- Best interest rates: Sep snapshot + monthly moves

- Offset not offsetting? Make sure you are getting the full benefit

- Borrowing is ticking up — your checklist to make it work for you

- More lender choice? The “proportional regulation” pivot to help borrowers

- 2025 outlook: Units set the pace (at last)

- August rate cut: four groups who can take the initiative

- Buyers: Off-market buys — beat the crowd

- Vendors: Price it right — choose truth, not hype

- SMSF & property — understanding the rules, risks, rewards

- Car-loan mistakes: eight traps to avoid

- AI in services — humans + machines win out

- Renewables spotlight — Fortescue’s “real zero” push vs farm-solar friction

- Post-solstice light is ahead of temperature increases – find out why

But first, a small request....

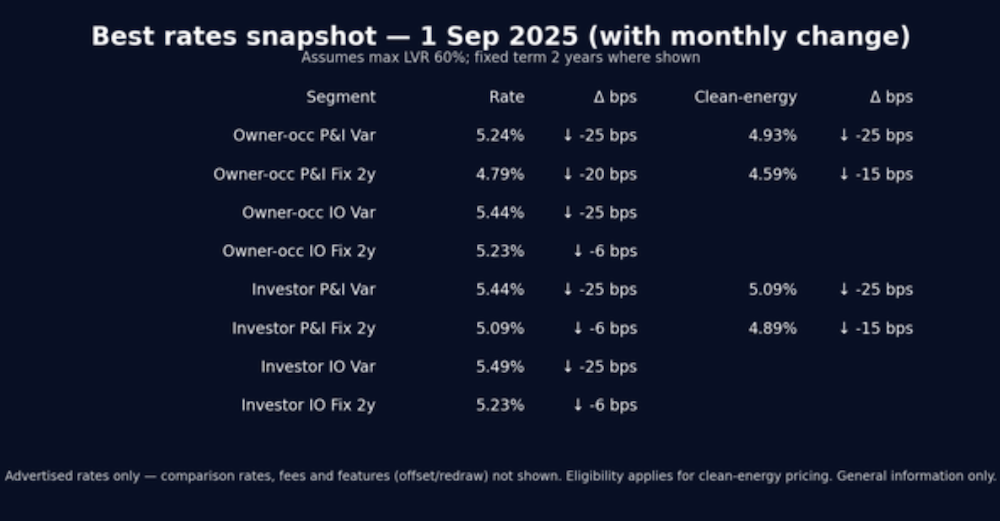

Best Interest Rates

Quick observations

- All rates broadly reflect the RBA cash rate cut, with Fixed Rates decreasing at higher levels (possibly pricing in future variable rate cuts)

- Clean-energy pricing (where offered) is typically ~0.20–0.35pp lower than the standard rate (OO P&I var: -0.31pp; inv P&I var: -0.35pp).

- IO options in this list don’t show clean-energy pricing (n/a).

- Fixed 2-year P&I rates (owner-occ and investor) are below their variable counterparts in this snapshot.

- This table shows advertised rates only. Comparison rates are not shown, and fees/features (e.g., offset, redraw, package/annual fees) aren’t reflected. Your effective cost may differ.

- Pricing assumes ≤60% LVR; other LVRs can price differently.

- Clean-energy/“green” pricing usually requires eligibility (e.g., energy-efficient home or approved upgrades) and may have extra conditions.

- General information only — no product or lender recommendations.

Offset not offsetting? Check your interest!

- Daily interest on the net amount: Interest = (loan balance – offset balance) × (rate ÷ 365), added up for the month.

- Everyday money, real savings: Cash sitting in offset lowers the interest charged without locking your money away.

- Linking/setup errors: Offset not linked to the right loan or split.

- Timing lags: Interest calculated before deposits show as cleared that day.

- Partial-offset misunderstandings: Some accounts only offset part of the balance or have conditions.

- System/config mistakes: Back-end errors when loans are restructured or refixed.

- Linking/setup errors: Offset not linked to the right loan or split.

- Timing lags: Interest calculated before deposits show as cleared that day.

- Partial-offset misunderstandings: Some accounts only offset part of the balance or have conditions.

- System/config mistakes: Back-end errors when loans are restructured or refixed.

- Export last 12 months of loan statements (with interest debits) and offset transactions; compare interest charged vs what you’d expect from (loan – offset) × rate ÷ 365.

- If there’s a gap: Start with your bank’s complaints/IDR team. If unresolved, you can go to AFCA (free).

- Next step: I’ll send you a simple CSV checklist and explain our optional Offset Check (a factual calculation review).

Borrowing is ticking up, make it work for you

Your 5-step prep checklist (plain English):

#1 Set a budget + buffer

Know your weekly limit and keep 3–6 months of repayments as a safety net.

#2 Check your credit report

Get a free report and fix errors (old addresses, closed cards still showing) - we organise this for you when we start your loan application process.

#3 Choose the right features

An offset account helps cut interest by using your savings, a redraw facility lets you access extra repayments, and loan portability allows you to transfer your loan when moving to a new property.

#4 Count the true cost

Don’t just look at the rate — include application, annual/package, valuation and settlement fees. When we show you the numbers, we look at the cost for the first two years - so you can make a realistic comparison.

#5 Broker short-list

I’ll match lenders to your profile (income type, deposit/LVR, property type, goals) and narrow to the sharp options. - using our Two Year time horizon strategy.

Market and policy pulse — more lender choice

- Canberra’s review backs “proportional regulation,” allowing smaller banks to face simpler, lighter administrative requirements (with safeguards).

- *** Customer-owned/non-majors say this will let them price sharper and innovate faster — helpful for niche borrower needs.

- Brokers drive switching, which in turn lifts competition; however, segments with fewer broker interactions will remain less competitive.

- Timing: changes need regulator implementation, so benefits build over time, not overnight.

- This is not deregulation: “Proportional” means same core prudential rules (capital, liquidity, risk controls), just scaled paperwork, not lower standards.

- APRA still supervises: Smaller ADIs remain under APRA oversight and must meet ongoing prudential tests.

- Consumer protections stay: Credit laws, hardship/help obligations, IDR/AFCA complaint rights, and disclosure rules still apply.

- Deposits protected: The Financial Claims Scheme (government guarantee) covers eligible deposits up to $250,000 per customer per ADI.

- Real-world takeaway: The bigger risk for borrowers is usually a poorly matched product or policy, not bank failure — a broker comparison helps fit the loan to your situation.

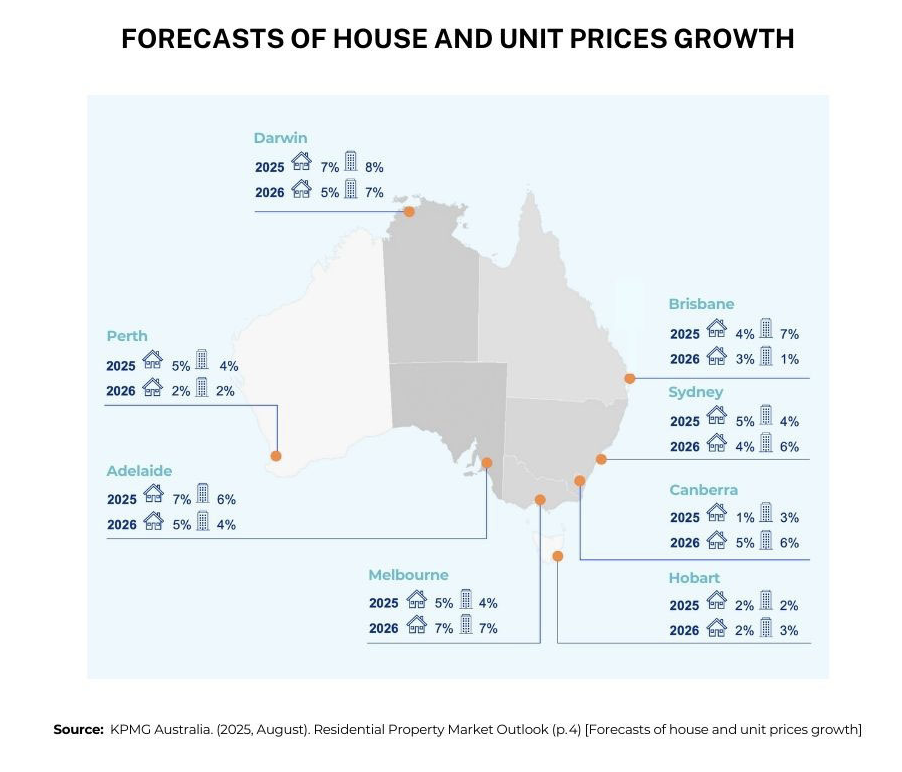

2025 outlook: Unit set the pace

- KPMG’s latest outlook has apartments outpacing houses over 2025–26 (units +4.5% in 2025, +5.1% in 2026), driven by affordability and supply constraints.

- Convergence: 2025 has seen narrower gaps in price growth across capitals; national +3.2% in six months, with Sydney/Melbourne improving as smaller capitals cool from hot levels.

- Investor momentum: Investor loans are near decade-highs in most states; Victoria is the exception (more investor selling, slower investor buying).

- Outlook: Expected rate cuts later in 2025 support prices, but affordability caps keep the focus on attached stock and realistic budgets.

- Lock-in your pre-approval before listings rise (early September onwards)

- Stress-test repayments at +2–3% for buffer, and plan strata/maintenance in your cash-flow (offset helps) – we can provide you with all this info as part of your initial Discovery Call.

August 2025 rate cut: Who can move now?

Off-market buys beat the crowd

- Privacy & discretion: Sensitive situations (family, high profile, tenants in place).

- Speed & certainty: One clean offer can beat weeks of opens.

- Lower hassle/cost: Less staging, fewer opens, reduced disruption.

- Agent networks quietly matching ready buyers to upcoming listings.

- Buyer advocates’ databases flagging owner interest before a campaign.

- Direct approaches (letters/door-knocks) in tightly held streets.

- “Test the waters”: some vendors try a quiet price to set expectations.

- Less competition and fewer bidding theatrics.

- More time to think and negotiate terms (deposit, settlement, rent-back).

- Access to homes that may never hit a portal.

- Price opacity: Fewer public comps = easier to overpay.

- Limited feedback loop: No open-for-inspection crowd to test price.

- Rushed due diligence: Without a campaign timetable, checks can get squeezed.

- Not always cheaper: “Off-market” can be used to anchor a high price before going public.

- Pull recent, like-for-like sales (same pocket, size, land, condition, orientation).

- Sense-check land value vs. improvement value (what’s the dirt worth; what’s the dwelling worth).

- Compare time-on-market norms — a long, quiet campaign can flag a mismatch on price.

- Ask the agent for their comparables and why they’re relevant.

- Contract & title review by your conveyancer/solicitor.

- Building/pest (or strata/builder’s report for apartments).

- Zoning/overlays & easements; owners’ corporation rules and levies if applicable.

- Services & compliance (smoke alarms, pools/spas where relevant).

- Finance guardrails: written pre-approval and a clear max price before you negotiate.

- Note on cooling-off: Rules differ by state/territory and by sale method. Ask your conveyancer before you sign anything.

- No recent comparables provided or weak ones from other suburbs.

- Pressure to sign without access for inspections or contract review.

- Unusual special conditions (or requests to waive cooling-off) you don’t understand.

- A clear reason to be off-market

- Price anchored to solid, recent sales

- Full access for due diligence

- Terms that make sense for both sides.

Vendors: Price it right, choose truth, not hype

- Chasing your number: Some agents ask your hoped-for price, then agree—because they want the listing.

- Days on market blow out: Overpriced homes attract fewer buyers; interest goes stale; discounts follow.

- Final price suffers: Properties that sit too long often sell for less than well-priced ones launched the same week.

- Signal vs noise: A “Just Listed” post helps the agent’s profile, not your result.

- Evidence first: Brings like-for-like comparables (same pocket, land size, condition, orientation, recent settlement dates).

- Explains the “why”: Walks you through land value vs improvement value, buyer segments, and likely objections.

- Sets strategy: Recommends method (auction/private sale/EOI), launch timing, target buyer profile, and Plan B if enquiry is soft.

- Price discipline: A realistic guide that invites competition—not a fantasy that kills it.

- “Show me the three most comparable sales in the last 60–90 days—and why they’re comparable.”

- “What buyer segments will compete for my home, and what will they push back on?”

- “Auction or private sale—why for my property, and what’s Plan B in week two?”

- “What’s your launch calendar (photos, copy, opens) and what happens if enquiry is slow?”

- “How will you qualify buyers (finance ready, timelines) before we negotiate?”

- “What price-setting risks do you see (e.g., over-capitalised improvements, busy road, layout)? Be blunt.”

- Insist on recent nearby sales (not cherry-picked from other suburbs or last year).

- Request a written rationale (land vs. dwelling, renovation premium, orientation, parking).

- Keep guardrails clear: low, mid and stretch outcomes, each tied to actual comparable sales data.

- If the guide moves, ask: What changed? (new comp, inspection feedback, building report).

- Vague comparisons or no settlement dates.

- Pressure to sign before your conveyancer checks the contract of sale/agency agreement.

- “We’ll try your price for a few weeks” with no data or fallback plan.

- Industry data consistently shows that well-priced listings attract more inspections and multiple offers early—when buyer urgency is highest.

- Over-pricing burns that window and usually costs more later.

SMSF and Property: Rules, risks, rewards

- What an SMSF is: A Self Managed Super Fund – i.e a super fund you manage. Many use it for more control; earnings are generally taxed at 15% in accumulation whilst pension-phase income can be tax-free.

- Holding an investment property in an SMSF can mean lower tax on rent and gains — usually 15% on earnings, 10% on gains after 12 months, and possibly 0% in pension phase (subject to caps) — compared with owning it personally, via a trust, or a company.

- Sole purpose test: investments must be for retirement benefits only

- Arm’s length: market value, commercial terms.

- Residential use: no living in it yourself and no renting to related parties.

- In-house assets: related-party exposures are capped (capped at 5% of fund value at 30 June).

- Only via an LRBA: An SMSF may only borrow using a Limited Recourse Borrowing Arrangement.

- Holding (bare) trust: The property is held in a separate holding/bare trust with a different trustee. The SMSF is the beneficial owner; legal title sits with the holding trustee until the loan is repaid.

- Limited recourse: The lender’s rights are limited to the acquired property and its income under the LRBA. (Note: typically, lenders will also require personal guarantees from all the members — that adds personal risk for the members).

- One asset per LRBA: Each LRBA must fund a single acquirable asset (e.g., one property) or a bundle of identical assets. There are ‘exception circumstances’, but get legal advice to see if your situation would qualify (eg when a building straddles two titles). The ATO says you may treat it as a single asset where there’s a unifying physical object (permanent, significant fixture) or a legal requirement to keep the titles together.

- Typical gearing: Up to ~80% LVR on residential is common (lenders vary). Commercial is often lower (≈60–70%). You’ll need ≥20% deposit + stamp duty + costs, plus in most cases, a liquidity buffer left in the fund.

- Paperwork-heavy & regulated: Expect detailed documents and exact naming: SMSF deed allowing LRBAs, holding/bare trust deed, loan agreement, correct purchaser on the contract, trustee resolutions, arm’s-length terms, annual audit.

- Repairs vs improvements (important): You can repair and maintain the property under the LRBA; however, major improvements that change the asset’s character are not permitted under the same LRBA

- Your SMSF can buy “business real property” and lease it to your own business — but at market rent and on commercial terms.

- Hold >12 months and capital gains may receive the one-third CGT discount (effective 10% in accumulation).

- Claim depreciation (capital works, plant & equipment) using a quantity surveyor’s schedule.

- Complexity, setup/admin costs, and ongoing audit/reporting obligations.

- Treat this as a retirement strategy first, not a tax shortcut.

- Use a qualified financial planner to assist you – it costs but they will ensure compliance so you don’t get caught out.

- Stamp duty can be complex, and the rate and requirements vary significantly by State.

- Ask your conveyancer to check every t is crossed and i is dotted.

- Contract of Sale: The bare trust trustee (not the SMSF trustee) is the Purchaser on the contract of sale (and execute the bare/holding trust deed correctly).

- Audit trail: Keep a clean paper trail (contract, duty-stamped instruments, trust deeds, lender letters).

- Before settlement: (and again before the end transfer to the SMSF trustee – typically when the loan has been repaid), ask your conveyancer to confirm the correct exemption section and lodgement deadline for your State. Do this correctly and on time, and you can qualify for nominal/exempt stamp duty.

- Set up your SMSF: well before you want to invest. Getting money transferred from an industry fund takes a few weeks at best, and getting an SMSF set up is quick once you have given clear instructions, but the timeline and process with your financial planner and accountant needs to be taken into account.

- Set up your bare trust: in advance of your proposed purchase. Whilst you don’t need to set this up when you set up your SMSF, you do need your bare trust ‘ready to go’ when you go to buy. Otherwise, if you sign the documents in the name of the wrong entity, the strict rules surrounding super funds may result in additional costs (one lender I spoke to mentioned that a client had to pay stamp duty twice because they listed the wrong entity on the contract of sale).

- Wrong names on forms (e.g., using the fund name instead of the SMSF trustee’s legal name).

- Late stamping (penalties/interest can apply if you miss deadlines).

- Beneficial ownership changes (e.g., trustee changes not documented correctly) can jeopardise duty relief.

- Deed misalignments (SMSF deed/holding trust deed must support LRBA and vesting steps).

Car loan mistakes: How to avoid them?

- Chasing a tiny monthly payment: Whilst good for showing servicing of other loans, longer terms can cost thousands more overall.

- Ignoring the comparison rate: It bakes in most fees — a better guide than the headline rate.

- Assuming dealer finance is cheapest: It’s convenient, sure, but not always the best total cost.

- Rolling extras into the loan: Paint protection, gap cover, add-ons = interest on extras you may not need.

- Skipping pre-approval: You lose leverage and can’t compare like-for-like at the dealership.

- Missing balloon/residual fine print: A low monthly payment now can mean a big lump sum later.

- Not checking early-payout fees: These can sting if you upgrade/sell early.

- Forgetting on-roads & running costs: Include stamp duty, rego, CTP/insurance, servicing, fuel/tolls in your budget.

- Get pre-approval and at least one non-dealer quote.

- Compare total cost (comparison rate + fees), not just the monthly.

- Decide upfront on extras — and don’t finance what you don’t need.

AI in services: Humans + machines win

- Early advantage: Some firms quietly use AI to deliver the same output at far lower cost, keeping the margin. That won’t last—others catch up and prices compress. (Cunningham’s “Phase 1→2”.)

- Do-it-yourself shift: As tools get easier, more companies insource routine work unless a firm adds extra value (judgment, change management, implementation). (Cunningham’s “Phase 3→4”.)

- Network effects: Firms (or niche solos) that learn across many clients build a flywheel and pull ahead. (Cunningham’s “Phase 5”.)

- Change is faster than most expect — tech leaders say the next few years could be wildly different; some predict big hits to entry-level white-collar roles in 1–5 years.

- Workplaces are already using AI for hiring and performance decisions; AI may manage more people as middle-management tasks get automated.

- Schools are scrambling: Generative AI has fueled cheating concerns, but students still need to learn safe and effective use before they graduate.

- Reality check: Not everyone agrees on the timeline (some experts argue that systems remain sub-human in areas of common sense), and CEOs can always have a vested interest — so maintain a balanced view.

- Upside: If we get this right, productivity and prosperity can benefit the broader population.

- How do you use AI? (faster research/drafts/comparisons)

- How do you check it? (human review, fact-checks, audit trail)

- Where’s my data stored? (privacy and security basics)

Renewables at scale: Big miners lean in

- Tech costs for solar, wind, and batteries continue to decline; major operators are electrifying sites to reduce fuel risk.

- Building on-site generation + storage + transmission improves cost control and reliability.

- Early movers are demonstrating that decarbonising heavy industry is both commercially viable and beneficial for the environment.

Grid rules, real hurdles: Farm solar

- Many farms can’t share solar across multiple titles/meters, even on the same property!

- Result: buying power is dear at one meter while exporting is cheap a few paddocks away.

- Industry is pushing for rule tweaks to recognise short-distance transfers and storage.

- Policy and metering settings matter – particularly the irrational, nonsensical bureaucratic ones!

- Before investing check the connection type, export limits, and tariff options. Multi-site businesses should assess embedded networks/private wires/storage to capture more value.

Why the cold peaks weeks after 21 June?

- Coastal (e.g., Sydney, Melbourne, Hobart, Perth): The ocean stores and slowly releases heat, so the lag is larger and winters feel milder but longer. Cold often peaks 3–6 weeks after 21 June.

- Inland & higher areas (e.g., Canberra, Ballarat, Alice Springs): Land responds faster, skies are clearer, so the lag is smaller with sharper frosts and bigger day–night swings—often 1–3 weeks after 21 June.

- Tropics (north): Dry‐season coolness is modest; lag is subtle.

- Home & investment: Book heater servicing, draught-proofing and insulation checks before July.

- Energy bills: Unless you have solar and batteries, expect the priciest winter weeks after the solstice – budget accordingly.

- Auctions & travel: Cool snaps linger near the coast; inland frosts bite earlier.

Keen for plain-English insights tailored to Melbourne? Our Melbourne finance news highlights where rate cuts are flowing (and where they aren’t), how to spot offset glitches, and the simple checks that keep your loan competitive.