- Best interest rates

- Negative cashflow is on the rise – let’s dive deeper into negative gearing

- Renewables’ best kept secrets

- Tips for tradies starting a business (also good for anyone else!)

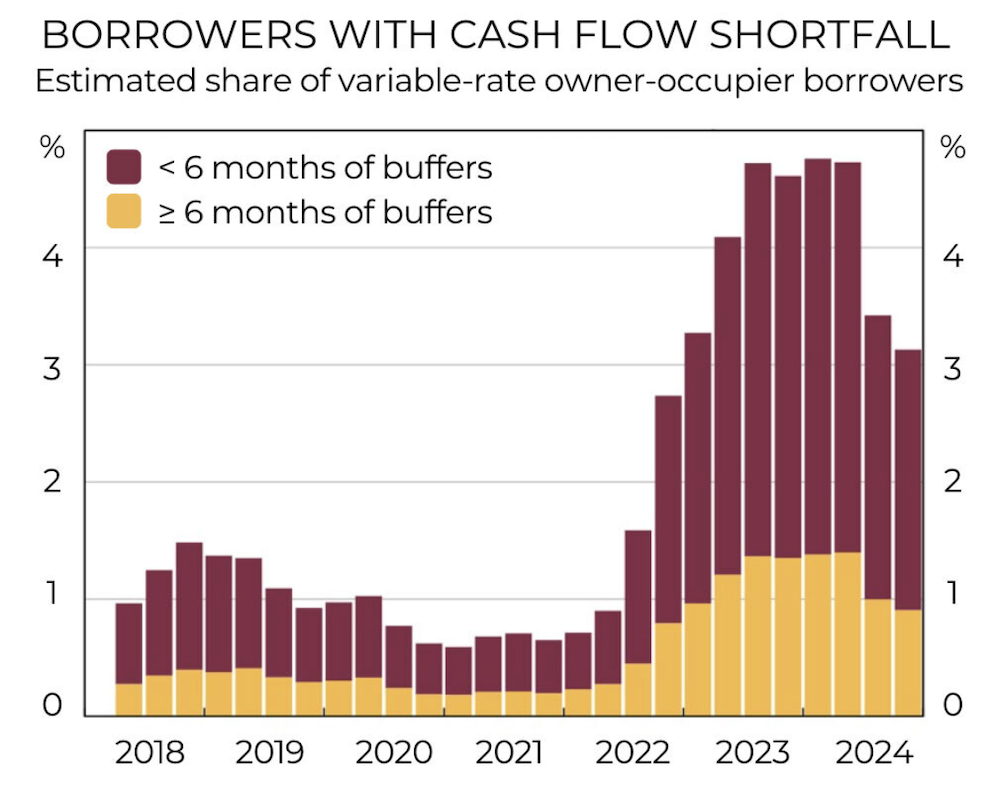

- 97% of borrowers are in good shape.

- NBN Gigabit plans? They are here (and reasonable)

- Can you afford a home loan?

- Chat GPT – the rules of prompting have changed

- Australia – king of the (highly priced) property market?

- AUKUS – back in focus

- Pros and cons of balloon car loans.

Best Rates

- The most recent RBA Cash Rate change was the 0.25% decrease in February 2025.

- This Rate was maintained at the RBA Board Meeting in April.

- The next RBA Board Meeting is scheduled for 20 May 2025. Whilst the pundits are anticipating a further rate reduction, the RBA has not made any announcement to suggest that this will be the case.

- The rates below exclude: > clean energy rates > first home buyer rates > packages > construction loan rates > offset account feature.

- The best rates are based upon a 30 year loan with a Loan to Value Ratio (LVR) of less than 60%. This is typically the lowest LVR used by lenders when sharpening their rates.

- Interest Only rates are based upon an Interest Only period of 1 year.

- Fees and charges are excluded from consideration. These can be considerable for some lenders so we always recommend a full analysis of all the costs you will be likely to incur. We provide this service for you when you book a time for an initial discovery call chat.

Owner Occupiers

Principal and Interest

-

Fixed Rates: from 5.19% pa – 2 and 3 year terms; down by 0.45% from last month

-

Variable Rates: from 5.64% pa; no change from last month

-

Clean energy loans:

-

Fixed Rates from 4.94% pa; down by 0.20% from last month

-

Variable Rates from 5.43% pa; no change from last month

- Fixed Rates: from 5.74% pa – 2 and 3 year terms; down by 0.25% from last month

- Variable Rates: from 6.04% pa; down by 0.10% from last month

Investors

Principal and Interest

- Fixed Rates: from 5.74% pa – 2 and 3 year terms; down by 0.39% from last month

- Variable Rates: from 5.79% pa; no change from last month

- Clean energy loans:

- Fixed Rate loans from 4.94% pa; no change from last month

- Variable Rates from 5.29% pa; no change from last month

- Fixed Rates: from 5.64% pa – 2 and 3 year terms; down by 0.15% from last month

- Variable Rates: from 6.08% pa; down by 0.01% from last month

Surveys Find More Property Investors Are Experiencing Negative Cash Flow

Before we start

The current negative gearing statistics explained

Quick tip if it’s been at least two years since you took out your home loan:

Deep Dive: Investment properties are a business

- From the profits the business makes and/or

- The increase in the value of the business and its assets.

What is negative gearing?

- Cash expenses and

- Non-cash expenses

So let's define depreciation

Depreciation is the accounting method used to spread the cost of an asset over its useful life, reflecting its gradual decrease in value due to wear and tear, obsolescence, or other factors. In essence, it's the process of recognising that assets lose value over time and distributing that loss of value as an expense over the asset's useful life. The accountant's logic is that by making this allowance in your profit and loss statement, you are funding the future acquisition of a replacement asset by making a charge against the profits which are being generated from that asset.

Ok, you still with me? Good! Let's continue.

Three Scenarios which apply to property investors

Scenario #1:

Your investment property rental income is greater than all your expenses.

Scenario #2:

Your investment property rental income is less than all your expenses (cash and non-cash) BUT it is greater than your cash expenses.

Scenario #3:

Your investment property rental income is less than all your expenses AND it is less than your cash expenses.

- If you can afford to fund this cash shortfall, this may not be an immediate issue. For example, you either earn lots of money and/or you have typically been able to save money, then you can potentially survive with this scenario.

- If you have not typically had a lot of spare cash from your day job, then this can put a huge strain on your financial resources and dare I say it, your relationships (money stress issues are right up there as a cause of marital break-ups).

- When you are in a cash loss position, you need to weigh up the negative impact of this cash loss against the (hopefully), future gains on the value of the property.

Renewables' best kept secrets

US Power Grid

- Between 2021 and 2024, grid battery capacity increased fivefold. During 2024, the US installed 12.3 gigawatts of energy storage. This year, new grid battery installations are on track to almost double compared to last year. Battery storage capacity now exceeds pumped hydro capacity, totalling more than 26 gigawatts.

- The aging US grid is in dire need of upgrades, and batteries can cushion the shock of adding gigawatts of wind and solar while buying some time to perform more extensive renovations. Some power markets are finally starting to understand all the services batteries can provide—frequency regulation, peak shaving, demand response—creating new lines of business. Batteries are also a key tool in building smaller, localized versions of the power grid.

- The most common battery storage technology, lithium-ion cells, saw huge price drops and energy density increases – from $3,000 a kilowatt-hour in 2008 to $150-$200 a kilowatt-hour for the full system install.

- The combination of solar plus storage accounted for 84 percent of new US power added in 2024.

- Most of Australia’s coal and natural gas is exported (14,904 Petajoules or 72%)

- Of all our domestic energy consumption of 1,500 terawatt hours (TWh), around 964 TWh or 64%, is lost before it gets to the end user. Inefficient coal and gas-fired power plants account for a third of this lost energy (314 TWh) whilst transportation (via combustion engines), accounts for over a fifth (200 TWh)

- If we electrified Australia with renewable electricity (think of South Australia for a minute), two things would happen:

- #1 – total energy entering the system would fall to 749 TWh – down from 1,500 TWh

- #2 – lost energy would account for 169 TWh of this total compared to the current 964 TWh.

Tips for starting a business as a tradie (or anyone else for that matter)

RBA reports just 3% of home loan customers have a cash flow shortfall

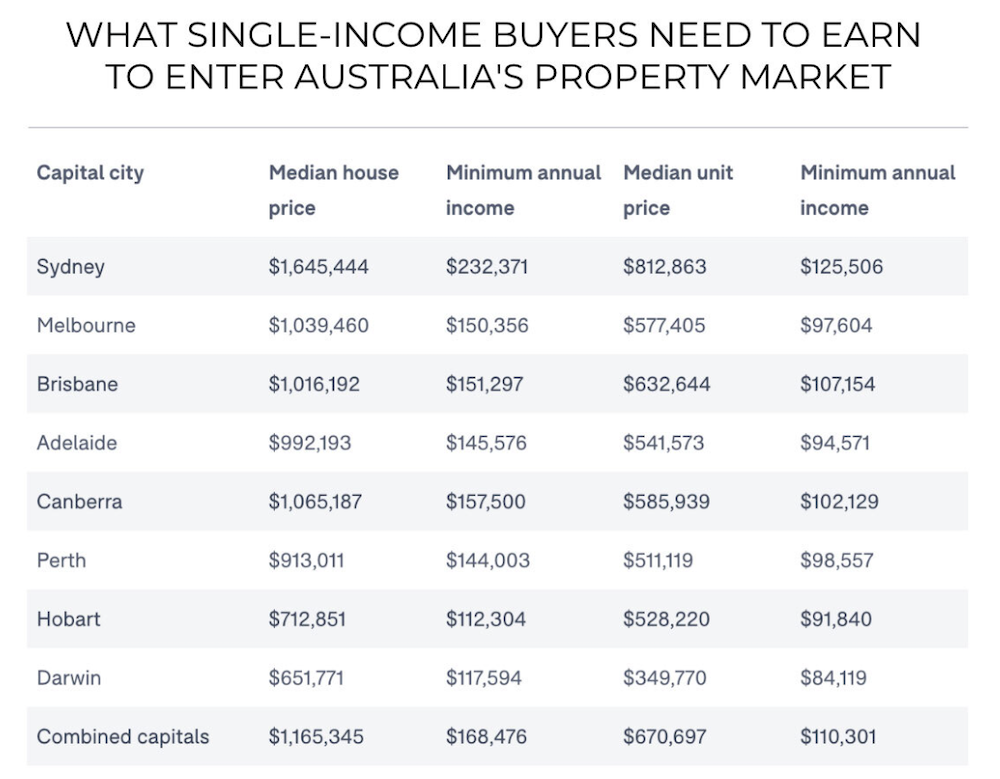

From $84k to $232k: The salary needed to service a mortgage across Australia

- Get a loan with an offset account. As regular readers know, I go a step further. Use your offset account as the account which receives your salary and from which you pay your bills. Treat your offset account splits the same as you would have traditionally used savings accounts. The more you park (and keep!) in your offset account, the less interest you’ll be charged on your loan.

- Capitalise on lump-sum payments. Use tax refunds and cash gifts to either pay down your mortgage or beef up your offset account. Again, as per my advice above, don’t stick them anywhere first other than your offset account. And if you find a better use for these funds, only then take them out of your offset account.

- Avoid setting-and-forgetting your home loan. People who stick with the same mortgage for 30 years generally pay more interest over the life of their loan. Instead, think about refinancing every two years or so. Why? Well, banks are no different to many other large service providers. If you play the ‘set and forget’ game, they will attempt to make a little bit more income from you. Why? Because they can and you are not watching!

NBN Gigabit plans? They are here (and reasonable)

Chat GPT: the rules of prompting have changed

- Role and objective: Tell ChatGPT who it should act as and what it’s trying to accomplish

- Instructions: Provide specific guidelines for the task

- Reasoning steps: Indicate how you want it to approach the problem

- Output format: Specify exactly how you want the response structured

- Examples: Show samples of what you expect

- Context: Provide necessary background information

- Final instructions: Include any last reminders or criteria

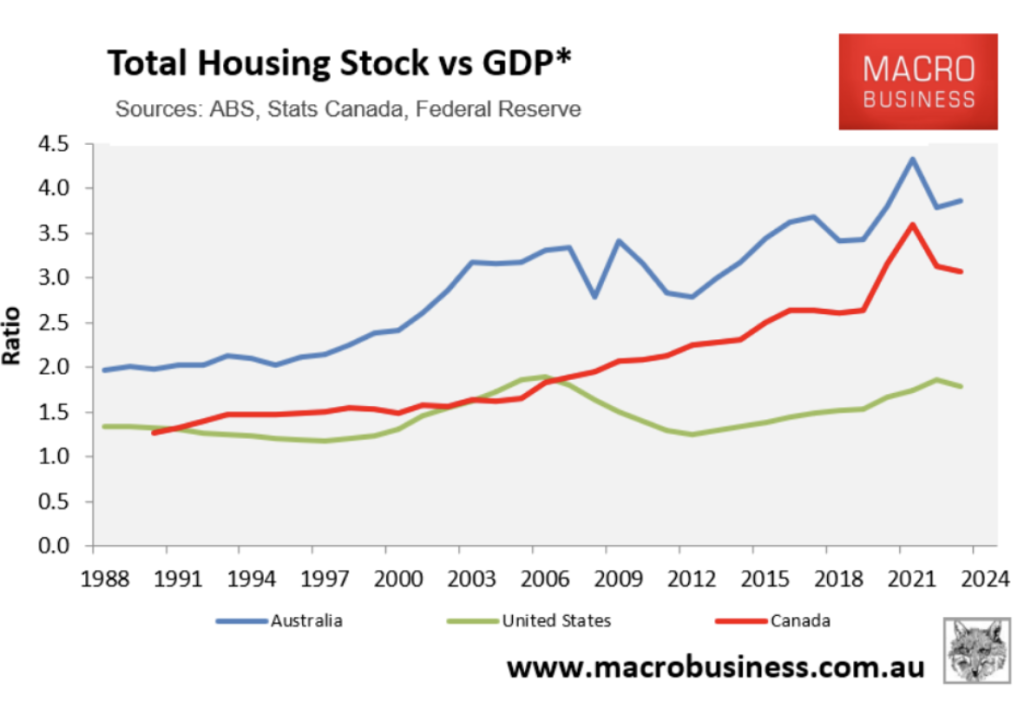

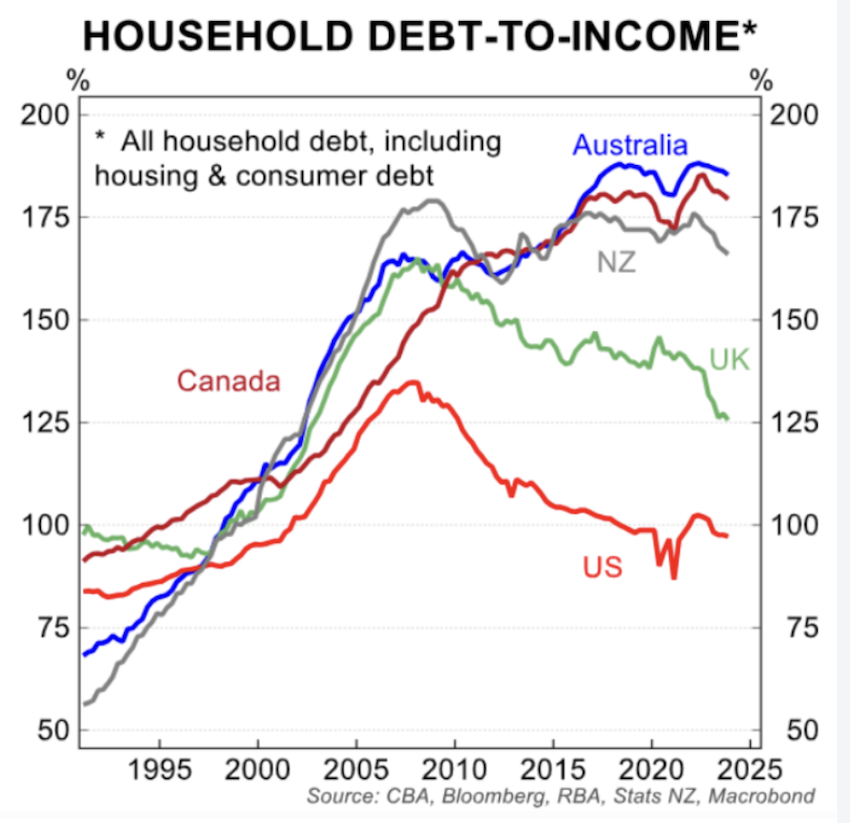

Australia - king of the property market?

- CoreLogic’s latest monthly chart pack valued Australia’s housing stock at $11.3 trillion as of the end of March 2025, with the average home valued at exactly $1 million.

- The value of Australia’s housing market relative to its economy is among the highest in the world, more than doubling the United States.

- Australian households carry some of the world’s largest debt loads, driven overwhelmingly by mortgage lending.

- Interestingly, back in 1995, our ratio was below all of the countries shown bar New Zealand. Along with Canada and New Zealand, our ratio has risen sharply – unlike the US and to a lesser extent, the UK

- In 1990, nearly two-thirds of bank lending was for businesses, and only around one-quarter of the lending went to mortgages. Thirty-five years later, this has flipped around, with nearly two-thirds of bank lending for mortgages versus only one-third for businesses. The crossover point? around 2000.

AUKUS - back in focus

- For more than a century, Australia has followed the same defence policy: dependence on a great power. This was first the United Kingdom and then the United States. Nothing new here. Except we have a rather different approach being taken by our good friends in the USA these days. I don’t know if anyone really knows where the US is heading (and what will be the cost they require us to pay).

- Albert supports the concept of the strategic defensive philosophy which he says is best suited for status quo states like Australia; the status quo being defined as “we are happy with what we have”. He goes on to say the needs of status quo states can be met without recourse to intimidation or violence. These states tend to be militarily weak relative to potential aggressors, and, they aren’t aggressors themselves. If war eventuates, Australia’s only goal is to prevent a change to the status quo.

- He also observes that defense is naturally a stronger position in war compared to attack. “It is harder to capture ground (including sea and airspace) than it is to hold it. All aggressors must attack into the unknown, bringing their support with them. Defenders, by contrast, can fall back onto a known space and the provisions it can supply.”

- The wide water moat surrounding the Australian continent greatly complicates and increases the cost of any aggressor’s effort to harm us. Our task, under strategic defensive, is to make any attack prohibitively expensive, in terms of equipment and human life.

- Long-range strike missiles and drones, combined with sensors, provide the defending nation with the ability to create a lethal perimeter around it.

- Australia has no need to operate in distant waters, such as those off the coast of China.

- In addition, Australia can afford so few vessels that their deterrence effect is not credible.

- The nuclear-powered submarines will not be available for a long time. Our need for protection is now.

- Long-range strike technology means the sea can now be controlled from the land. Rapidly improving sensors make it impossible for attackers to hide on, below or above the surface of the ocean.

- A better bet would be for Australia to invest in uncrewed surface and sub-surface maritime vessels to patrol its approaches, as well as large numbers of land-based launchers and missiles.

Is a balloon car loan the right choice for you?

Considering a Car Loan with a Balloon Payment? Here's What You Need to Know

The Pros

- Lower Monthly Repayments: By deferring a portion of the loan, your regular repayments are reduced, making the loan more affordable in the short term.

- Increased Cash Flow: The savings on monthly repayments can free up cash for other expenses or investments.

- Flexibility: If you plan to sell or trade in the car before the balloon payment is due, you can use the proceeds to cover the lump sum.

The Cons

- Larger Final Payment: At the end of the loan, you’ll owe a significant lump sum, which could be challenging to pay unless you’ve planned ahead.

- Higher Overall Interest: Since interest is calculated on the full loan amount, you may end up paying more over the life of the loan.

- Depreciation Risk: If the car’s value drops below the balloon amount, you could end up owing more than it’s worth.

Recent Trends in the Australian Car Loan Market

- Extended Loan Terms: More buyers are opting for longer loan terms, with seven-year car loans becoming increasingly common.

- Interest Rates: Car loan interest rates have been fluctuating, with rates typically starting around 6-7%. It’s important to shop around and compare offers.

- Balloon Payment Options: Many lenders offer balloon payment options, allowing for lower monthly repayments. However, as noted above, it’s crucial to consider the long-term financial implications.