As a Williamstown mortgage broker, I’m seeing plenty of headlines and hot takes. When the news cycle gets noisy, the smart move is to zoom out, keep a long-term view, and adjust your plan—not your pulse.

I’m not sure what to make of the news in the past few weeks so in times like this, it is wise to take a longer term view.

Reacting to each bit of news – good, bad, breath-holding and downright crazy is going to take you to the brink of your sanity – and stress levels!

The good news? The RBA is on the move with a drop in interest rates. Which is good news for the government and borrowers, particularly those who might be struggling to meet repayments. More on this below.

The Reserve Bank recently made its first cash rate decision of the year, with attention now turning to the next announcement on April 1. Here’s what else is making news:

- Best interest rates available (plus a tip for borrowers with a Variable rate loan following the RBA’s cash rate decrease)

- Offset accounts are my favourite (and sexiest) borrowing tool

- 5 better than good reasons to prepare your property for sale

- The property crystal ball

- ATO makes it tougher for businesses with cashflow difficulties

- Debunking Budgeting Myths from the Wealth Whisperer

- Nine sporting bucket list moments

- SMSF and digital assets (something your SMSF’s accountant and auditor need to know)

- The wisdom of Warren Buffett

- Property market enters new cycle

- Average mortgage reaches record $666K

- Govt lowers home loan barrier for young buyers

- What to expect from a lower-rate environment

Read more below.

Best Rates

Interest rates below as at: 5 March 2025

Please note:

- Not all lenders have reduced their rates since the RBA Cash Rate reduction of 0.25% pa – but a lot have.

- These rates exclude clean energy rates, first home buyer rates and packages and construction loan rates and an Offset feature (where applicable).

Owner Occupiers

Principal and Interest

- Fixed Rates: from 5.49% pa – 2 and 3 year terms

- Variable Rates: from 5.58% pa

Clean energy loans: Fixed Rates from 4.84% pa and Variable Rates from 5.13% pa

Interest Only

- Fixed Rates: from 5.74% pa – 2 year term

- Variable Rates: from 6.14% pa

Investors

Principal and Interest

- Fixed Rates: from 5.64% pa – 2 year term

- Variable Rates: from 5.79% pa

Clean energy loans: Fixed Rate loans from 4.94% pa Variable Rates from 5.29% pa

Interest Only

- Fixed Rates: from 5.64% pa – 2 year term

- Variable Rates: from 6.08% pa

Tip for Borrowers with a Variable Rate Loan

With the recent drop in variable interest rates, a borrower needs to be pro-active if they wish to lower their monthly repayments. Otherwise, it is likely your repayments will stay ‘as is’. Staying ‘as is’ is not a bad thing as you will effectively increase your principal repayments. And if you have an offset account set up correctly (see my article below 👇), in many situations it doesn’t matter what you do (amazing but true!). But, if you want to move to a lower monthly repayment, it is wise to check in with your lender and make sure they adjust what they are taking as your repayment.

Offset accounts are my favourite (and sexiest!) borrowing tool

Yep, you heard it first here – an Offset account is sexy!

First, some interesting news: NAB recently announced that the percentage of loans with an Offset account had reached 70% – up from 50% in 2022.

Not surprisingly, given this press release, NAB has just released its Variable Rate loan product with up to 10 Offset accounts; matching the options available for Westpac, CBA and Macquarie (but well behind the pacesetters who allow you to have up to 99 Offset accounts – I am looking at you Bank of Melbourne! – and unlimited for Bank Australia – you gotta wonder who their favourite client is!)

So why an Offset and how do you best use it to make the most of this feature?

Tip for Borrowers with a Variable Rate Loan

An offset account is a savings or transaction account linked directly to your home loan. The balance in this account is used to reduce the amount of interest you pay on your mortgage. For example, if your mortgage is $300,000 and you have $20,000 in your offset account, you’ll only be charged interest on $280,000. This setup can help you save money over the life of your loan without locking your funds away.

Tips for those about to use an offset account

#1 STOP using separate savings accounts. These accounts are costing you big time! Why? Well, you earn a lower rate of interest on a savings account than your borrowing rate. And, this savings interest rate is BEFORE TAX – so you need to reduce it by your marginal tax rate (calculators to the ready!). Only then are you comparing apples with apples.

#2 Request your employer to put all your money DIRECTLY into your offset account. That way, from day 1 of this money being deposited, you are maximising the reduction in your loan account balance.

#3 Set up different offset accounts for different purposes. EXACTLY as you would do when you had multiple savings accounts (eg, one for monthly transactions, one for the big bills, one for your holiday, one ‘to keep untouched’ for your loan reduction.

#4 You can stop worrying and fretting about the following irrelevancies (but favourite topics of media commentators and some brokers):

a) The regularity of your loan repayments

b) The term of your loan. When your offset account balance equals your loan account balance, your loan is fully paid off.

c) Making extra repayments against your loan. This is what an offset account does.

#5 If you are looking at adding an equity release loan to add to your current loan, the increase in the size of your loan repayment. This is irrelevant as the extra money you borrow as part of your equity release loan and which sits in your offset accont will effectively be available to make your higher loan repayments.

Three avoidable reasons why an offset account may not be sexy enough for you

#1 You are a spendthrift. However, no matter if your funds sit in an offset account or a savings account, a spendthrift will do what a spendthrift wants to do. But, if your surplus funds are paid against your loan account, at least it requires a manual request to gain access to the funds (via your Redraw facility).

#2 It can cost you – around $350 pa is pretty typical. Not a big deal for most people. But having said that, what is the breakeven balance you need (on average) in your offset account to make break even (with these costs) compared to a savings account? Around $3,288 per ChatGPT but this conclusion depends upon the savings rate you can get, your loan rate and your income tax rate – all pretty complicated stuff when you are debating what is essentially a simple benefit.

#3 It is generally only available for Variable Rate accounts. For those of my clients who want a Fixed Rate loan (particularly as Fixed Rates are less than Variable Rates), I recommend they keep a small balance (say $100K) in a Variable Rate account so that over the period of the Fixed Rate loan term, they can have the benefit of the lower Fixed Rate PLUS the benefit of the Offset account via the Variable Rate loan split.

The ATO makes it tougher for businesses with cashflow difficulties

We have it hot of the press from Valiant Finance that starting 1 July 2025, the General Interest Charges (GIC) on ATO debt will no longer be tax deductible.

What this means is that it may be more beneficial for a company to borrow the money to repay the ATO debt and at least get a tax deduction.

The devil is in the detail but it certainly swings the pendulum away from using the ATO as the bank of small business.

5 better than good reasons to prepare your property for sale

These tips come from Susan Peter-Budge. Susan would know because, as one of the owners of 3 Two Projects, she works with vendors to get their property in shape for sale. She organises things like getting in maintenance and trade, assisting with the pre-sale makeover, property styling, packing and unpacking, plus more.

IWhen we sold our home, the agent was able to considerably outperform market expectations because we did a paint job, fixed some rotting weatherboards and a wonky deck, plus, re-carpeted the bedrooms to freshen them up to match the new paintwork. It changed our home remarkably and made it so much easier for the agent to get a much higher price and sell it much more quickly.

#1 Maximise Your Sale Price

Buyers are prepared to pay more for homes that are move-in ready, meaning your investment in a little pre-sale work could yield a much better return. Simple updates like a fresh coat of paint, new flooring, or minor repairs can add significant value to your property.

#2 Speed Up the Sale Process

When a property is ready to move into without any need for repairs or upgrades, buyers are more likely to make an offer quickly. Homes that are clean, well-maintained, and properly staged tend to sell faster. This can help you avoid the prolonged market time that might drag down your final sale price.

#3 Stand Out in a Competitive Market

By preparing your home thoroughly, you ensure it stands out among the listings. Even in a seller’s market, competition remains fierce. A clean, updated property with appealing features can generate more interest and may even lead to multiple offers, giving you extra leverage in negotiations.

#4 Attract Serious, Qualified Buyers

A well-prepared property sends a message to buyers: this home is well cared for and ready for a new owner. This not only attracts more serious buyers but also those who are ready to act, saving you time and avoiding unnecessary viewings from buyers who may be deterred by properties in need of significant work.

#5 Avoid Delays and Negotiation Hassles

Taking care of any issues upfront means you’re less likely to face complications during inspections or negotiations. A well-maintained home can help you avoid last-minute concessions or price reductions, leading to a smoother and quicker transaction process.

Let me know if you would like an intro to Susan and her business partner, Rayleen.

The property crystal ball

One of my regular contributors, Philip Robison from The Holy Grail, has come up with the following things to reflect upon as you consider the investment property market. Terry’s comments on infrastructure are repeated by many well-known experts in the property sphere including Phil Anderson from Property Share Market Economics.

Follow The Infrastructure Trail

Unprecedented spending: Australia’s infrastructure spending is at record levels, with over $500 billion already in projects for 2024 and another $370 billion in advanced planning.

Diverse Projects: Investments cover hospitals, universities, airports, motorways, rail links, shipbuilding, and major energy projects like wind and solar farms.

Economic Stimulus: Many projects were spurred by Covid lockdown impacts, aimed at generating economic activity and jobs to avoid recession.

Job Creation Impact: For example, a planned $1 billion hospital may create 3,000–4,000 construction jobs and up to 6,000 operational jobs once completed.

Key Regions: Per capita infrastructure spending is highest in Darwin, Brisbane, Adelaide, Melbourne, and regional areas in Queensland and South Australia – areas likely to see rising house prices due to these developments.

New Leaders Emerge in Property Price Growth

Shift in Market Leaders: CoreLogic data shows that regional and apartment markets are outperforming capital cities.

Regional vs. Capital Trends: In January, capital cities saw a 0.2% drop in median house values while regional areas increased by 0.4%; a similar trend is seen in apartments (–0.2% vs +0.5%).

Changing Rankings: Nine of 15 major markets recorded increases in median house and apartment values.

Perth’s Decline: After two years of leading, Perth’s growth has slowed, showing only 0.3% monthly and 1.7% quarterly increases.

Emerging Champions: Smaller capitals like Adelaide (1.7%) and Darwin (0.6% monthly, 2% quarterly) now lead, along with regional markets in South Australia, Queensland, and Tasmania outperforming Perth.

Units to Outperform Houses

Wow. This has been a long time coming.

Price Growth Forecast: KPMG predicts unit prices will grow by 4.6% in 2025, compared to 3.3% for houses, as affordability constraints push buyers toward more accessible options.

Affordability Shift: With detached house prices soaring, more buyers are turning to units, which offer lower entry points, especially in capital cities.

Future Hotspots: Forecasts suggest that Melbourne and Sydney will see substantial unit price growth by 2026.

Current Data: As of February 2025, Sydney’s median house price is $1.437 million with units at $815,000; Melbourne’s median house price stands at $898,000 with units at $583,000. This has to level up at some point.

Debunking Budgeting Myths from the Wealth Whisperer

I recently had a fun zoom meeting with Erin Moran, the Wealth Whisperer, who is a Professional Money Coach who runs a business called Stallion Financial Group – up Queensland way.

I was not sure what to expect when I caught up with Erin but the good news is I got a lot out of it! Not only is Erin a money coach with a 10-lesson program to get you focused and on track, but she also has developed some software to help people quickly and easily budget and monitor their expenditures. I like her two-pronged attack – sound coaching advice to get you set up then a tool to make your budgeting easy.

Some tips from Erin.

Myth #1: “Budgeting Means You’re Broke”

Budgeting isn’t a sign of scarcity. As John Maxwell, a well-known leadership writer, said, “A budget is telling your money where to go instead of wondering where it went.” It’s about turning every dollar into a strategic decision that supports your goals, no matter your income.

Myth #2: “Budgeting Is Too Restrictive”

A well-crafted budget doesn’t confine you – it frees you up. By planning for your favourite activities, like a dream holiday, you assign value to your money. Budgeting becomes the foundation for the experiences you truly cherish.

Myth #3: “Budgeting Is Only for Those Who Struggle with Money”

Budgeting is a tool for everyone, from individuals to multi-billion-dollar corporations. It’s about actively managing resources for long-term success. When you see money as a tool, you’re already on the path to financial freedom.

Myth #4: “Budgeting Means No Fun”

On the contrary, budgeting lets you plan for fun without the guilt. When you know exactly where your money is going, you can enjoy life – be it a casual café meet-up or a special outing – with the confidence that your future is secure.

Myth #5: “Budgeting Means Saying No All the Time”

Budgeting is about making intentional choices. It empowers you to decide what matters most. For instance, when you’re out with friends, you might choose to invest in your future goals rather than overspending on the night out. It’s not about saying no to fun – it’s about doing it differently.

If you would like an intro to Erin, just let me know or you can reach out to her via her website:

Nine sporting bucket list moments

I met Kevin Garwood, a Travel Agent, and owner of Classic Traveller, at a recent networking event put on by VIP Executive (Margaret Cunniffe – lovely person – let me know if you would like to get an invite to one of her Melbourne events).

Anyway, back to Kevin. I asked him for his thoughts on some of the memorable sporting moments around the world which are coming up in the next year or two.

Here is Kevin’s list of events for those with a penchant for a sporting bucket list (but as I’m sure Erin the Wealth Whisperer would say, enjoy what you can afford 😍)

If you would like an intro to Kevin (he organises all sorts of travel),

let me know – he is a truly nice guy.

Or, you can vist his website.

#1 The Olympics – Summer & Winter Games

Why Travel: It’s a once-in-a-lifetime event that brings the world together.

The Olympics offer the thrill of watching record-breaking performances and experiencing the magic of the opening and closing ceremonies.

Tip: Plan your trip well in advance to secure the best seats and accommodation options.

#2 The FIFA World Cup

Why Travel: There’s nothing like the electrifying atmosphere of the FIFA World Cup. The energy in the stadiums and the celebrations in the streets make it a must-see event for any football fan.

Tip: Choose your destination carefully as tickets sell out fast. Consider a multi-city tour to catch several matches.

#3 The Super Bowl

Why Travel: The Super Bowl is much more than just a game. The intense competition, entertainment, and surrounding events create a spectacular party atmosphere that appeals even if you’re not a die-hard football fan.

Tip: Look out for additional events like NFL Experience and celebrity parties to get the full experience.

#4 The Tour de France

Why Travel: Follow the adrenaline as cyclists race through scenic French towns and famous landmarks. The Tour de France is perfect for those who love a mix of sports and cultural experiences.

Tip: Book your accommodations early in popular towns along the route to be close to the action.

#5 The Wimbledon Tennis Championship

Why Travel: Experience tennis at its best at Wimbledon. You’ll be part of history where legends like Roger Federer, Rafa and Serena Williams have competed, and you can even enjoy a traditional afternoon tea at the All England Club.

Tip: Plan to arrive early to soak up the unique atmosphere and enjoy the full experience.

#6 The Monaco Grand Prix

Why Travel: For those who love speed and luxury, the Monaco Grand Prix is the ultimate event. Beyond the race, enjoy the extravagant parties and VIP experiences that come with it.

Tip: Consider splurging on trackside seats for an up-close view of the racing action.

#7 The Rugby World Cup

Why Travel: Be part of the intense action as nations clash for rugby glory. The host cities offer a rich blend of local culture and festive celebrations between the matches.

Tip: Pack your team’s colours and join in the local celebrations for an immersive experience.

#8 The Cricket World Cup

Why Travel: The Cricket World Cup is a festival of sport where stadiums buzz with energy and fans cheer every moment of the game. It’s a brilliant way to experience both the sport and the local culture.

Tip: Take some time to explore the host country’s cultural offerings between the matches.

#9 The NBA Finals

Why Travel: For basketball fans, the NBA Finals deliver high-octane action, star power, and jaw-dropping plays. The energy in each arena is unique and thrilling.

Tip: Try attending games in different cities to experience the diverse atmospheres of each arena.

Your SMSF and digital assets (something your SMSF's accountant and auditor need to know)

Anyone with an SMSF (Self Managed Super Fund) knows that a regular audit is a requirement for their fund.

Where the fund has held digital assets (aka crypto etc), up until recently, the ATO has accepted a picture/screenshot of a digital wallet along with a signed statutory declaration to comply.

As Peter Christo, Founder and CEO of Digital Asset Custody Solutions (https://dacs.io/), has pointed out, those days are going, going, gone. Auditors now require verifiable evidence such as public wallet addresses with cryptographic signatures.

I am not going to pretend I understand the technical aspects but if you have an SMSF and you have (or are thinking of having) digital assets in your fund, you will need to make sure your SMFS’s Accountant and Auditor do not fall foul of their obligations. Which is where Peter’s solution steps in. It allows the SMSF trustees to be able to provide the evidence which will satisfy the ATO.

Let me know if you would like me to put your SMSF’s Accountant and Auditor in touch with Peter.

The wisdom of Warren Buffett

As Warren Buffett liquidates his holdings in ETFs (to zero), now is the time to reflect upon the wisdom that has driven his company, Berkshire Hathaway, to a sustained period of way-above-average growth.

Scott Phillips from Motley Fool gave the following summary from Warren Buffett’s annual shareholder letter:

#1 Mistakes happen, just make sure you fix them

Buffett reminds us that everyone makes mistakes, whether it’s in capital allocation, hiring, or evaluating business prospects. What matters most is to quickly fix those errors. As Charlie Munger (who Warren Buffett called ‘the architect of Berkshire Hathaway business philosophy) put it, failing to act in the face of a problem is a costly habit. The takeaway for investors is clear: recognise your mistakes, cut your losses when needed, and avoid holding on to poor decisions out of stubbornness.

#2 Invest in businesses – not just shares

Buffett highlights the difference between owning shares and truly owning a business. Berkshire Hathaway does both – fully owning 189 companies while also holding significant stakes in giants like Apple, American Express, and Coca-Cola. His core philosophy is to invest in great businesses with competent, ethical managers. At The Motley Fool, the same mindset applies: invest in companies, not just share symbols.

#3 Life without Buffett

At 94, Buffett acknowledges his time at the helm is nearing an end, naming Greg Abel as his successor while ensuring that Berkshire’s culture and investment philosophy remain intact. He also warns future leaders that deceiving shareholders will ultimately lead to self-deception, underlining the importance of business integrity.

#4 Results speak volumes

Berkshire Hathaway enjoyed a robust year with operating earnings rising to US$47.4 billion from US$37.4 billion. This growth was driven by higher investment income from US government bonds, boosted by rising interest rates, and strong performance from GEICO under Todd Combs. The company’s insurance businesses, which generate billions in “float” (premiums collected before claims are paid), continue to be its core strength, giving it a competitive edge by enabling early capital investment.

#5 Paying your taxes is the sign of a good thing

Berkshire Hathaway paid a record US$26.8 billion in corporate income tax in 2024 – more than any other US company and accounting for 5% of all corporate tax collected. This massive tax bill is a result of its long-term reinvestment strategy, which compounds growth by reinvesting earnings rather than paying dividends. Buffett sees this as a point of pride, highlighting Berkshire’s meaningful contribution to the US economy.

#6 There’s value across the ditch

Buffett’s strategic investment in Japan, acquiring stakes in five major trading houses (ITOCHU, Marubeni, Mitsubishi, Mitsui, and Sumitomo) in 2019, has yielded impressive growth—from US$13.8 billion to US$23.5 billion. Alongside vice-chair Greg Abel, Buffett is committed to these holdings for the long term, demonstrating that patient investing pays off.

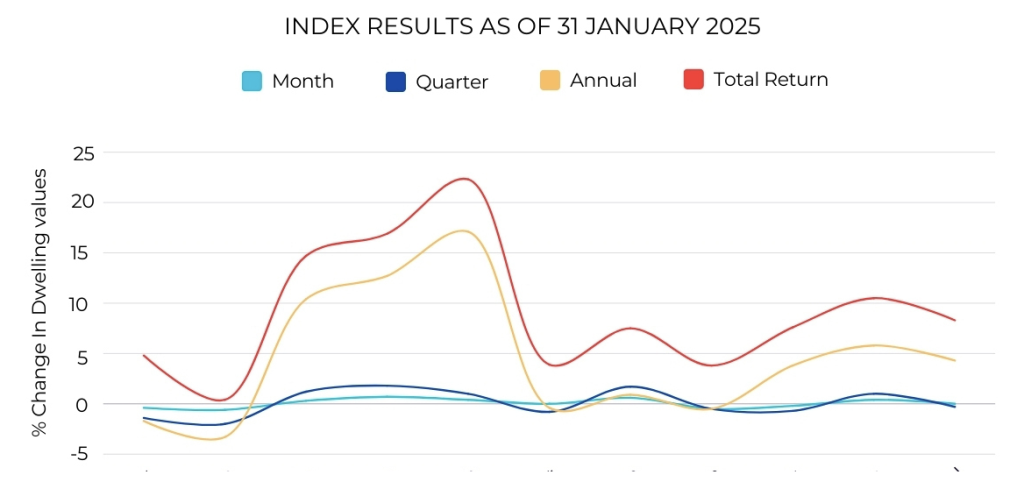

Property Market Moves Into New Cycle

Australia’s median property price fell 0.3% over the three months to January, following almost two years of steady growth, according to CoreLogic. While this downturn might raise concerns, it’s worth remembering the long-term cyclical trends that govern property prices—a perspective often highlighted by Philip Anderson.

Long-Term Cycles

Anderson’s view reminds us that property markets typically move in cycles. Periods of growth are often followed by corrections, which, in the long run, can present new opportunities for buyers and investors. Even though current data shows a slight decline, history suggests that downturns are usually temporary before the market finds its footing again.

Key Questions Ahead

As the market enters this new cycle, three main questions have emerged:

- How long will the downturn last?

- How deep will it be?

- What impact will rate cuts have on the market?

These questions are on everyone’s minds, and we’re closely monitoring developments to understand how they might affect your property decisions.

Looking Ahead

If you’re considering buying or refinancing, keep in mind that market corrections can offer strategic entry points. Staying informed and taking a long-term view is key to navigating these cycles successfully.

“Lower mortgage rates and a subsequent lift in borrowing capacity as well as an under-supply of newly built housing could be setting the foundations for a relatively shallow housing downturn,” CoreLogic Research Director Tim Lawless said.

It is also important to note that the rate reduction is probably feeding more into the affordability narrative rather than the ‘it’s time to buy property’ narrative.

Having said that, don’t be surprised if 2025 is a good year for property prices.

“But the easing cycle for interest rates is likely to be a gradual one, and we also have the ongoing headwinds of affordability constraints, normalising population growth and generally soft economic conditions to contend with. All things considered, the likelihood of a significant growth cycle over the coming year remains low.”

That would be positive news for buyers, because it would mean steady prices and restrained competition.

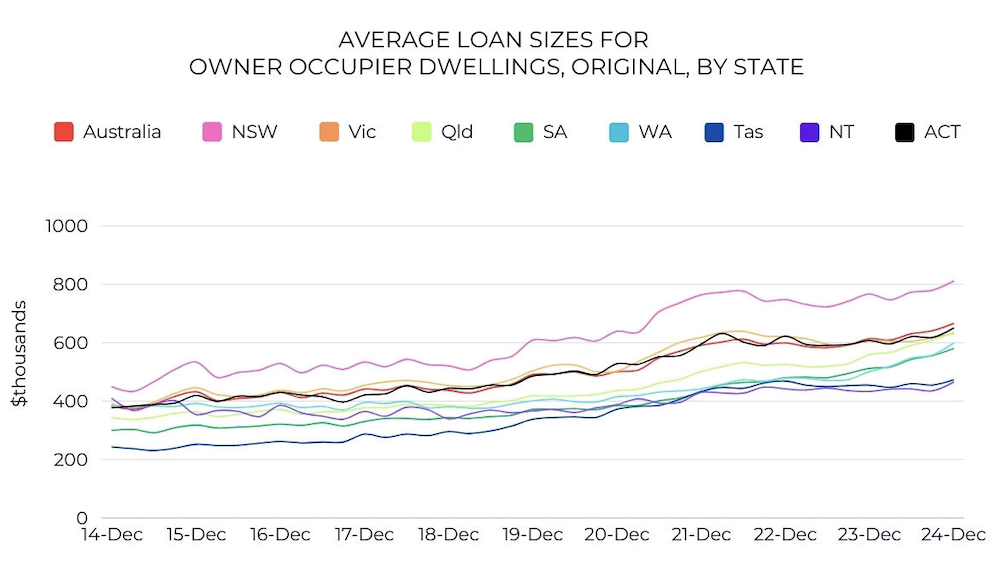

Rising Prices Leading To Rising Mortgage Commitments

Home loan customers are now borrowing an average of $666,000 per mortgage—a new record, according to December lending data from the Australian Bureau of Statistics. Over the past decade, average loan sizes have jumped by 73.4%, reflecting the sharp rise in property prices and the borrowing requirements that come with them.

Different states have seen varying growth. For instance, while the Northern Territory experienced just a 13.7% increase in loan sizes over the last 10 years, Tasmania saw an almost 95% rise. These differences highlight that while the national trend is for larger loans, regional factors still play a major role in lending and affordability.

As borrowing records are set, it’s important to consider how these trends affect loan affordability. With larger loans, customers will typically face higher repayments, which emphasises the need for careful financial planning and personalised advice when entering the market.

Boosting your Home Loan Qualification

If you’re planning to buy a property later this year, here are some extra tips to strengthen your home loan application in Australia:

- Build a Larger Deposit: Increasing your deposit can lower your loan-to-value ratio, which might help you secure a better interest rate.

- Monitor Your Credit Report: Regularly check for errors or inconsistencies that could affect your credit score.

- Consolidate or Reduce Debts: If you have multiple loans or credit cards, consolidating them or paying down high-interest debts can show lenders you’re managing your finances responsibly.

- Keep Your Financial Profile Stable: Aside from staying in your job, avoid switching banks or making major changes to your financial setup before applying.

- Document All Income Sources: Whether it’s salary, part-time work, or investments, having clear proof of all income streams can support your application.

- Speak to us early: We can help you understand the lender’s requirements and guide you through the process with current market insights.

- Consider a Guarantor: If you’re eligible, having a guarantor can sometimes improve your borrowing power and loan terms.

Govt Aims To Lower Home Loan "Barrier" For Young Buyers

Student Loan Relief on the Horizon

Property buyers with outstanding student loans might soon find it easier to qualify for a mortgage thanks to proposed changes from Treasurer Jim Chalmers. Under these new rules, lenders could, in some cases, exclude HELP-HECS debt from their serviceability calculations when assessing home loan applications.

Currently, lenders treat student debt the same as other debts, even though repayments don’t start until you earn at least $54,435 a year. Recent media discussions suggest that excluding this debt could ease the burden on young professionals and recent graduates, potentially widening access to the property market. However, some experts caution that while this move may improve serviceability ratios, it will be important for lenders to balance this change with overall financial risk management.

Overall, these proposed changes could provide much-needed relief and support for borrowers in the competitive Australian lending environment, making the dream of home ownership a little more accessible for many.

“Currently, a barrier for young Australians to get into the housing market is the reluctance of banks to give them a mortgage. The ABA [Australian Banking Association] has indicated that one reason for this uncertainty is the interpretation of lending regulations and guidance by APRA and ASIC,” Dr Chalmers said.

“APRA has confirmed it will start consultation soon on the treatment of HELP debts in serviceability requirements and debt reporting. ASIC has confirmed it will move to quickly implement changes to its guidance on the treatment of HELP debts, following targeted consultation.”

What To Expect From A Lower-Rate Environment

A Closer Look at Rate Cuts: Profit or Market Share?

As expected, the Reserve Bank of Australia (RBA) reduced the cash rate in February, a move that generally brings down variable-rate mortgages. But look closer, and you’ll see a different story emerging in the way lenders react.

Lenders usually adjust their variable interest rates in line with the RBA’s decisions. However, not all follow suit immediately. Some delay their rate cuts, which raises a cynical question: do they enjoy a few extra weeks of higher interest margins for extra profit? There’s a growing perception that delaying the pass-through of the full rate cut can sometimes be more about boosting profits than swiftly passing on savings to borrowers.

Moreover, not all lenders reduce their rates by the full amount of the RBA’s cut. In some cases, lenders opt to only pass on part of the reduction. The reasoning here might be that by doing so, they can maintain a healthier profit margin rather than competing solely on price for market share. It appears that for some, the priority might lean towards maximising profit rather than offering the lowest possible rate to win over customers.

It’s also worth noting that these changes have a dual impact: new borrowers may benefit from increased borrowing power and potentially qualify for larger loans, which could boost property demand. On the flip side, those saving for a deposit might find themselves earning less interest on their savings, further complicating the financial landscape.