contact with Gaurav, Sharon or Trish, just let me know and I will organise an introduction for you.

Three less common loan products

Superfunds Overpaying Their Lenders

Those of us with self managed super funds have historically looked at ways to outperform the market. And a leveraged property-backed loan was a good solution.

The only trouble is that in recent times, the lenders who provided these funds are now no longer in this space. And guess what? They are quite happy charging their clients a premium!

We are now helping quite a few owners of SMSF property loans refinance their SMSF loan to get a better deal (around 3% in the most recent cases).

Property finance I’m not prime 😢

We have had quite a few deals where the solution needed a lo doc lender or private lender.

Lo doc lenders are very useful for the self employed and those with incomplete tax returns. And, the rates can be quite reasonable – higher than a prime rate but not outrageous (from 7.24%).

And, if your circumstances improve, we can assist you refinance to a lower rated product (and some of these lenders will graduate you to one of their lower-rated products as your situation improves).

Private lenders will lend on very different criteria than a typical residential lender so they can fit all different kinds of deals.

They will often require the borrower to be to a company but apart from this, they can be a quick source of funds when you don’t qualify as that pristine prime borrower.

Businesses: Urgent Cash Needed!!!

Businesses need cashflow to grow and survive.

And, we have the perfect solution for those ‘Quick, my business needs some funds now!’ situations.

Think stock order, marketing campaign, employee payout, or just ‘an emergency’.

Because of the low cost to set up and hold this facility in place, we are recommending to clients ‘Set it up now so it is available when you need it’.

And if you have a property in your own name and you have a ‘not bad’ credit history, then we can arrange finance for anywhere from $5K to $300K with the provision of your bank statements! Simples 🤗

But wait, there’s more! See the bit below 👇

Urgent Cash needed for my business

Continued from above 👆

For businesses with a lumpy invoice to pay, there is also an interesting loan product that pays your supplier upfront but breaks your repayments into four installments. You pay a quarter of the supplier’s invoice upfront, and then the three remaining quarterly payments are paid over the next 90 days. Your supplier gets paid on time, and you even out your cashflow with payments over three months for a once-off fee of 4.5%.

It is quick and simple to use. LUCA Plus is the lender and and you can find out more at the link below (just click the Sign Up button on the website’s task bar). When you start the application, enter the code BLB2024BIR. (This will win you brownie points 😂).

Give me a call with your tricky scenario

and let’s see if we can get you a great deal

0411 190 474

Earlier this year, many economists believed the Reserve Bank of Australia (RBA) might start reducing the cash rate in the third quarter of 2024. However, recent forecasts have pushed these predictions back, with some experts now anticipating the first rate cut won’t happen until 2025.

The Role of Inflation

Currently, inflation stands at 3.6%, and the RBA aims to bring it down to their target range of 2-3%. The primary goal of increasing the cash rate, which affects home loan and business loan rates, is to curb spending and reduce inflation. While inflation has dropped significantly from its peak of 7.8% in December 2022, it remains too high for the RBA’s comfort.

Conflicting Economic Data

Recent data shows mixed signals. On one side, the economy has slowed significantly, growing just 0.1% in the March quarter. Reduced economic activity means less spending, which should lower inflation. On the other side, the unemployment rate has improved, dropping from 4.1% in April to 4.0% in May. More people employed means more money circulating in the economy, potentially driving inflation up.

What’s Next for Interest Rates?

Given these conflicting signals, it’s hard to predict the future of interest rates. The RBA might even decide to increase rates further. Therefore, it’s essential to plan your budget with these uncertainties in mind.

Did you know there are 27 rental expenses you can claim? So say the experts at Duo Tax, quantity surveyors and tax depreciation experts. Have a read of their informative blog (and at the end of this article is a great offer from Duo Tax so read on!)

But, according to Rob Thomson, Assistant Commissioner at the Australian Taxation Office (ATO), most property investors are making errors in their tax returns, despite the fact that 86% use a tax agent.

The ATO has announced that it will closely examine investors’ tax returns this year. They will cross-check the information provided with data from banks, land title offices, insurance companies, property managers, and sharing economy providers.

“If you use a tax agent, make sure you let them know all about your rental property, including full records of your expenses. If you have a nagging question or something doesn’t make sense, make sure you ask your agent when you’re working with them,” Mr Thomson said.

“Rental property investments and taxation can get tricky, so it pays to get the right advice from the very beginning. Don’t rely on things you hear at a Sunday afternoon barbeque.”

Specific issues in the ATO’s spotlight

This year, the ATO is particularly focused on claims that may have been inflated to offset the increases in rental income (which for many investors, has increased markedly with the tight housing market).

Key things to make sure you get right:

- Repairs and maintenance Vs capital improvements. Repairs are deductible in the year they are incurred whilst capital improvements reduce your capital gain when you sell. Confuse the two and the ATO might come knocking 😯

- Overclaiming deductions (never!) The ATO believes that many investors over-claim deductions and fail to provide documentation to substantiate their expenses. This can lead to ‘issues’ during tax time….

But here is some good news….

Depreciation ‘done right’ can save you tax

Depreciation is available as a deduction for property investors that reduces your tax liability and can often result in a substantial cash flow advantage. Described as ‘wear and tear’ or ‘decline in value,’ the ATO allows property owners to make a claim on depreciation, which is often overlooked.

Sometimes, Investment Property owners might not have properly assessed the maximum depreciation allowance. This is where an expert in this area can assist you maximise your depreciation claim.

Special BIR Finance offer for you!

We have partnered with Duo Tax Quantity Surveyors who specialise in property depreciation, and can provide you one of their tax depreciation reports which normally costs $700 for $550 (incl. GST). Check our their website (https://duotax.com.au) as they do a whole lot more than just tax depreciation reports.

To claim this saving, click the link below.

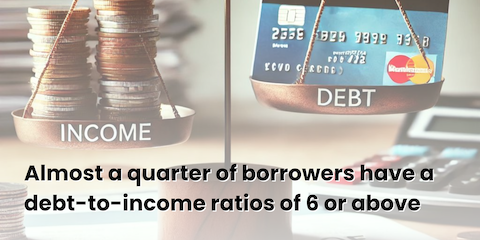

Qualifying for Higher Loan Amounts

With property prices continuing to rise, qualifying for a higher loan amount can give you more options. Recent banking statistics reveal how many Australians are being approved for relatively large loans.

According to the banking regulator, APRA, in the March 2024 quarter, 23.8% of new home loans (by value) had a debt-to-income ratio (DTI) of six times or greater. While this is down from a peak of 40.7% in December 2021, it indicates that lenders are still willing to extend significant credit to many borrowers.

For regular readers of my newsletters, you will remember that Phil Anderson from Property Sharemarket Economics predicted that borrowing would continue to expand, driving up property prices as we head towards the next property price peak in 2025 to 2026 – all part of the 18.6 year cycle Phil talks about.

Borrowing Power Variations

It’s important to note that borrowing power varies not only by individual borrower but also by lender. Two people with similar financial situations can have very different borrowing capacities with different lenders. Similarly, the same borrower can receive different loan amounts from different lenders.

Seeking Professional Guidance

If you’re planning to buy a property, it’s crucial to understand the lending policies of various banks. I can help you find the most suitable lender for your profile, considering the specific policies of each bank.

Mortgage lenders will be required to simplify the process for customers to switch loans. Under new banking reforms announced by the federal government, lenders must ensure customers have direct and easy access to the necessary information.

Improved Disclosure Requirements

Banks will also need to improve disclosure requirements for basic deposit products. They must inform customers when their interest rates change on their transaction and savings accounts.

Notification of Interest Rate Offers

The government plans to collaborate with banks to enhance how customers are notified about bonus interest rate offers and the end of introductory periods with special rates. This may involve developing industry standards.

Encouraging Consumers to Switch

Additionally, the government will direct Treasury to investigate how prompts could encourage consumers to switch to cheaper home loans and retail banking products.

Response to Consumer Watchdog Inquiries

These reforms are part of the government’s response to two inquiries conducted by the Australian Competition and Consumer Commission (ACCC).

Treasurer Jim Chalmers said these changes would “help bank customers get a better deal, including through more choice, lower prices and better services”.