Spring has sprung, which means we’re now in the midst of the busiest season in the property calendar. Here’s what’s making headlines:

- Best interest rates

- Spring listings are up: how to win without overpaying

- The art of property negotiation: buy well without overpaying

- Selling or buying: 5 hidden bathroom tiling problems – and how to fix them

- Affordability inching better + 1 October First Home Scheme changes

- Building vs buying in 2025: why the gap is finally narrowing (and what to do)

- Offsets at record highs: simple tweaks that save real interest

- Credit cards, BNPLs vs borrowing power: quick wins before you apply

- Caring for a long-held family home: when parents move into care or pass away

- Business owners: From knowing to doing: the owner’s execution system

- News media insights: Australian online news: ABC still No.1

- Nuclear vs renewables: what actually scales – for Australia

- Why we publish a “proper” newsletter – and how it helps you

Read more below.

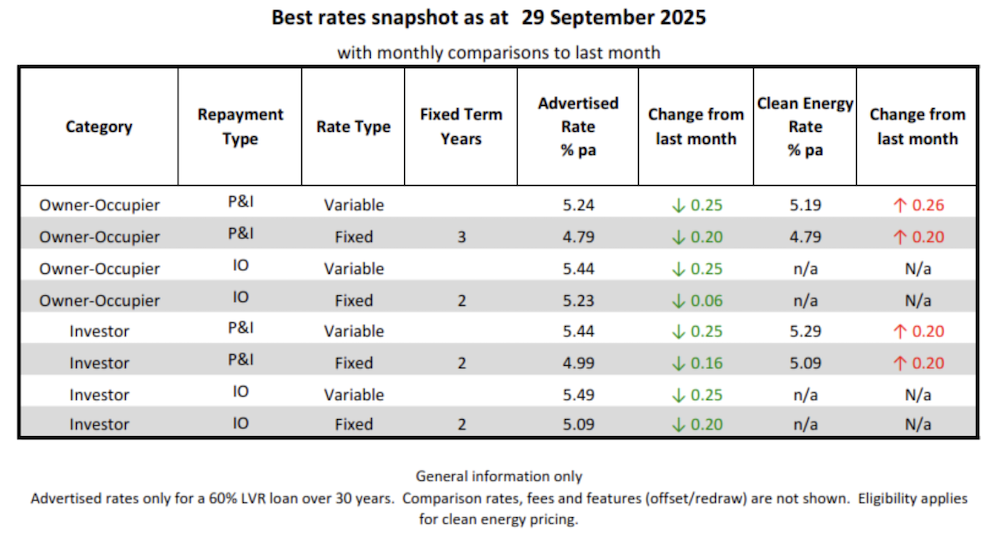

Best Interest Rates

Quick observations

- Broad easing: Most headline rates fell ~20–25 bps month-on-month (OO/INV variable and several fixed terms).

- Fixed still under variable: In this snapshot, 3-year OO P&I fixed (4.79%) and 2-year Investor P&I fixed (4.99%) both sit below their variable counterparts (5.24% / 5.44%).

- Clean-energy pricing narrowed: The “green” discount has shrunk materially: OO P&I variable shows a –5 bps edge (5.19% vs 5.24%), down from a much wider gap last month whilst Investor P&I variable holds –15 bps (5.29% vs 5.44%). No green pricing is available on the IO products in this list; and the Investor P&I 2-yr fixed now prices above the standard rate (+10 bps).

- IO options: Interest-only lines remain higher than P&I equivalents (as usual) and typically don’t carry clean-energy offers.

Notes

- Advertised rates only. Comparison rates are not shown; fees/features (offset/redraw, package fees) aren’t reflected—your effective cost may differ.

- Pricing assumes ≤60% LVR; other LVRs can price differently.

- Clean-energy/“green” pricing usually requires eligibility (e.g., energy-efficient home or approved upgrades) and may have extra conditions.

- General information only — no product or lender recommendations.

Reply “RATES” if you’d like an estimate of your best rates for your current or proposed loan.

Spring listings are up: How to win without overpaying

More properties are hitting the market, which means greater choice—but the best homes still sell fast. Get your ducks in a row so you can move quickly and avoid paying an “emotional premium.”

What the market’s doing – fast facts

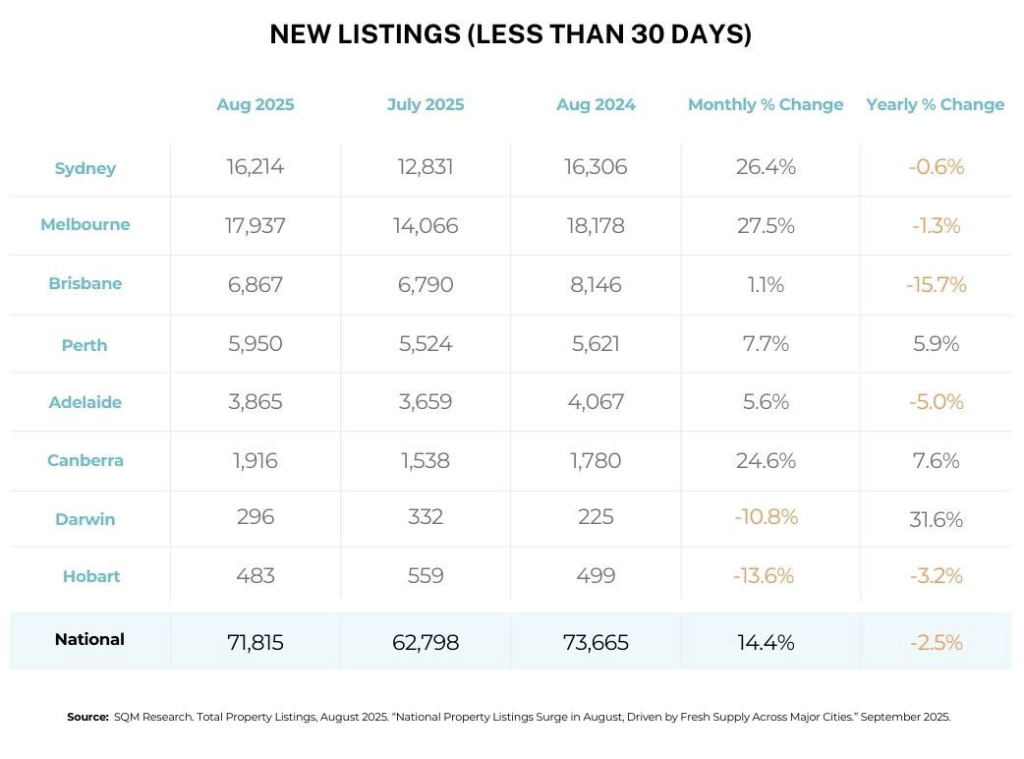

- New stock lifted in August and total listings rose month-on-month, led by Sydney, Melbourne and Canberra (classic spring pattern).

- Rental vacancy remains tight (national ~1.2% in May), keeping investor interest alive in select pockets.

- Rates: The RBA cut to 3.60% in August and is cautious near-term; borrowers should check their actual rate and ensure their lender has passed the rate cut through.

Spring is traditionally the busiest season of the year for property sales, and this year is shaping up accordingly, with SQM Research reporting a 14.4% month-on-month increase in the number of new listings in August. The number of homes for sale typically rises in spring as sellers look to take advantage of warmer weather and stronger buyer demand.

While the increased choice can benefit buyers, the competition can also be fierce. Sellers often receive multiple offers, which means buyers need to be well prepared if they want to secure their preferred home.

Our three-step buyer playbook

1) Finance first — pre-approval + buffers

- Get a current pre-approval and confirm how long it’s valid (typically ~90 days).

- Build price guardrails: your max bid number plus 1 to 2 fallback options so you don’t chase.

- Sell then buy? Map your bridging/contingency (timing, LMI, cash buffers). (PS There are new products that act like bridging loans without the usual hassles and delay of a bridging loan – and they aren’t expensive).

- Consider a Deposit Bond to secure the property without freeing up cash or selling first.

2) Search with intent — shortlist + due diligence

- Lock in 2 to 3 suburbs and target streets/buildings; attend opens early.

- Pull recent sales comparables (±5% of your target price) and set a walk-away number.

- Book pest & building (houses) or review Owners Corporation minutes + sinking/capital-works fund (units/strata).

3) Offer/auction tactics — play the tempo

- Private sale: a clean, dated offer with a finance clause aligned to your pre-approval can beat messy, higher offers.

- Auction: bid in firm increments; don’t telegraph your ceiling.

- Passed in? Negotiate terms first (settlement, inclusions, timing), then price.

Where value is showing up

- Renovation-needed houses on owner-occupied streets; older, larger units (healthy OCs) often sit below renovated peers. Get a reno cost band and net it off your price.

- Vendor motivation tells: multiple reschedules, long days-on-market, staged price guides — all can signal room to negotiate.

Risks to watch (and insure)

- Underquoting vs reality: always test the guide against the last 6 to 8 comparable sales.

- Insurance & location risk: flood/bushfire/storm overlays can lift premiums or exclusions.

- Under-the-house/invisible issues: stumps, drainage, electrical, plumbing, asbestos, blocked vents, and plumbing/sewer leaks can be costly to repair. And, they may make insurance either difficult to obtain (or your insurer may exclude pre-existing damage).

- Strata hazards: special levies for lifts/roofs in older mid-rise blocks, cladding claims, and major refurbishments.

Solution: a quality pest & building inspection (especially for older homes).

Need a good inspector? Drop me a line and I’ll connect you.

Buyer’s agent perspective — Trish Moore, Hidden Gems Property Scouts

“Overpaying happens when you’re vague, emotional, or swayed by FOMO.

The fix is clarity, evidence and matching the vendor’s motivations.”

Trish Moore, Buyer’s Agent, Hidden Gems Property Scouts

Trish’s four essentials for buyers:

- Clarity: Be specific about what and where you want to buy. Start with a brief. Trish uses a short “Buyer’s Brief Questionnaire” (each partner completes it independently) to surface differences and lock in a clear target.

- Value: Know what it’s worth. Appraise every candidate property with recent comparisons so your offer is strong, not desperate — and not insulting.

- Finance-ready: Turn intent into leverage with a current pre-approval. It speeds decisions and strengthens your position in private negotiations and post-auction talks.

- Win–win terms: Price isn’t everything. Understand the seller’s motivation (timing, settlement length, inclusions) and match terms to unlock a better overall deal.

How Trish’s tips fit our playbook:

Step 1 – Finance gives you speed + certainty.

Step 2 – Search gives you clarity + comps.

Step 3 – Tactics uses terms to win without overpaying.

Book a 30-min Pre-Purchase Strategy Call

Bring one live listing.

We’ll set your max number,

so you can plan your auction/private-treaty approach.

The art of property negotiation: Buy well without overpaying

A good search finds you options; good negotiation stops you overpaying.

The right timing, smart homework, calm emotions and creative deal structure can be worth tens of thousands. Neil Jenman (jenman.com.au) argues skilled negotiators can move the price by meaningful margins for vendors – sometimes around 10%, which is why sellers prize agents who can truly negotiate, not just run a campaign.

Mary Maatouk, Maatouk Property Advocates, adds to this logic with a couple of gems for buyers who are on the receiving end of a negotiator-savvy real estate agent (who, it is worth reminding, acts for the vendor, not the buyer) – and can give you an even greater advantage if the agent relies on the auction process to get the best result.

Four unbeatable negotiation tips

1) Timing: when silence says more than words

Silence after an agent’s counter can draw out concessions or extra inclusions. Make your point, then stop. This “strategic pause” is a classic tactic across negotiations because it shifts the pressure back to the other side to fill the space—often with useful information or movement.

How buyers can use it:

- After offering, say: “That reflects the recent sales we’ve seen. Happy to sign today if we can agree.” Then zip it.

- At auction-adjacent negotiations, don’t rush your counter; ask, “What terms would the vendor value most?” then pause.

Risk check: Silence isn’t stonewalling—stay courteous and responsive on logistics.

2) Homework: vendor motivations = real leverage

Price guides are noisy; motives are signal. Are the sellers already committed elsewhere? Chasing a long settlement? Fixated on a specific date? Your terms can trade for price.

Your quick research pack:

- Sales history: last sale price/date, days on market, price changes.

- Context: has the property passed in? Was there a recent fall-through?

- Motivation cues: tenancy ending, relocation, probate, long settlement noted in listing remarks.

Jenman pushes vendors to choose negotiators who can truly extract the top market price—not just accept the highest public bid on the day. The point for buyers: agents who negotiate hard for sellers raise the bar; your edge comes from knowing what else (besides price) matters to the vendor and trading for it.

3) Emotions: love the home, not the price

Falling in love with a kitchen is human; paying an emotional premium is optional.

Three guardrails to keep your cool:

- Walk-away number: set it before inspections (based on comparisons) and stick to it at auction or private treaty.

- Two options rule: always have a Plan B property. Choice limits FOMO.

- Bid choreography: at auctions, bid confidently and in firm increments up to your cap; if passed in to you, negotiate on terms first, not just dollars.

For sellers, Jenman strongly critiques auctions as prone to under-selling vs skilled private negotiation; whether you agree or not, the takeaway for buyers is to be auction-fluent and private-treaty-fluent—each format demands a different emotional tempo.

4) Structure: flexible terms can beat higher offers

Money talks, but terms sing. Many vendors value certainty and convenience.

Terms menu you can trade:

- Settlement: offer the date they want (long/short).

- Deposit: adjust size/timing (e.g., 5% on exchange, balance later).

- Conditions: quick building/pest, finance pre-approval already in place.

- Inclusions: be easy about minor fixtures, or offer a rent-back if they need time.

A lower price with the vendor’s perfect terms can beat a higher, messy deal. This aligns with Jenman’s long-standing view: real value comes from private negotiation skill, not just letting an auction’s top bid set the result.

Private treaty vs auction: what changes for buyers

Private treaty: Most room to use timing, silence and terms. Open with evidence; trade non-price terms first.

Auction: Your prep does the talking—pre-set your cap, plan your post-auction negotiation if it passes in (often where real deals are done). Jenman argues auctions can under-sell for vendors; as a buyer, understand that some agents will try to close quickly—be ready with your terms and comps.

Final thoughts

- Negotiation isn’t about “beating” the other side; it’s protecting your interests and shaping a deal that genuinely works. Do your homework, keep your emotions steady, and use terms creatively. That’s how you secure the home and keep cash in your pocket.

- Be ready with finance. Whether with a home or a car, having your finance in place gives you negotiating power. Subject to finance should only be your fall-back strategy when you can’t get organised in advance.

Selling or buying: 5 hidden tiling problems

How to spot them before they cost you

Tiling is one of those things people think about doing when they are selling (‘My bathroom looks a shocker!’, ‘My agent has asked to spruce up our 1960s bathrooms’) or buying (‘Before we move in, let’s start off with the right bathroom looking schmick’).

Recently, Milan Gala was referred to me by Yanal Shyamji, of Triple Zero Constructions, at triplezerogroup.com.au. Yanal is a kitchen and bathroom renovator, and Milan does a lot of his tiling work for him.

Milan operates a small bespoke tiling business. Milan’s father was a tiler, and he is a tiler. And not just a tiler either. Both Milan and Yanal are the types of tradies you want on your job. Decent, reputable, and experienced tradies who keep you in the loop and get the job done. And, both are reasonably priced. They won’t blow your budget.

After Milan recently fixed my grouting in two of my bathrooms, I was seriously impressed and thanked Yanal for the warm introduction. Because I love to put good content in this newsletter, I asked Milan for his thoughts on the most common problems people encounter when tiling their bathrooms. Read below to get the low down on what to look out for – and what questions to ask your tiler before they start (and if you want an intro to Milan, just let me know – fyi he is Melbourne-based).

Milan's top 5 tips to protect your bathroom—and your budget

Bathroom tiles can look fine on day one, then quietly fail months later. The most common culprits are waterproofing issues, mould, poor preparation, lippage (uneven tiles), and grout/silicone mistakes.

Waterproofing defects are consistently among the most costly complaints in residential building – so prevention beats cure.

Knowing what to look for (and what to ask your tiler) can save you thousands and keep your bathroom sale-ready.

1) Inadequate waterproofing – the silent, expensive problem

What goes wrong: Missed corners, thin membranes, no bond breakers, or poor drainage to the floor waste. Results: drummy/loose tiles, musty smells, swollen skirtings, and mould.

Why it matters: Wet-area waterproofing is regulated by the National Construction Code (NCC 2022) and AS 3740:2021. These set the rules for where membranes go, heights on walls, junction detailing, falls to waste, and connections to drains.

Quick checks during a reno:

- Ask for photos of the membrane before tiling (including upturns at walls and around penetrations).

- In showers, look for falls to the waste—AS 3740 guidance notes a typical minimum of 1 to 80 (1:80), where a floor waste is installed; falls that are too flat or too steep can cause problems.

- Confirm the membrane is correctly terminated at the drain connection (a common leak point).

- Be cautious when lifting tiles—removal can tear the membrane, forcing a full redo. Get professional advice before you start pulling tiles.

2) Mould and bacteria growth – often a symptom, not the cause

What goes wrong: High humidity + poor ventilation + micro-cracks in grout or failed silicone. Soap scum and body oils feed mould.

What to do:

- Improve ventilation (fan ducted outside, not just into the ceiling).

- Re-silicone corners and junctions where planes meet (wall/floor, wall/wall).

- Regrout with a quality, mould-resistant grout; seal if the product requires it.

- Treat the cause—check for leaks or ponding due to poor falls or blocked wastes.

3) Poor surface preparation – the root of cracks and loose tiles

What goes wrong: Tiling over dust, old adhesive, movement, or out-of-level substrates. Results: adhesion failure, cracked tiles, hollow sounds underfoot.

What “good” looks like – per standards guidance

- Substrates clean, sound, and flat to the tolerances in AS 3958.1.

- Correct adhesive coverage (notched trowel technique matched to tile size).

- Movement joints planned (doorways, perimeters, and at set spacings).

Why movement joints matter: Tiles and buildings move. Industry guidance recommends the use of properly detailed movement joints (e.g., at shower corners and where tiling meets other materials) to prevent tenting and cracked grout.

4) Tile lippage and unevenness = trip hazards and ugly edges

What goes wrong: Edges of adjacent tiles sit at different heights (lippage). Causes include uneven substrates, insufficient adhesive, large-format tiles laid without appropriate set-out, or trying to create falls to a waste without planning cuts.

How to spot it: Use a straightedge and check transitions under light—lippage shows as shadowed edges or catches your toe.

What the Standards say: AS 3958.1 provides guidance on tolerances and jointing; some lippage can occur, especially with larger tiles graded to a floor waste unless transverse cuts are used.

Fix options: Localised rectification (stone/diamond hone on some edges), or re-laying sections if lippage is severe—often linked back to substrate and falls planning.

5) Grout and silicone mistakes – small errors, big consequences

What goes wrong: Wrong grout type or mix, pinholes/gaps, grout where silicone should be (corners/movement joints), or stained grout from harsh cleaners.

Best practice:

- Use silicone at junctions where planes meet or movement is expected (e.g., vertical corners of shower compartments), and grout only in the body of the field.

- Match grout width to tile and pattern per AS 3958.1 guidance; keep lines consistent.

- After curing, follow the manufacturer’s cleaning instructions to prevent discolouration.

What to ask your tiler before they start

- Standards & scope: “Are you installing to NCC 2022 wet-area requirements and AS 3740/AS 3958.1 guidance? Please note this in the quote.”

- Membrane evidence: “Please provide photos of waterproofing stages (including bond breakers, upturns, and drain connections) before tiling.”

- Falls plan: “What falls to waste will you achieve in the shower (target ~1:80 to floor waste)? Will you use transverse cuts for large-format floor tiles?”

- Movement joints: “Where will you place movement joints and silicone junctions (e.g., shower corners, perimeters, transitions)?”

- Substrate prep: “How will you check flatness and adhesion coverage for our tile size? Any levelling/screed needed?”

When it’s already gone wrong....

- Hollow (‘drummy’) tiles: Get an assessment—lifting a tile may damage the membrane; you might be better off planning a controlled repair rather than ad-hoc removals.

- Persistent mould/odours: Investigate waterproofing and drainage first, not just surface cleaning.

No matter what your renovation, we’ll help you confirm your best finance options.

Postscript: We are working on producing a Checklist for Tiling – let me know if you would like a copy when it is ready. Just reply Tiling Checklist and I will add you to the list 👍

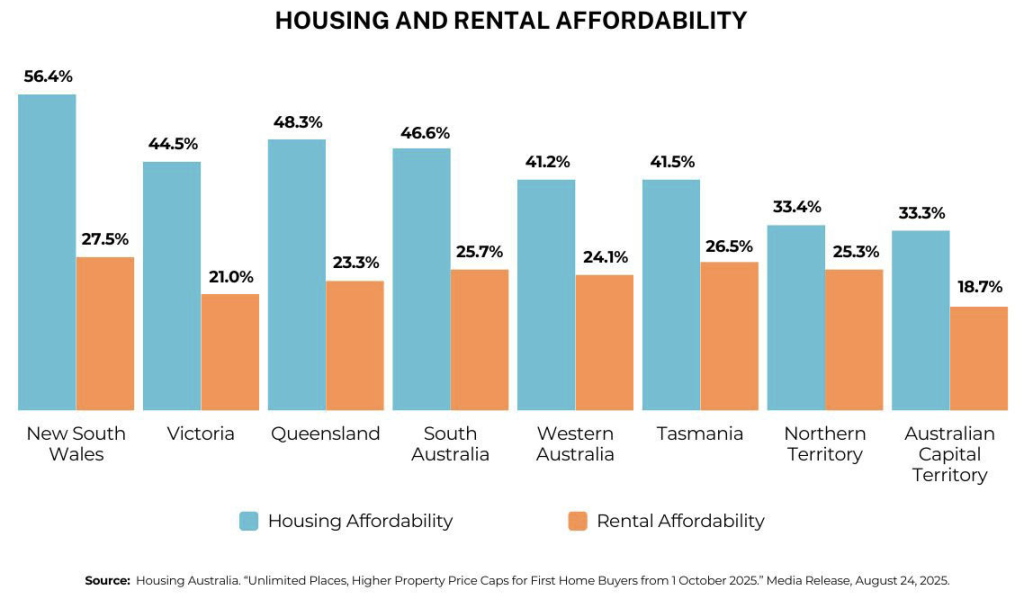

Affordability inching better + 1 October scheme changes

Repayments are slightly more manageable than late last year, and the Home Guarantee Scheme gets a major expansion on 1 October—opening the door for more first-timers and returning buyers.

The numbers to know

- Nationally, the proportion of family income required to meet average loan repayments fell to ~47.7% in the June quarter – the second improvement in a row since the December 2024 low point.

- WA bucked the trend (affordability slipped) due to strong price growth.

- The RBA’s August cut to 3.60% helps at the margin—check lender pass-through to your actual rate.

What changes on 1 October

Housing Australia confirms the Scheme’s expansion: unlimited places, higher property price caps, and no income caps. That’s a big capacity lift for eligible buyers.

Who could benefit

- Singles on moderate incomes who were previously above income thresholds.

- Couples where combined income exceeded old caps.

- Regional buyers who were constrained by lower price caps.

- Long-term renters aiming to buy with lower deposits under the guarantees.

How to use it – a simple pathway

- Suburb shortlist → check new price caps for your target LGA.

- Confirm deposit pathway (5% or 2% family guarantee variants) and borrowing capacity.

- Get pre-approval aligned to the new caps and be auction-ready.

- Don’t assume every bank treats the guarantee the same—policy differs by lender (rates, LMI treatment, servicing, plus the interpretation of Housing Australia’s guardrails!).

Contact me if you’d like to explore

whether you qualify for the Home Guarantee Scheme

and how it could help you enter the market sooner.

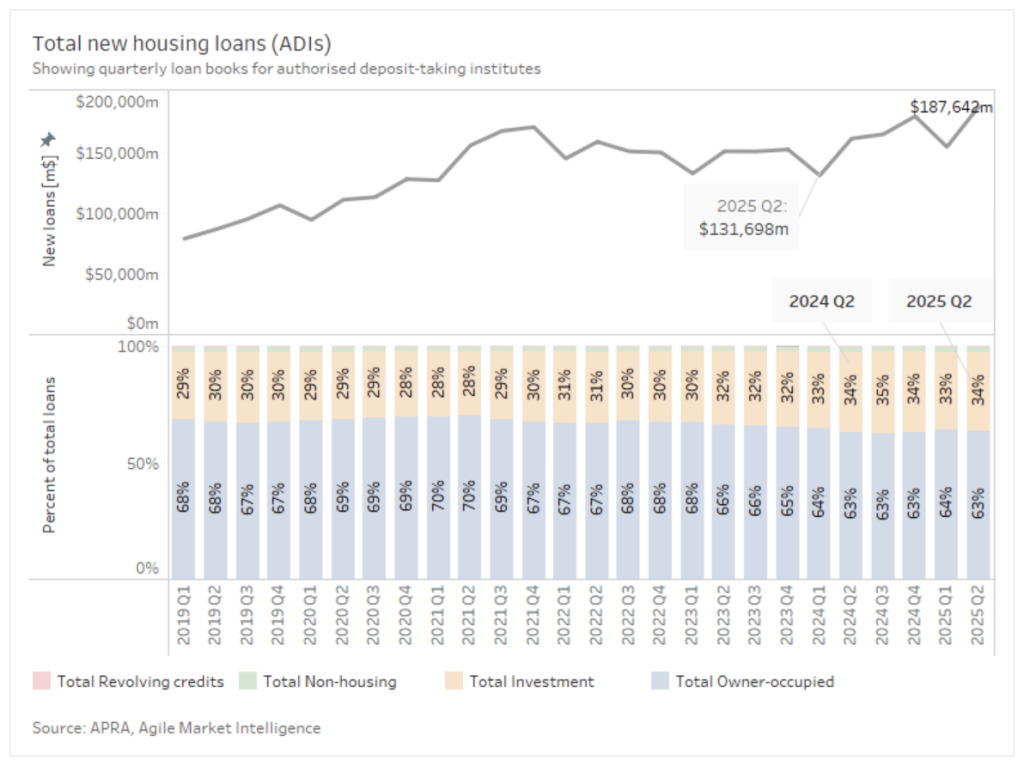

Meanwhile….. with improved affordability comes an increase in loans.

Broker Pulse together with Agile Market Intelligence, filed a report from APRA which covered a number of key findings from its research into ADIs (Authorised Deposit-Taking Institutions – there are over 135 banks, credit unions, building societies and even PayPal!)

Interesting findings:

- Lending has jumped 16% in the last quarter

- Owner Occupied dwellings make up the lion’s share of lending – 63%, whilst Investment Property loans made up 34% of all loans.

- Over 80% LVR loans (i.e. in the LMI territory but also in the Government First Home Buyer Deposit Scheme territory) dropped slightly to 30.4% of new loans.

- Loans with a high Debt to Income (DTI) ratio rose slightly to 5.5%. These loans fell when interest rates were increasing, so as interest rates fall, you would anticipate loans with a higher DTI would start to become more prevalent.

Offsets at record high: Simple tweaks that save real interest

With offsets near record levels, even small changes to how your salary and savings flow can shave thousands in interest across a year.

Offsets explained

An offset account is a normal everyday bank account that links to your home loan. The money you keep in it reduces the loan balance used to calculate interest. Example: loan $600,000, offset $40,000 → you’re charged interest on $560,000. That can cut mortgage interest and help you pay off your home loan faster.

What the data is saying

- APRA reports households continue to build buffers, with offset balances trending higher (as a share of credit limits) across the year.

- Media/industry tallies put offsets above $300B (June quarter), a fresh high.

Six quick wins you can do this week

- Do not use savings accounts! Full stop. Get offset splits set up to mirror your savings accounts. You save on interest, and you don’t get taxed on the interest you would have earned.

And if you insist on keeping savings accounts….

- Salary-to-offset: pay income directly into your offset; run expenses on a low-fee debit/credit card paid in full each month.

- Sweep rules: turn on automatic sweeps so any cash left in transaction accounts moves nightly into the offset.

- Check it’s a true offset: some “offset-like” accounts are actually redraw and it’s harder to get your money out. Ensure your product nets off daily interest.

- Don’t overpay for features: if the offset’s higher rate/fee exceeds the saving, consider a clean P&I split with an offset only on the larger portion.

- Parking lump sums: tax refunds/bonuses sit in offset until genuinely needed.

Structure tips for different borrowers

- First-home buyers: Start with a single big split + offset; keep the “future investment” split clean if you might convert to IO later.

- Upgraders: Use multiple splits to separate reno budget vs everyday cash; this keeps redraw/offset admin tidy.

- Investors: Offsets can preserve tax deductibility when you move homes (get tax advice) and, by keeping funds for different purposes in separate offset splits (eg personal Vs investment), your accountant will love you (and charge you less)

Disadvantages of an Offset account

- Home loans with offset features may come with higher interest rates and/or fees. In our experience, lenders who offer both loans with and without an offset account typically charge a few hundred dollars each year for the offset functionality.

- Compared to a redraw facility, offset account funds are easier to access. And for some of us, ‘easy to access’ is not good. So, putting surplus funds into a redraw can create some friction between wanting to spend and accessing the money. Similarly, funds placed in a savings term deposit will also increase the friction.

We can quickly calculate how much an Offset account can save you

so you can have a bigger smile at the end of each month!

🥰

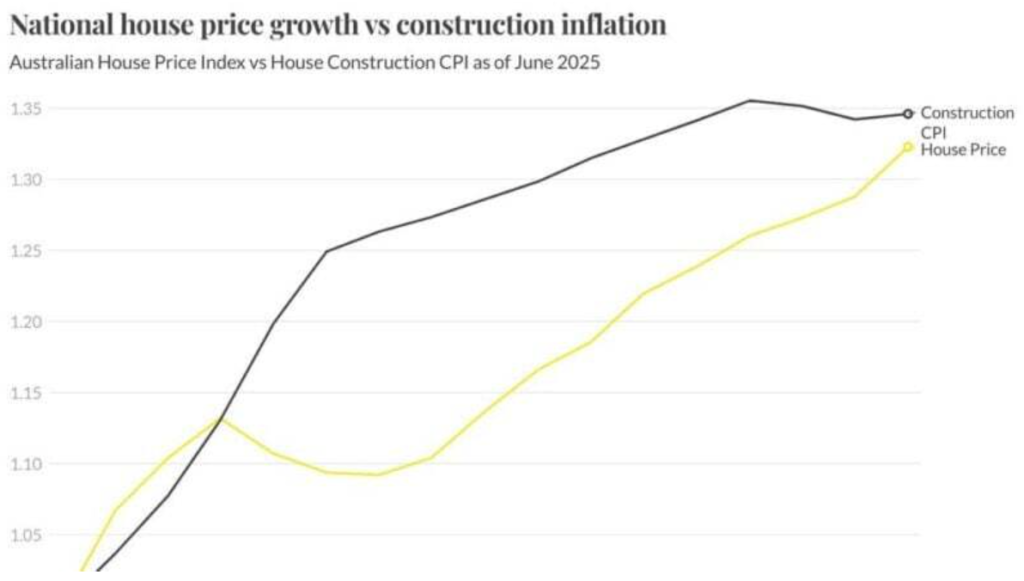

Building vs Buying 2025: Why the gap is finally narrowing (What to do)

Your options have opened up again

In his regular property update, Michael Yardney’s Metropole website has provided a timely update on Building Vs Buying.

We researched this issue and have accessed articles by Ray White, realestate.com.au, Cotality, ABS and HIA,

For the first time in years, it’s not always cheaper (or smarter) to buy an established home. With construction cost growth easing and home values rising, the price gap has narrowed; so building on titled land or a house-and-land package may stack up in more postcodes than it did in 2022–23.

What changed (the short version)

- Build costs cooled: Residential construction costs rose just ~0.4–0.5% in the March/June quarters 2025; annual growth around ~2.9%, well below the pandemic spikes. Builders are also using incentives again.

- Home prices re-accelerated: After a soft patch late 2024, values rose into 2025 in many cities—house prices in some capitals are now outpacing build-cost inflation, compressing the gap.

- Evidence across markets: Multiple wrap-ups (Ray White, realestate.com.au, PropertyUpdate) show the buy-vs-build lines converging through 2024–25, not just in one city.

Takeaway: It’s still cheaper to buy in most areas—but the advantage has shrunk enough that build-ready land + a sharp fixed-price contract can be competitive again.

But… two big caveats

- Land costs: Median residential land prices hit record highs in late 2024; what you pay for the block can make or break the build maths.

- Time & risk: Even with stabilising costs, builds can face delays (trades, approvals, titles). Factor rent/holding costs and add a contingency.

Who should lean towards building

- You can secure titled land (or short-dated titles) at a fair price and lock a fixed-price build with clear exclusions.

- You value new-home efficiencies (7-Star NatHERS, lower running costs) and a full builder warranty.

- You’re happy to trade time (build) for custom design and fewer immediate maintenance costs.

Who should lean towards buying established

- Location > floorplan: you need a specific school zone/transport now.

- The local land price wipes out the build advantage.

- You prefer certainty of timing (move-in date beats build-time risk).

Quick decision framework

- Build: land price + site works + fixed-price contract + upgrades + driveways/landscaping + rent/holding during build. Prioritise titled land, builder solvency, and true fixed-price inclusions (site costs, piering, rock allowance, bushfire/BAL, energy upgrades).

- Buy: purchase price + stamp duty + immediate reno/maintenance. Target properties where land value is the prize; be ready to move (pre-approval + guardrails).

Tips:

- Stress-test the build: add +5–10% contingency for variations/time.

- Finance check: some lenders treat progress payments differently to a standard purchase—serviceability and cash-flow matter.

- Model the cashflow of the two options (we can help you build a model)

- Resale lens: consider local buyer demand for new builds vs character homes in your target suburb.

- Timing: if you need to live in it within 6–12 months, the established option may still be safer.

We’ll run both scenarios with current lender policies, cash-flow over 36 months, and a suburb-level resale lens—so you can choose with confidence.

Credit cards, BNPLs vs borrowing power: Quick wins before you apply

Credit card limits are key

One of the fastest and quickest ways to improve borrowing power is to reduce unused credit card limits (or close spare cards).

Lenders look at all your credit when assessing a home loan—including credit cards. Even if you clear the balance every month, they still count your card limits because you could use them at any time. That lifts your assumed repayments and can reduce your borrowing capacity.

Lenders typically assess your approved limit when calculating commitments—so even a $0 balance can still hurt. The maths for servicing is: a lender will typically take the limit x 3.8% and add this to your monthly expenditure as an extra expense line.

What the data says (and why timing matters)

- July saw a large pay-down of card debt as tax returns hit with the biggest monthly reduction since 2022. If you’re applying soon, clearing/down-limiting in this window can help servicing.

- The number of personal credit cards in circulation fell by about a quarter of a million between July 2024 and July 2025, from 14.98 million to 14.73 million.

- Over the same period, the amount of credit card debt accruing interest fell by 0.4%.

- The RBA’s Retail Payments data pack is the source of truth for card trends; use it to benchmark balances/usage.

Practical tidy-up checklist – do this before lodging – particularly where servicing may be an issue

- Reduce limits on cards you rarely use (your bank can decrease your limit within minutes).

- Close duplicate cards; keep one everyday card if you value rewards, but pay it in full monthly.

- Ask your broker to submit your application, with a condition precedent: that your credit card limits will be reduced from $X to $Y – or cancelled.

- Avoid new BNPL lines before lodging—some lenders treat these like revolving credit.

- Proof of good conduct: 3–6 months of statements showing on-time payments helps – and payments on time show up on your credit report.

- Update your credit file: make sure closed cards actually show as closed (we audit your credit file as part of your pre-submission checklist).

BNPL on the rise

Meanwhile, Revive Financial has reported that the average BNPL balance is up ~14% year-on-year.

The rise in BNPLs appears to be due to financial hardship and is often caused by a multiple of factors combining. Revive saw cases tied to illness and business failure rise by ~33%; childbirth plus illness: ~20%; childbirth plus other pressures: ~11%; with job losses combined with illness and/or childbirth also rising.

Takeaway: with overlapping life events, BNPL debt can escalate quickly.

External signals match the risk

Finder’s June 2025 survey found

- ~44% of Australians use BNPL

- A quarter said they’ve used it for essentials (groceries/bills).

- 12% reported the instalments created other financial difficulties.

- 6% couldn’t make repayments.

- 14% admitted to unnecessary purchases.

This pattern – small balances and many scheduled payments can squeeze cash flow and show up on credit files.

What lenders are starting to look for

- Multiple BNPL enquiries and repayment history on your credit file.

- Stacked instalments (several small plans) that inflate monthly commitments.

- Missed/late BNPL payments are counted like other credit arrears under the new regime.

Quick tidy-up before you apply for finance

- Consolidate or close inactive BNPL accounts.

- Cancel auto-instalments you don’t need.

- Clear past-due BNPL first—fresh late marks are a red flag.

- Keep proof of good conduct (3–6 months statements) handy.

- If you’re close on servicing, reduce credit card limits as well—lenders assess limits, not just balances.

Balanced view

BNPL is credit. Used carefully, it can be fine; used loosely, it clutters your file and cash flow—now with more formal consequences because it sits inside the credit rules.

With our sophisticated servicing software tools,

we can quickly show you the benefit to your servicing capacity

if you were to shut down or reduce your unneeded credit facilities.

Credit cards, BNPLs, personal loans and car loans.

Caring for a long-held family home: When parents move into care or pass away

Rayleen Coates and Susan Peter-Budge from 3Two Projects do an amazing job getting the little (or not so little) things done so you can sell your home for the best possible price. They manage trades and timelines, so you can focus on your family and preparing for your next destination.

From a quick coat of lipstick to the paint work to fixing those broken tiles or wonky light switches, she has on tap a whole raft of specialist tradies who can come in and turn your home into a winner at the sale yards.

So how do they manage the delicate situation when a parent moves into care or passes away?

Suddenly managing a home full of memories – and the decisions which flow from this is stressful – and something most of us are not used to coping with.

This guide gives you a calm, step-by-step plan to secure the property, sort belongings, and present it well for sale, without burning out.

As a segue to another really useful service, have a look at Wishkeeper, a fantastic online, secure portal that allows all your family’s documents, wishes, and photos to be retained in an orderly and safe manner.

First things first: security, insurance, and basic care

- Redirect mail to the executor or a family PO box so the letterbox doesn’t overflow.

- Keep it looking lived-in: mow lawns, trim hedges, clear bins, collect flyers, set timed lights if possible.

- Insurance check: confirm unoccupied-property cover and any conditions (locks, alarms, regular inspections).

- Key register: one set per decision-maker; log who holds what.

- Contact list: insurer, solicitor/executor, property manager (if leased), trusted neighbour

- Many of the above items can be solved using Wishkeeper – see above ☝️

Personal belongings: respectful sorting without overwhelm

- Start with the “must-keep” items: photos, documents, jewellery, military/service medals, family recipes.

- Create three zones: Keep / Donate or Sell / Dispose. Label rooms or tubs to avoid re-sorting.

- Temporary storage: use short-term storage for sentimental items if decisions need time.

- Responsible disposal: recycle e-waste, chemicals, paints properly; don’t leave it to open-day week.

Tip: If emotions are running high, bring in a neutral coordinator to keep pace and defuse decision bottlenecks.

Prepare the property for sale: the high-ROI refresh

The Goal: present a clean, safe, light, and move-in-ready home. Focus on “first-impression” works – not a full renovation.

- Declutter: remove excess furniture; keep scale and light.

- Repairs & refresh: fix door hardware, taps, cracked tiles; patch and paint scuffs; replace tired lampshades.

- Kitchen & bath spruce: new handles, silicone, spotless grout; small changes read “well-kept”.

- Flooring & windows: steam-clean carpets; clean windows inside/out.

- Garden: edges, mulch, mow; simple, low-maintenance look.

- Final deep clean: kitchens, bathrooms, skirtings, gutters, paths.

- Develop a room-by-room checklist – so nothing gets overlooked.

Styling and staging: when it’s worth it

- Vacant homes usually benefit most. Staging helps buyers understand scale and flow.

- Part-occupied: consider partial styling (art, rugs, lamps) to modernise without stripping character.

- Heritage feel: honour original features (floorboards, mantels) while keeping decor contemporary and neutral.

Appraisals and sale strategy: set the plan early

- Get two or three appraisals from local agents; ask for evidence of comparable sales – use our agents’ checklist – ask and we will send it to you.

- Discuss terms that suit the family: settlement timing, early access for trades, or rent-back if needed.

- Method of sale: private treaty vs auction—choose what fits the home, location, and timing.

Admin and practicalities (often overlooked)

- Utilities: keep power/water on for cleaning and inspections.

- Compliance & safety: working smoke alarms, pool fences (if applicable), basic electrical/plumbing safety.

- Pest & building: consider a vendor report to head off surprises and speed buyer decisions.

- Digital assets: scan key documents; share a simple Google Drive folder with the family and agent. For a superior solution, get Wishkeeper – you will be glad you did.

When to bring in a coordinator (and what they do)

A specialist team like 3Two Projects can:

- Project-manage declutter, trades, cleaning and styling end-to-end.

- Arrange quotes and scheduling (painters, gardeners, handypeople).

- Keep a single timeline and budget so everyone stays aligned.

- Provide weekly photo updates and a ready-to-market checklist before the first open.

The aim is peace of mind: the home is managed thoughtfully and respectfully, and value is protected.

Quick timeline to market

Week 1–2: security, insurance, mail redirection, light garden tidy; belongings triage; agent appraisals.

Week 3–4: repairs/refresh works; book styling; deep clean.

Week 5: photography, listing copy, launch to market.

What if the family isn’t ready to sell yet?

- Consider light caretaking (monthly garden clean, interior check) to preserve the condition and insurance cover.

- If the home will be leased short-term, complete safety and compliance (smoke alarms, locks, trip hazards) before tenants move in.

- Speak with your broker (us) about holding-cost planning and any bridging finance options if another purchase is on the horizon.

Checklist — before the first open

- Mail redirected; utilities on; insurance confirmed.

- Decluttered; minor repairs done; fresh paint touch-ups.

- Garden tidy; paths/gutters cleared.

- Deep clean completed (carpets/windows).

- Styling installed; scent and lighting checked.

- Property file ready: floorplan, contract, any vendor reports

Business owners: From knowing to doing

A simple execution system for busy owners

Turn ideas into weekly wins (without working longer)

Most owners aren’t short on ideas. They lack consistent action that moves the needle. This article, provided by Glenis Gassman, gives you a lightweight weekly system to turn what you already know into progress—supporting your mindset with clear steps and simple guardrails. She has published a book on this subject, and it was recently featured in the London News – not bad for someone all the way across the globe in Queensland!

Here is a link where you can buy the paperback or the Kindle edition:

Why Knowing isn’t Enough

A precis for you to whet your appetite…

Why we stall (and how to unstick it)

Big plans die in the gap between intention and follow-through.

Common culprits are:

- Perfectionism (waiting for ideal conditions)

- Decision fatigue (too many choices, no priorities)

- Split focus (busywork over deep work)

- Self-trust dips (we stop believing we’ll do what we said)

Mindset matters—confidence, clarity, and optimism help—but mindset sticks best when you see yourself keeping small promises on your way to your bigger goals. That’s where an execution system shines.

The 5-step “Knowing → Doing” system

Use this as a weekly rhythm. It’s designed for owner-operators with real life happening around them.

1) Pick your “one result” for the week

Choose one meaningful, measurable outcome (not a task).

Examples: “Publish pricing page update”, “Book 5 capability calls”, “Ship v1 of client onboarding”.

Write it somewhere visible. If everything else slips, this still gets done.

2) Break it into three movable blocks

Create three 45–90 minute blocks that you can drag around your calendar.

- Block A: the first 20% that unlocks the rest (draft, outline, skeleton).

- Block B: the heavy lift (build, call list, edit).

- Block C: finish and ship (QA, publish, send).

Protect these blocks like appointments. (Mindset note: the calendar becomes your promise to yourself.)

3) Use “tiny commitments” to rebuild self-trust

Each day, set one tiny action you can complete in under 10 minutes that advances the result (send the email, outline three bullets, request the asset).

Tick it off.

Small wins compound belief: “I do what I say.”

4) Reduce decision fatigue with a short no-list

Before you start the week, write 3 things you are NOT doing (e.g., new landing page, ad test, webinar). Park them on a “Later” list. This frees attention for the one result.

5) Friday close-loop: evidence and next move

End the week with a 10-minute check-in:

- Did the result ship? If not, what’s the single blocker?

- Capture evidence of progress (sent, published, booked).

- Pick next week’s one result while momentum is warm.

Fixing four common execution traps

- Perfectionism → “It’s good enough to ship” – define the essential Vs the nice-to-have.

- Decision fatigue → “Three defaults – same time every week” – fewer choices, more action.

- Split focus → “theme your days” – Marketing Mondays, Deliveries Tuesdays, Sales Wednesdays, Operations Thursdays. Finance Fridays.

- Self-trust dips → “shrink the promise” – if you’ve slipped, halve the goal and do it today. Momentum first, optimisation later.

The mindset link kept practical

Use a 60-second priming cue before each block (read your one result aloud; visualise the finished thing).

Finish each block by writing the very next action on a sticky note. Your brain rests when it knows what tomorrow looks like.

Where owners see the fastest ROI

- Pricing & packaging (clarity increases conversions)

- Sales hygiene (daily 20-minute outreach, logged)

- Customer onboarding (turn a repeatable email thread into a one-pager + checklist)

- Cash drivers (quote follow-ups, invoice reviews, simple upsells).

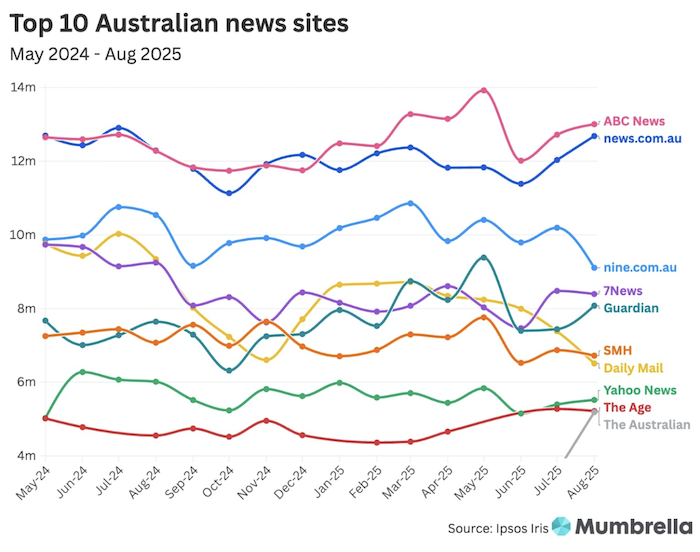

Online news insights ABC still no. 1: Free news dwarfs paywall sites

Back in the good old days, print media dominated, along with TV news.

These days, online ‘print media’ is the way to go for Australians to get their news hit. Ipsos runs Iris, the industry-endorsed digital audience measurement dataset. As reported by Mumbrella, their news article shows interesting trends as well as the market share of eyeballs.

- 21 million Australians used news websites

- Average daily consumption of news content reached 4.78 hours

The Leaders:

- ABC News ~13.0m monthly readers.

- news.com.au 12.68m (+5.4% vs July).

The Chasers:

- Nine.com.au 9.11m (down -10.7%)

- 7news.com.au 8.39m.

- The Guardian 8.08m (+8.6% after a volatile year).

- Yahoo News 5.52m (+2.3%).

Paywalled standouts:

- SMH 6.72m (top paywalled site).

- Daily Mail Australia 6.51m (≈-12%, now partially paywalled).

- The Age 5.22m

- The Australian looks to be growing strongly to almost join The Age; but….

Ipsos confirmed that The Australian’s 45% jump (to 5.19m) was driven largely by off-platform exposure (e.g., Apple News/Google News), i.e., many users of these online news platforms clicked the link for an article, but they then encountered the paywall on click-through (so they couldn’t actually read the article). I have encountered this myself via my Google news feed (thanks (not) to SMH, AFR and The Australian for getting into my Google news feed but then having a block on the article I was clicking to read).

Nuclear vs renewables: What actually scales for Australia

Subject to major plant-related meltdowns, nuclear energy is as clean as renewables. Whilst for many Australians, that risk is a bridge too far, we have a strong local voice in favour of nuclear energy as part of Australia’s energy mix.

Let’s take a step back and get an update on the global nuclear energy landscape.

A recent article in Renew Economy focused on the current status of nuclear power worldwide. In short, it is stagnating as a source of future energy.

Despite the rhetoric in the mainstream media, it has been reported in the latest edition of the World Nuclear Status Report (WNISR-2025) that:

- There isn’t a single power reactor under construction in the 35 countries on the American continent. That is staggering when you consider how long it has historically taken to build a nuclear power plant.

- The number of countries building reactors has plummeted from 16 to 11 over the past two years.

- Whilst new records for global nuclear power generation were set in 2024, they were only 1% higher than previous records. Compare that to the almost exponential growth in renewable energy – 1% just doesn’t cut it.

- The current nuclear fleet is now 32.4 years old (as of mid-2025). The average age of nuclear power plants shut down between 2020 and 2024 was 43.2 years. With a global average age in the low-30s and recent closures averaging 43.2 years, a sizable share of today’s fleet will face end-of-life decisions by the mid-2030s unless life-extension investments proceed. Yet building new plants is taking far longer than 10 years from conception to being online, with the average construction commencement to live operations being around 9 to 15 years, plus the average pre-construction timeframe for siting, licensing and financing is anywhere from 4 to 10 years (with Western countries’ projects usually at the longer end). Lower time horizons are often attained when there are multiple reactors being built as a series of standardised reactors (eg in the UAE, China and Pakistan).

- Nuclear’s high upfront cost, long build, and construction risk make the cost/availability of capital decisive—hence the need for state support (loan guarantees, CfDs, RAB, sovereign equity) to reach the Final Investment Decision.

- Utility-scale renewables are predominantly financed by private capital (equity/debt, often with Power Purchase Agreements (PPAs) underpinning the demand (businesses, energy retailers or governments buy output to underwrite the project).

- At the household level, government rebates have driven the adoption of rooftop solar and batteries.

In short

- If Australians want clean power that’s affordable and arrives fast, the global build-rate and costs point to renewables + firming (firming = batteries, hydro, and other storage systems which combat the highs and lows of renewables – aka when ‘the sun don’t shine’ and ‘the wind don’t blow’).

- Nuclear is low-carbon, but it’s slow to build, capital-heavy, and currently not legal for new projects in Australia.

- Renewables are scaling now—global additions have been running at record levels.

- Battery technology is improving, and costs have fallen sharply over the past decade, supporting firming.

- Rooftop solar + batteries are reshaping demand and supply locally; they’ll carry more of the load alongside targeted new transmission that connects renewable zones to demand centres.

Why we publish a “proper” newsletter?

clear answers, less noise!

Our newsletter packages the latest trends and ideas into plain-English, bite-sized articles—so you can make decisions faster, and you know we’re across what’s changing. And, as a side benefit, you know your broker is also keeping themselves up-to-date on the property and finance market (and a few side issues as well 😉)

What you told us – our survey snapshot

The overwhelming vote was to keep the current long-form format—everything you need in one place, no extra clicks.

We’re also exploring a header + “read on the blog” link for future editions of each newsletter, so you can save and revisit deep dives easily. Stay tuned.

How we build each edition

- Track the market: rates, policy shifts, grants, lending rules.

- Filter the noise: what actually matters for homeowners, buyers and investors.

- Explain the “so what”: quick steps you can take this week.

And, if an article sparks a question about your loan or plans,

grab a slot

and we’ll tailor the insights to you